The Next Phase

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

The second quarter reminded investors that markets rarely move in a straight line. Geopolitical conflict, shifting Federal Reserve expectations, renewed inflation concerns, and growing scrutiny of artificial intelligence investment all created periods of heightened volatility. Yet despite the steady stream of headlines, investors repeatedly looked through short-term uncertainty and refocused on the factors that ultimately drive long-term returns: earnings growth and productivity.

That focus was well supported by improving underlying fundamentals. Corporate earnings expectations moved higher, businesses continued investing aggressively in AI and other productivity-enhancing technologies, and economic growth remained resilient. As we enter the second half of the year, the investment landscape appears to be entering a new phase — one in which investors are transitioning from debating whether the economy can withstand higher interest rates and geopolitical uncertainty to evaluating how the tremendous levels of capital deployment into artificial intelligence may shape the next stage of economic growth.

Q2 2026 at a glance

- Economic Growth: Economic growth remained resilient despite geopolitical tensions and higher interest rates, supported by healthy consumer spending, continued business investment, and productivity gains. While growth moderated from last year's pace, the economy continued to outperform many expectations.1

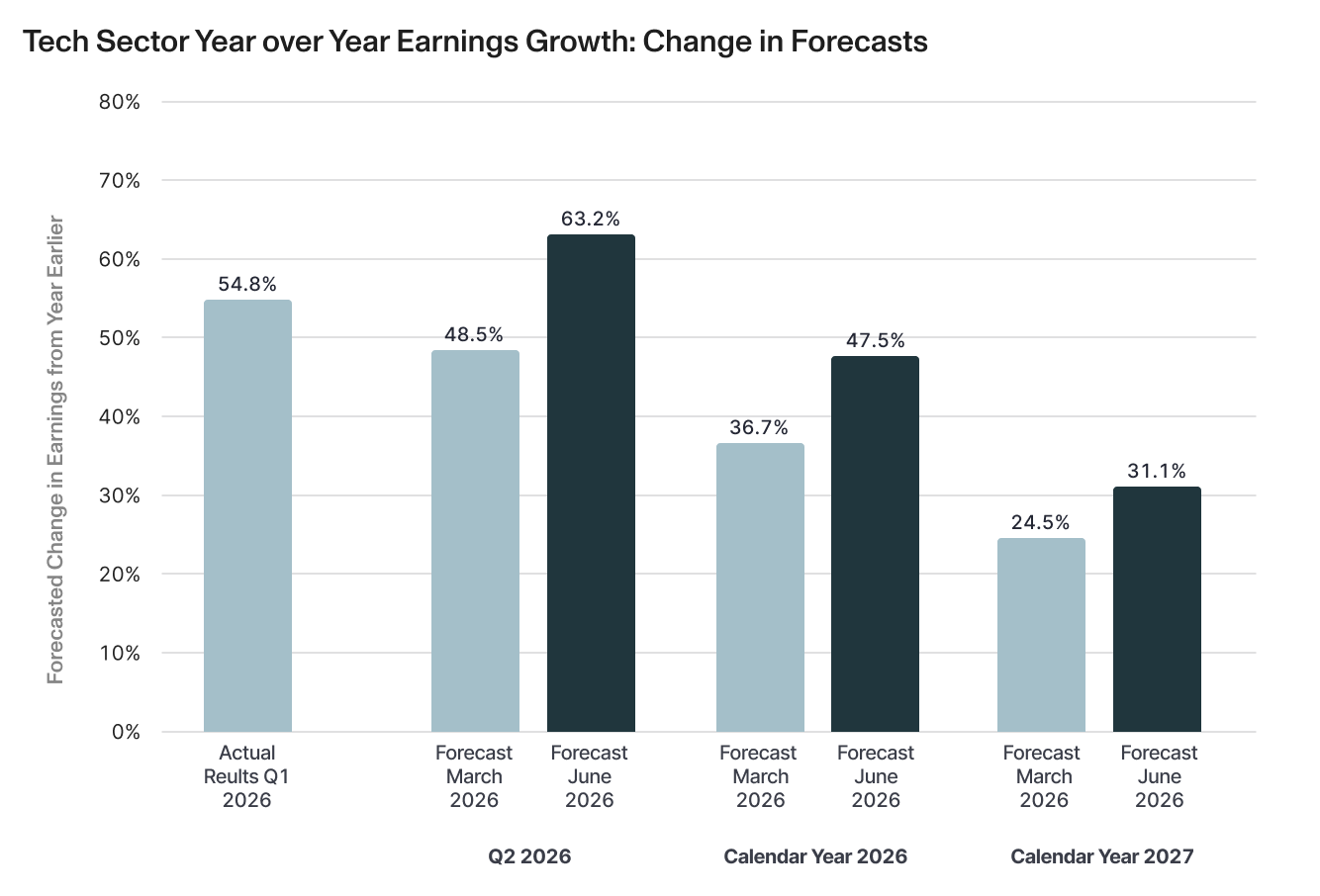

- Earnings: Corporate earnings results for the first-quarter also exceeded expectations and analysts raised forecasts for the remainder of the year. Positive guidance and broadening earnings growth reinforced confidence in the fundamental outlook.2

- Equity markets: Equity markets continued their advance despite periods of heightened volatility. Market leadership also broadened, with gains extending beyond the largest technology companies into other sectors benefiting from economic growth and AI-related spending.3

- Fixed Income: Despite some retreat in June, bond yields remained elevated as investors adjusted to a Federal Reserve expected to keep policy restrictive for longer than previously anticipated.4

