How low will rates go?

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

The third quarter of 2025 delivered solid returns across global markets as investors navigated a complex landscape of Fed policy, persistent inflation, evolving trade dynamics, and a government shutdown. Equity markets pushed to new highs driven by strong corporate earnings and the Fed's first rate cut since December. Beneath the surface, however, more questions are developing. Most notably how much and how fast will the Fed ease rates? The evolving answer is important because of the apparent disconnect between market expectations for aggressive Fed easing and the central bank's more cautious guidance. Other questions center around the continued evolution of the extraordinary capital spending on AI infrastructure and the path to profitability, and just how broad and deep the impact of government shutdown will be. As we look toward the final quarter of 2025, understanding these forces will be essential for investors seeking to position portfolios appropriately.

We will explore these questions later in this month's market update, but first…

Last quarter at a glance

- Market Performance: Equity markets continued to push higher led by strong returns from technology and AI related stocks.1 Bond returns were also strong on generally falling interest rates although longer-term rates rose to end the quarter and remain relatively high.2

- Private Markets: IPO activity picked up substantially in the third quarter with 64 IPOs raising $15 billion, the largest quarterly new issuance since 2021. 24 of the IPOs raised at least $100 million, also a high mark since 2021. Performance was strong during the quarter, with the Renaissance IPO Index up 11% in Q3.3

- Trade Policy Developments: While tariffs continue to evolve, investors seem to be less reactive to each new development. In September, President Trump announced new tariffs including 25% on heavy trucks, 50% on kitchen cabinets and bathroom vanities, and 15% levies on branded or patented pharmaceutical products. While tariffs imposed earlier in the year haven't raised inflation as much as many expected, they are likely squeezing margins, particularly among small businesses.4

- Federal Reserve: The Fed cut interest rates by 25 basis points on September 17. The widely expected move lowered the Fed Funds target to a range of 4.0 to 4.25%. The newest Fed governor Stephen Miran was the only dissent, favoring cutting 50bps. The Fed member’s updated economic projections (the “dot plots”) suggest two more 25 basis point cuts in 2025 (at the remaining October and December meetings), one cut in 2026, and one in 2027. In his press conference, Fed Chair Powell characterized the cut as a "risk management" move, noting that "downside risks to employment have risen".5

- Government Shutdown: The U.S. government shutdown began at midnight on September 30. While historical precedent suggests brief shutdowns have limited economic impact (averaging just a few days among 21 shutdowns since 1950), this shutdown poses heightened risks given deep political divisions, an economy already vulnerable to tariff-related shocks and slowing job growth, and the potential disruption to federal data collection for key indicators at a critical time when the Fed is balancing employment concerns against persistent inflation.

- Economic Data: Reports over the quarter showed inflation remains elevated above the Fed’s 2% target, with the August core PCE up 0.2% from the prior month and 2.9% above year earlier levels.6 The government shutdown means there will be no payroll employment and unemployment rate released on Oct. 3rd, but the ADP Private Payroll measure showed a loss of 32,000 jobs in September, consistent with the view of slowing employment growth.7 Consumer spending remained solid, up 0.4% in August, the same pace as July.8

- Earnings: The (almost) final earnings growth rate for the S&P 500 for Q3 was 7.9%, the ninth consecutive quarter of earnings growth for the index.9 Looking forward, the earnings growth over the next 3-5 years implied in the current S&P 500 valuation is 11%, above the 9% historical average over the past 30 years, but below the 16% implied growth reached at the peak of the dot.com bubble in 2000.10

Stocks push higher on rate cut and strong earnings

Stocks showed strong performance across all broad categories in the third quarter, boosted by a rally after the Fed's September 17th rate cut. The final weeks of the quarter were marked by increased volatility around the path of future Fed rate cuts, inflation concerns and several new tariff announcements, but solid economic conditions and better-than-expected quarterly earnings results more than offset those worries. This year’s leaders (US large cap growth, technology stocks and emerging markets) outperformed in September while performance for the quarter was more broadly based.

- Small-cap value stocks led markets for the quarter with especially strong performance in August.11

- The NASDAQ and S&P 500 Growth were close behind, rising over 11.41% and 9.80%, respectively, for the quarter on continued enthusiasm for the AI trade.