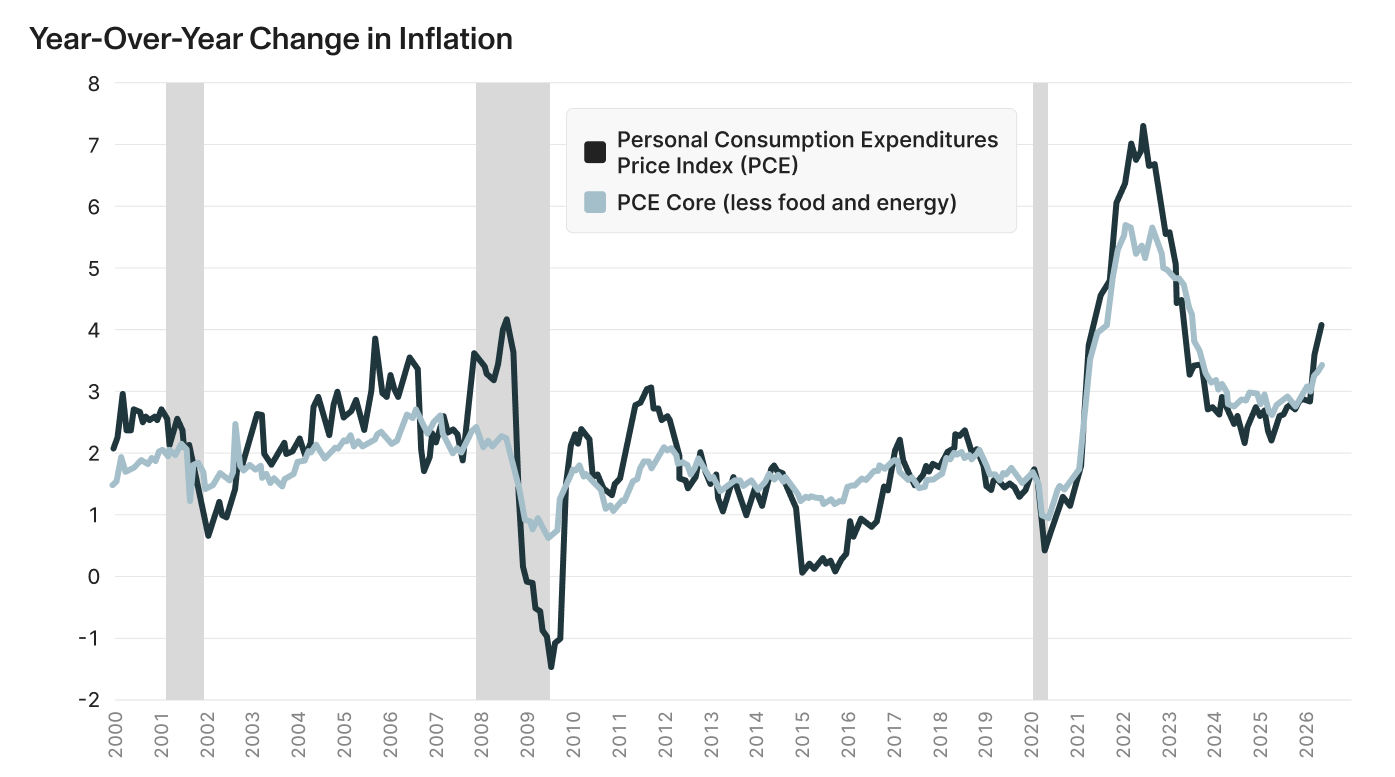

- Inflation and Employment: Inflation remained above the Federal Reserve's long-term target but was largely concentrated in a handful of categories rather than broad-based.5 Labor market conditions remained healthy, with solid job gains and still low unemployment.6

- The Federal Reserve: The Federal Reserve unanimously held rates steady in new Chair Kevin Warsh’s first FOMC meeting. Chair Warsh emphasized real-time economic data, productivity trends, and the risks of easing policy prematurely. Markets responded by shifting expectations away from interest rate cuts toward the possibility of rates rising later this year.7

- Artificial Intelligence: The conversation around artificial intelligence continued to evolve from enthusiasm over technological breakthroughs to evaluating how rapidly massive investments can translate into sustainable earnings growth. AI's influence is broadening beyond technology companies into infrastructure, utilities, industrials, private markets, and credit.8

- Geopolitical risks: The conflict with Iran has pushed energy prices higher, but oil prices retreated after a U.S.-Iran memorandum of understanding reopened the Strait of Hormuz and reduced immediate concerns over global energy supplies. Nevertheless, the region remains an important source of geopolitical risk.

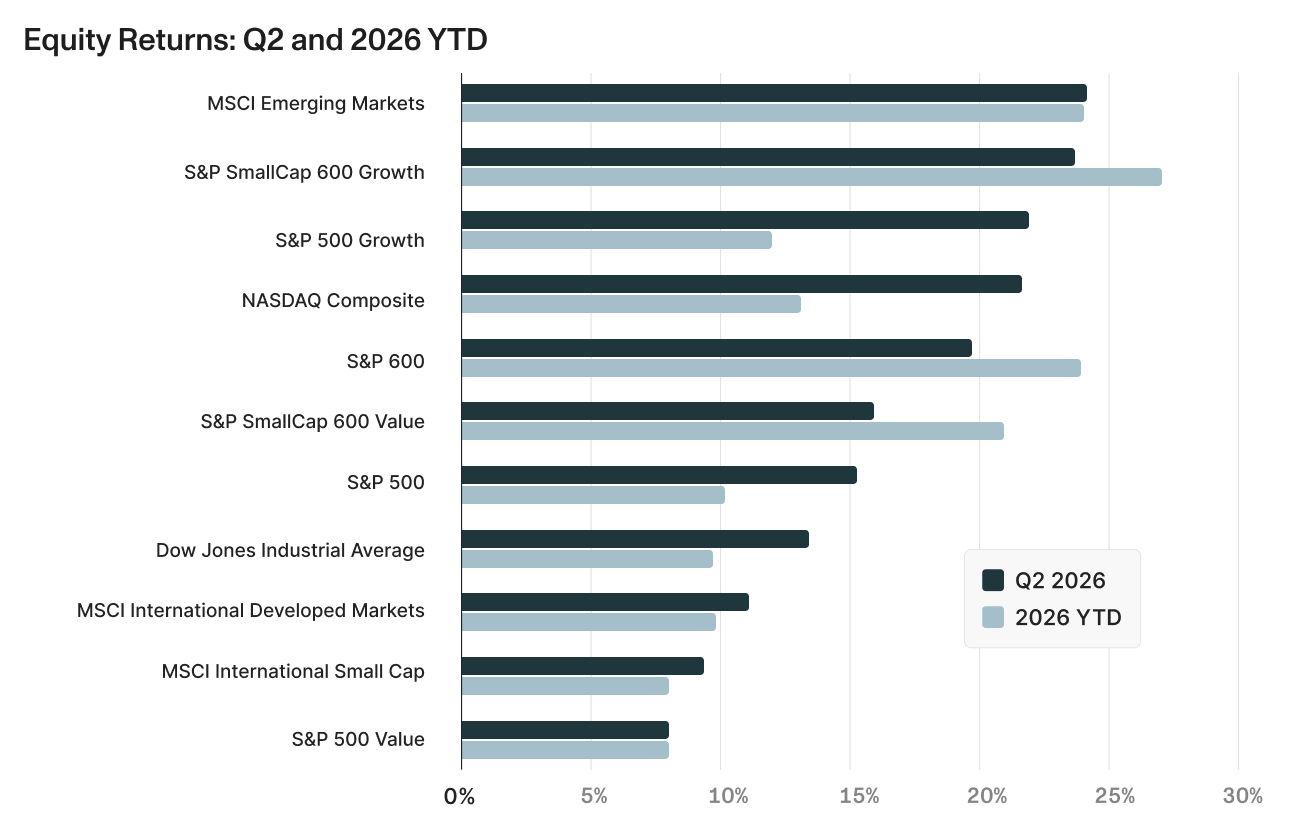

Stocks: Broadening Beneath the Surface

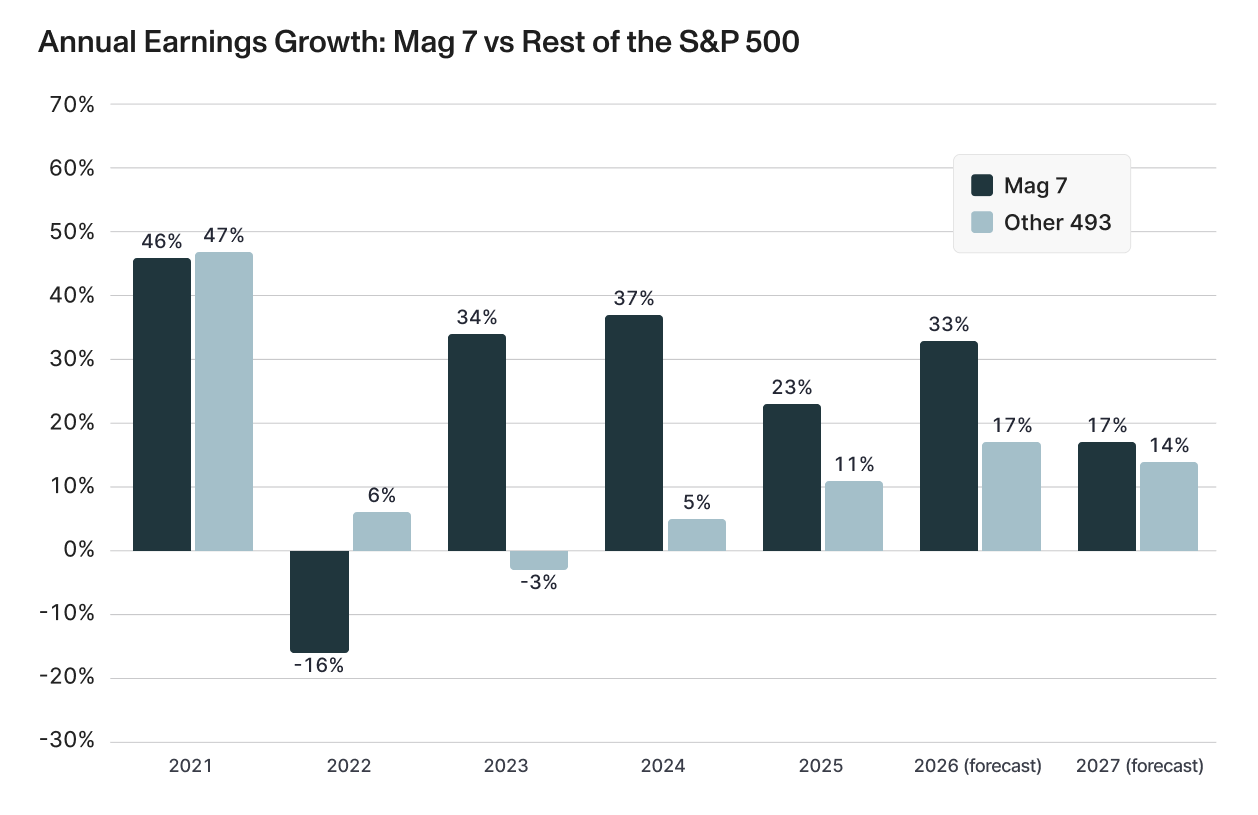

Although the S&P 500 finished the quarter near record highs, leadership beneath the surface continued to evolve. The Magnificent Seven collectively lost more than $2 trillion in market value during June as investors questioned whether unprecedented AI capital spending would ultimately generate sufficient returns. At the same time, performance broadened beyond the largest technology companies as investors rewarded businesses demonstrating improving earnings and identifiable beneficiaries of the expanding AI investment cycle.9

- June performance was more mixed than the full quarter, with large-cap growth, the Nasdaq, emerging markets, and international small caps pulling back while small-cap stocks, industrials, financials, health care, and the Dow posted gains.

- The second quarter was broadly positive across major equity indices, led by emerging markets, small-cap growth, large-cap growth, and the Nasdaq, reflecting continued investor enthusiasm for AI, rising earnings growth, and solid economic conditions.

- Small caps were among the strongest performers in both June and the full quarter, suggesting that market leadership began to broaden beyond the largest technology companies.

- Value stocks lagged growth stocks during the quarter, but June showed some rotation back toward value, cyclicals, and more defensive sectors.

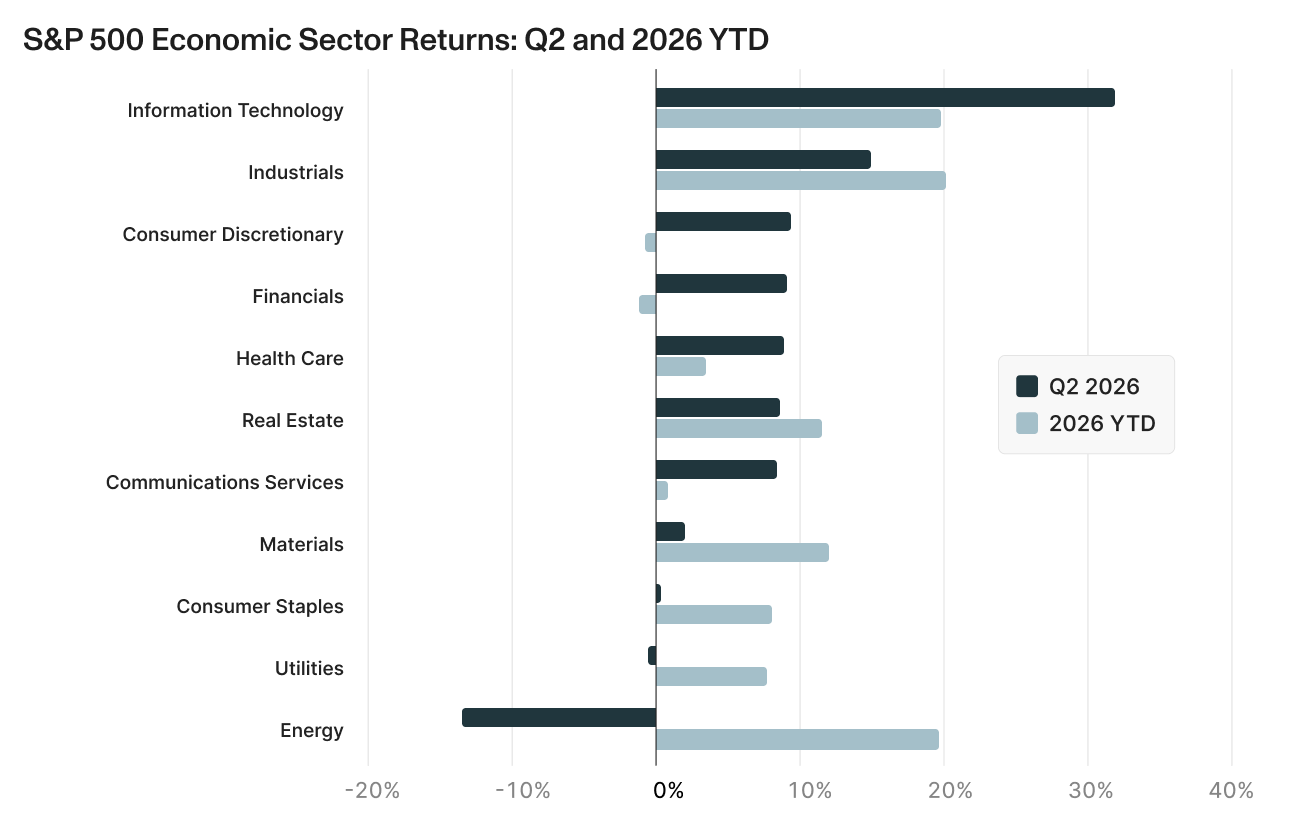

- S&P Sector returns:

- Information Technology was the clear sector leader for the quarter, supported by continued AI-related spending and rising earnings expectations, though the sector weakened in June as investors became more selective.

- Industrials, financials, health care, and real estate delivered positive June results, highlighting broader participation outside of the mega-cap technology complex.

- Energy was the weakest sector during the quarter, as oil prices retreated following progress toward reopening the Strait of Hormuz and easing concerns over global supply disruptions.

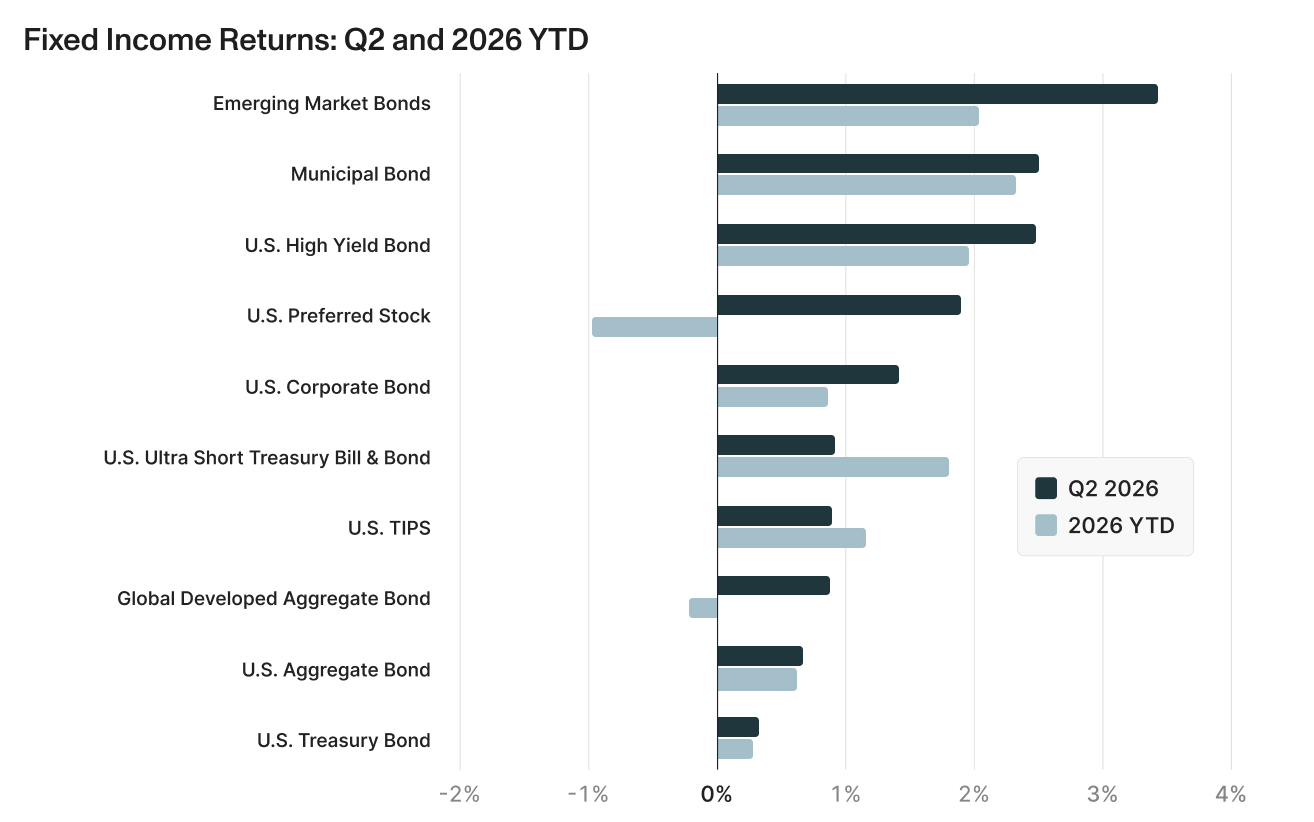

Fixed Income: Solid Returns

Fixed income markets delivered positive returns across most sectors during the second quarter despite continued uncertainty surrounding inflation and monetary policy. After yields rose earlier in the quarter as investors priced in a more hawkish Federal Reserve, bond markets stabilized in June as easing energy prices, moderating inflation expectations, and continued confidence in the economic outlook helped support high-quality fixed income.14 Elevated starting yields continued to provide attractive income opportunities while helping cushion periods of equity market volatility.

- Emerging market debt led fixed income returns, benefiting from improving global risk sentiment and a softer U.S. dollar during much of the quarter.

- Municipal bonds remained one of the strongest fixed income sectors, supported by favorable technical conditions, resilient credit quality, and attractive after-tax yields.

- Short-duration and core investment-grade bonds continued to provide stability and income, reinforcing the value of diversification as interest rate expectations evolved throughout the quarter.

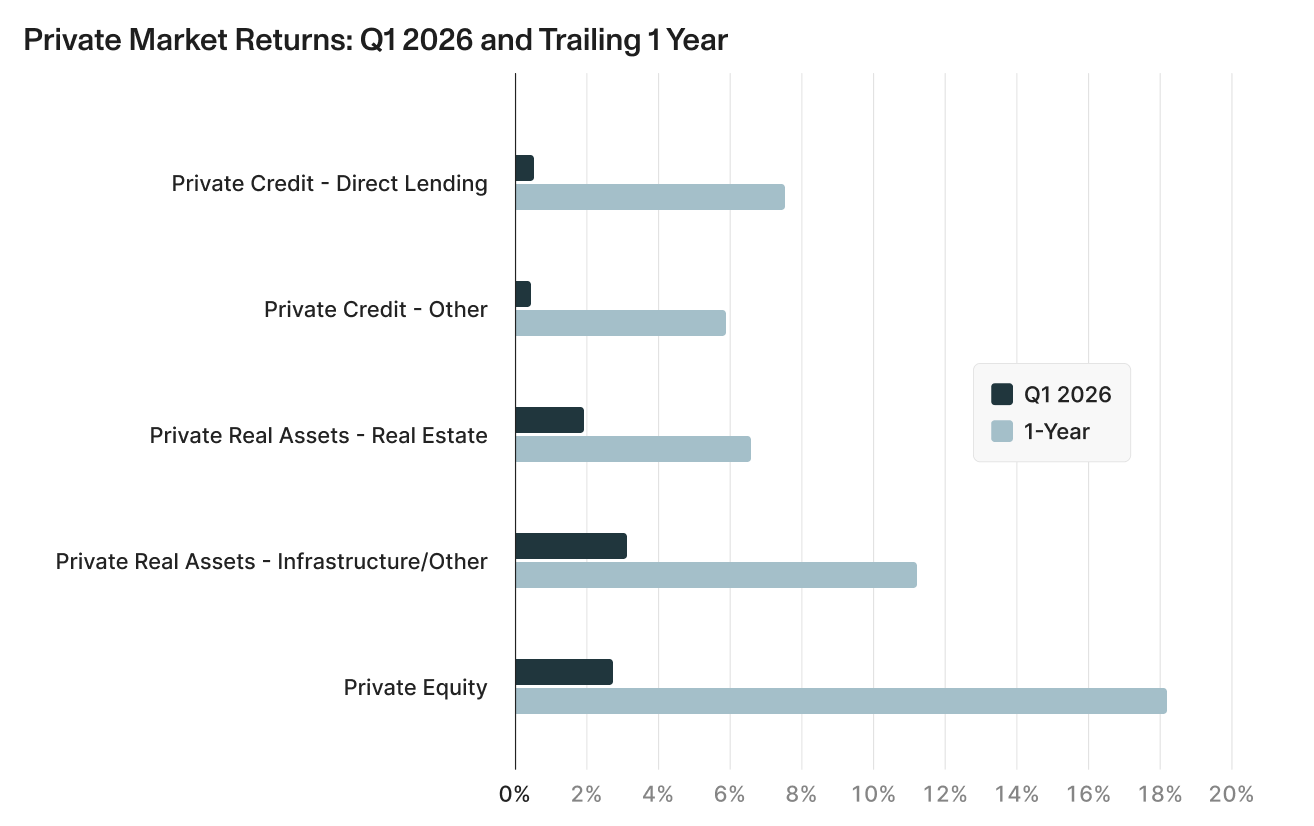

Private Markets: Expanding Opportunities

- Private Equity & Venture Capital: Private equity and venture capital activity continued to improve during the second quarter, supported by stronger fundraising, a healthier IPO market, and continued investment in artificial intelligence and digital infrastructure.16 As companies remain private longer and reach greater scale before going public, private markets continue to capture an increasing share of innovation and long-term value creation.17 The renewed IPO market, highlighted by the SpaceX listing in June and a growing pipeline of future listings, suggests capital markets are becoming more receptive to growth-oriented businesses.

- Private Credit: Private credit continued to benefit from strong institutional demand as borrowers and investors increasingly view direct lending as a permanent complement to traditional bank financing. While greater attention has been paid to underwriting standards, liquidity management, and portfolio construction, the discussion has shifted toward manager selection rather than questioning the long-term role of the asset class.18

- Private Real Estate: Private real estate continued its gradual recovery as property values stabilized and transaction activity improved across several sectors. Industrial, logistics, and data center properties remained supported by structural trends including e-commerce, supply chain investment, and growing demand for AI-related infrastructure, while office properties continued to recover more slowly. The combination of improving fundamentals and more stable valuations has created a more constructive backdrop for long-term investors.19

Key Investment Themes for the Rest of 2026

As investors look beyond second-quarter market performance, two themes increasingly shape the outlook for the remainder of the year: the path of inflation and interest rates, and the continued evolution of artificial intelligence.

Inflation, Interest Rates, and the Federal Reserve

Inflation remained one of the market's defining themes during the second quarter. While price pressures have eased significantly from their 2022 peaks, inflation has remained above the Federal Reserve's long-term target and recent readings have generally come in stronger than many investors expected. At the same time, a resilient economy and healthy labor market have given policymakers little urgency to begin lowering interest rates.

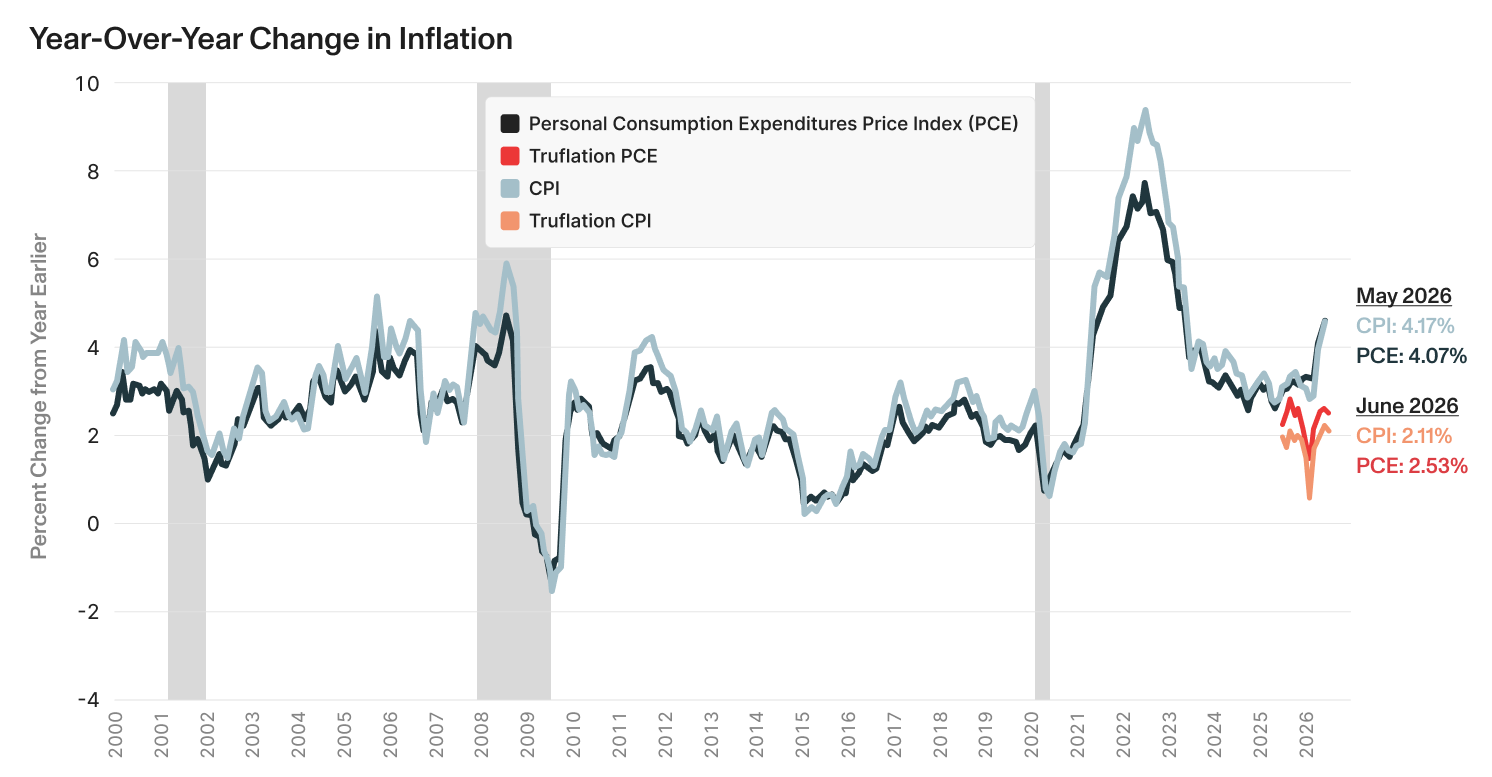

New Fed Chair Kevin Warsh has signaled a desire to look beyond backward-looking traditional inflation reports. There are now more higher-frequency measures available, such as Truflation, which tracks millions of daily price observations across the economy.22 While official measures like the Personal Consumption Expenditures (PCE) Index remain the Federal Reserve's preferred gauge because they are comprehensive and methodologically consistent, they are also published with a lag. Real-time measures can provide an earlier indication of where inflation may be heading rather than where it has been. Although Truflation’s measures suggest that underlying inflation pressures may be moderating more quickly than official data indicates, Federal Reserve policymakers will likely want to see that improvement confirmed in traditional inflation measures before considering any change in policy.

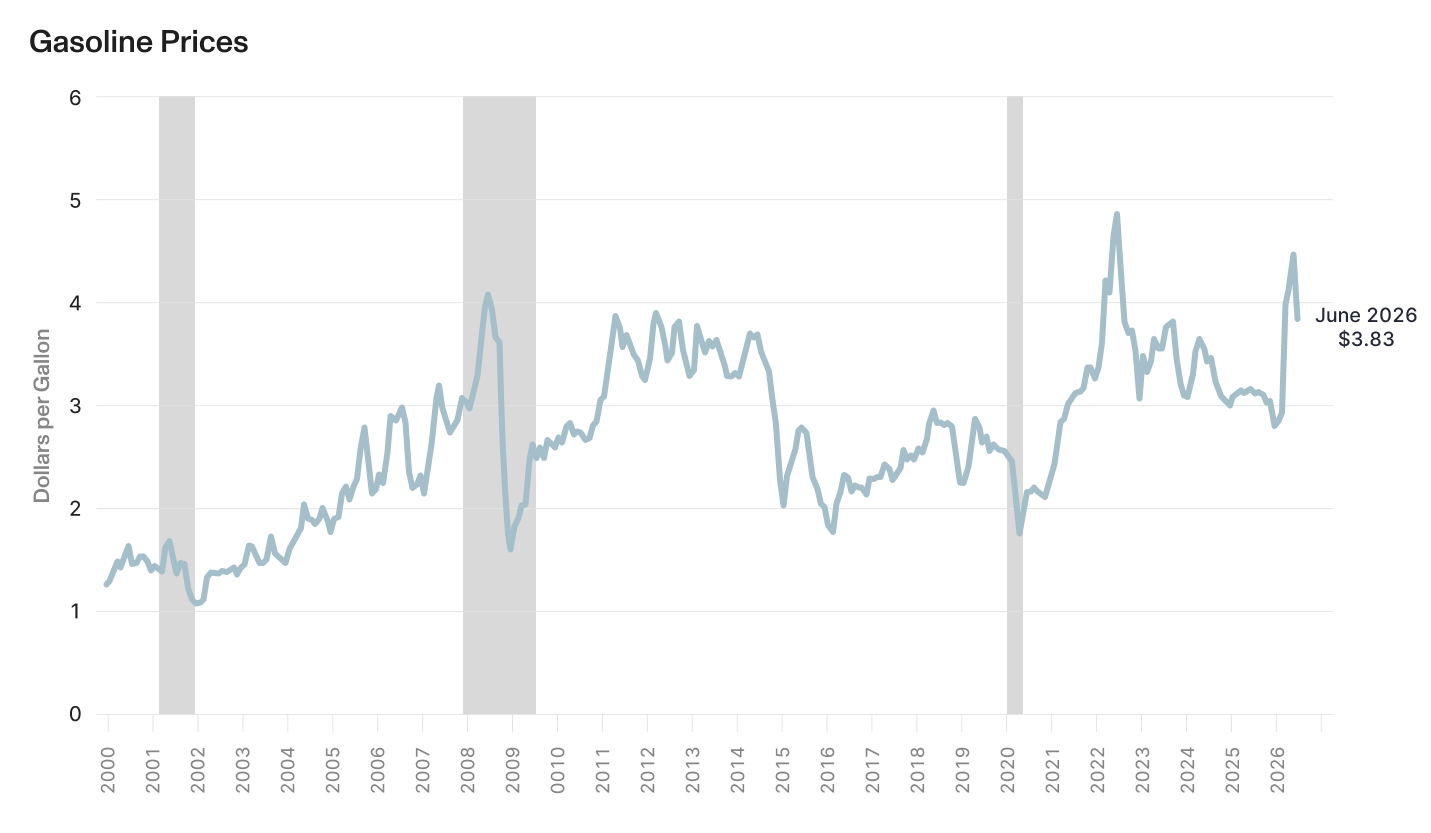

Although recent inflation reports have been firmer, there are reasons to believe some of the upward pressure may prove temporary. The conflict with Iran pushed oil and gasoline prices higher, raising concerns that energy costs could once again broaden inflationary pressures throughout the economy. Those concerns eased considerably after a U.S.-Iran memorandum of understanding helped pause hostilities and reopen the Strait of Hormuz, allowing energy prices to retreat from their recent highs.26

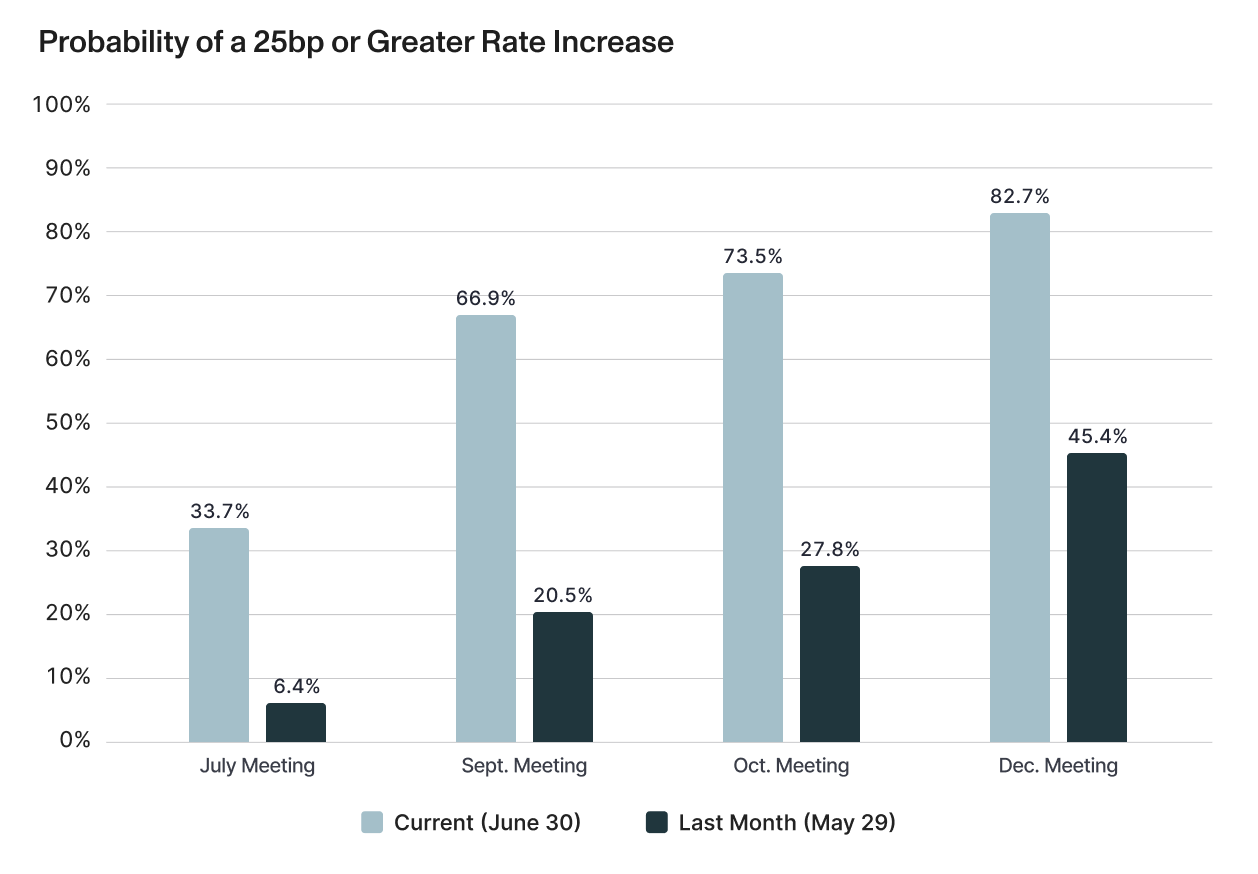

The inflation backdrop shaped the first Federal Open Market Committee meeting under Chair Warsh. As expected, the Committee unanimously left interest rates unchanged while emphasizing that policy decisions will continue to be guided by incoming economic data rather than a predetermined path.28 Compared with market expectations earlier this year, investors have increasingly concluded that interest rates may remain elevated for longer, with the probability of an additional rate increase rising substantially since the end of the first quarter.29

The Fed and Inflation — what to watch:

- Moderation in both official and real-time inflation measures that would strengthen the case for a less restrictive monetary policy.

- Indications from Fed member and Chair Warsh’s speeches of how the Fed will balance above-target inflation against a healthy labor market.

- Shifts in market expectations for future Fed rate changes.

The Next Phase of the AI Investment Cycle

Artificial intelligence continued to drive investment results during the second quarter, but the conversation surrounding AI continued to evolve. Investors are no longer asking whether AI will transform the economy — they are increasingly asking which companies will generate sustainable returns from the unprecedented capital being invested today. Early enthusiasm rewarded nearly any company associated with AI. Today's market is becoming more discerning, placing greater emphasis on earnings growth, productivity gains, and the ability to translate technological leadership into long-term shareholder value.

That shift is supported by closer scrutiny of corporate fundamentals. First-quarter earnings exceeded expectations, analysts continued raising forecasts for the remainder of the year, and earnings growth broadened beyond the largest technology companies. Still, investors also became more selective during the quarter, evidenced by a large sell-off of several of the Mag 7 names in June. Performance broadened beyond the largest technology companies as the market increasingly rewarded businesses demonstrating clear earnings growth and identifiable beneficiaries across the broader AI infrastructure ecosystem. Rather than relying on multiple expansion alone, today's market continues to be supported by rising corporate profits and improving earnings expectations.

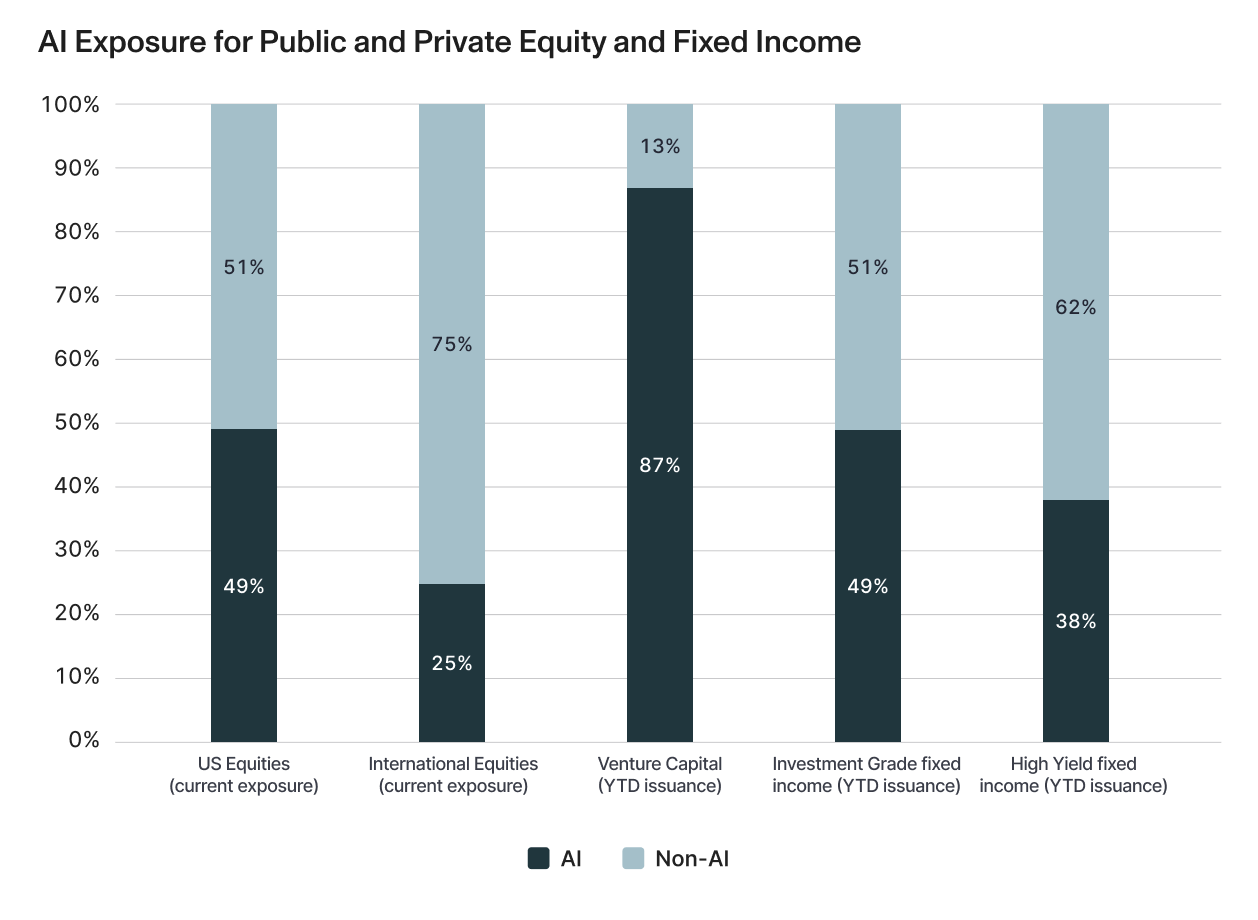

At the same time, AI has evolved from a technology innovation story into one of the largest capital deployment cycles of all time. Building artificial intelligence at scale requires far more than advanced software or semiconductor manufacturing. It requires enormous spending on data centers, electric utilities, power generation, transmission infrastructure, cooling systems, engineering, communications networks, and real estate. As a result, the investment opportunity has expanded well beyond traditional technology companies, creating beneficiaries across public equities, private equity, private credit, infrastructure, and real estate. This breadth has led to substantial exposure to AI across many asset classes.

This broader investment cycle is also changing how innovation reaches public investors. Many of today's fastest-growing companies are remaining private longer, using private capital markets to fund years of expansion before eventually accessing the public markets. SpaceX provides one of the clearest examples of this trend. By the time it became publicly traded in June, SpaceX had already grown into one of the world's largest and most strategically important companies, illustrating how an increasing share of innovation and value creation is occurring before companies ever reach a public exchange. The continued maturation of private markets alongside public markets is reshaping how investors access long-term growth opportunities.

As we enter the second half of the year, investors will be watching for evidence that today's unprecedented AI investment is translating into measurable business results. Thus far, the evidence has been encouraging. Businesses continue increasing capital expenditures, earnings expectations continue moving higher, and demand for AI infrastructure remains robust. If those trends persist, the next phase of the AI investment cycle will likely be defined less by how much companies spend and more by what those investments ultimately earn.

AI Investment Cycle — what to watch:

- Evidence that spending on artificial intelligence translates into accelerating revenue growth, higher productivity, and expanding profit margins.

- The benefits of AI expanding beyond technology companies into other parts of the economy.

- Whether AI related companies can continue increasing capital expenditures while maintaining strong earnings growth.

Looking Ahead: The Next Phase

The first half of 2026 demonstrated that markets can successfully navigate periods of heightened uncertainty when supported by strong underlying fundamentals. Despite geopolitical conflict, persistent inflation, and shifting expectations for monetary policy, corporate earnings continued to improve and economic growth proved more resilient than many had anticipated. While uncertainty is unlikely to disappear in the months ahead, investors appear increasingly focused on the factors that have historically driven long-term market returns rather than short-term headlines.

As we enter the second half of the year, several important themes will continue to shape the investment landscape. The Federal Reserve will seek evidence that inflation is moving sustainably toward its target before considering changes in monetary policy. Companies investing heavily in artificial intelligence will increasingly be judged on their ability to convert capital spending into productivity gains, earnings growth, and shareholder value. Investors will also begin looking ahead to the midterm election cycle, where changes in congressional leadership could influence fiscal priorities, tax policy, regulation, and government spending. While elections can create periods of uncertainty, markets have historically looked through changing political environments and focussed on the underlying drivers of long-term returns: economic growth, corporate earnings, innovation, and productivity.

Periods of transition often create uncertainty, but they also create opportunity. Markets rarely move in a straight line, and volatility should be expected as investors digest new economic data, corporate earnings, and policy developments. Maintaining a disciplined, diversified, and long-term investment approach remains the most effective way to navigate changing market conditions. While the next phase of this market cycle may look different from the last, the principles of successful investing remain unchanged.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.bea.gov/data/gdp/gross-domestic-product

[2] https://insight.factset.com/industry-analysts-project-21-increase-in-sp-500-price-over-the-next-12-months-1

[3] https://www.spglobal.com/spdji/en/index-family/equity/

[4] https://fred.stlouisfed.org/series/DGS10

[5] https://www.bea.gov/news/2026/personal-income-and-outlays-may-2026

[6] https://www.bls.gov/news.release/empsit.nr0.htm

[7] https://www.federalreserve.gov/newsevents.htm

[8] https://www.apolloacademy.com/lessons/2026-mid-year-outlook/

[9] https://www.spglobal.com/spdji/en/index-family/equity/

[10] https://www.spglobal.com/spdji/en/index-family/equity/

[11] https://www.msci.com/end-of-day-data-search

[12] https://www.nasdaq.com/market-activity/index/comp/historical

[13] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[14] https://fred.stlouisfed.org/series/DGS10

[15] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[16] Renaissance Capital, Q2'26 US IPO Market Review

[17] https://am.jpmorgan.com/us/en/asset-management/protected/institutional/insights/market-themes/artificial-intelligence/

[18] Cliffwater, Alternatives Roundup (June 2026)

[19] Fidelity Investments, Private Markets Quarterly Executive Summary

[20] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[21] https://www.bea.gov/news/2026/personal-income-and-outlays-march-2026

[22] https://blog.truflation.com/truflation-leading-indicator-of-the-official-bls-cpi/

[23] https://www.bea.gov/news/2026/personal-income-and-outlays-march-2026

[24] https://www.bls.gov/news.release/cpi.nr0.htm

[25] https://truflation.com/marketplace/us-inflation-rate

[26] https://www.eia.gov/dnav/pet/pet_pri_gnd_a_epmr_pte_dpgal_w.htm

[27] https://www.eia.gov/dnav/pet/pet_pri_gnd_a_epmr_pte_dpgal_w.htm

[28] https://www.federalreserve.gov/newsevents.htm

[29] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[30] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[31] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[32] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[33] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[34] https://www.apolloacademy.com/lessons/2026-mid-year-outlook/