- International markets have been the year's big winners, with returns nearly double the S&P 500. For the quarter, emerging markets continued that strong performance while developed markets lagged most US indices.12

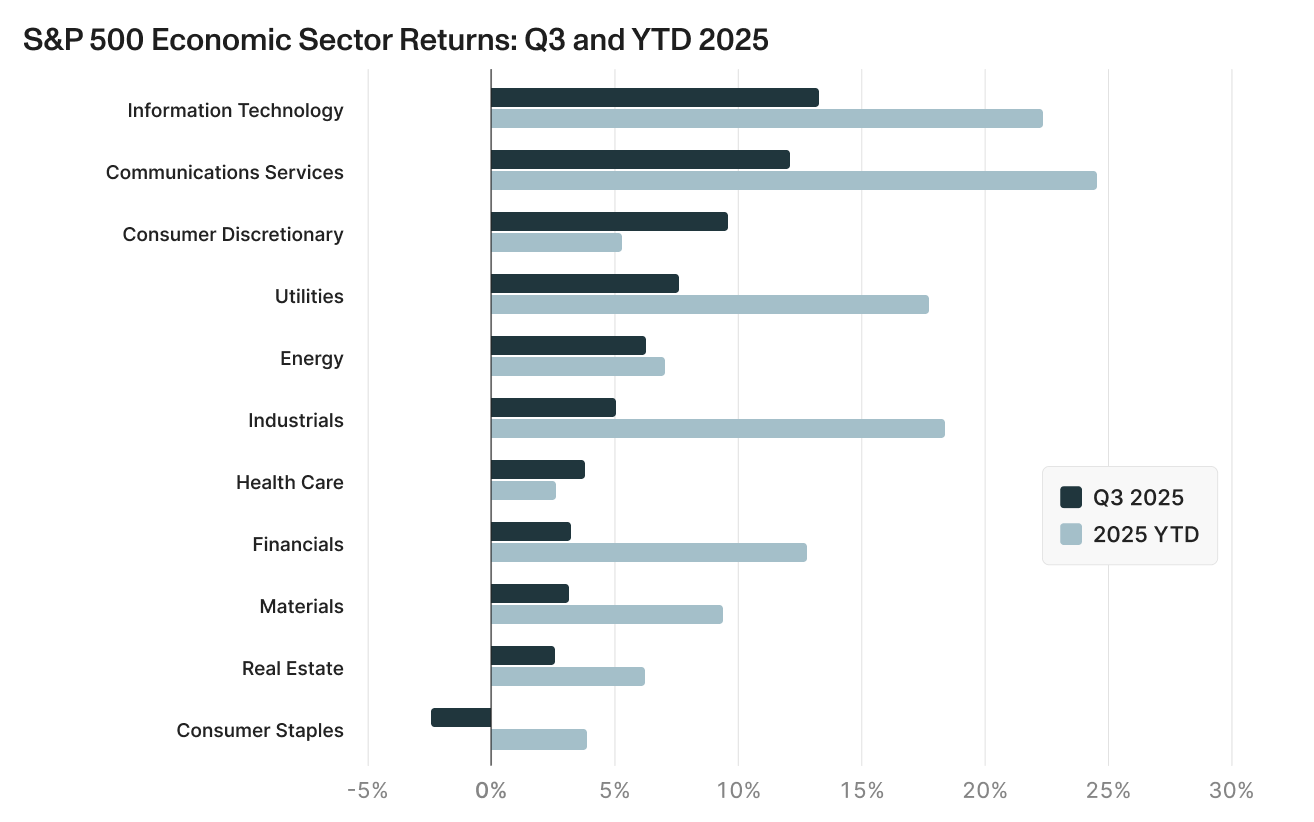

- Sector performance within the S&P 500 for the quarter returned to the patterns shown most of the year, with tech and more cyclical stocks faring best.13

- Technology and communication services continued to lead all sectors. Tech posted the strongest September (+7.25%) and Q3 (+13.19%) returns, driven by generative AI sentiment and strong earnings results.

- Consumer staples significantly underperformed, posting negative returns in both September (-1.56%) and Q3 (-2.36%) and are now up just 3.89% for the year. The sector continues to face pressure from persistent cost inflation and tariff-related margin concerns.

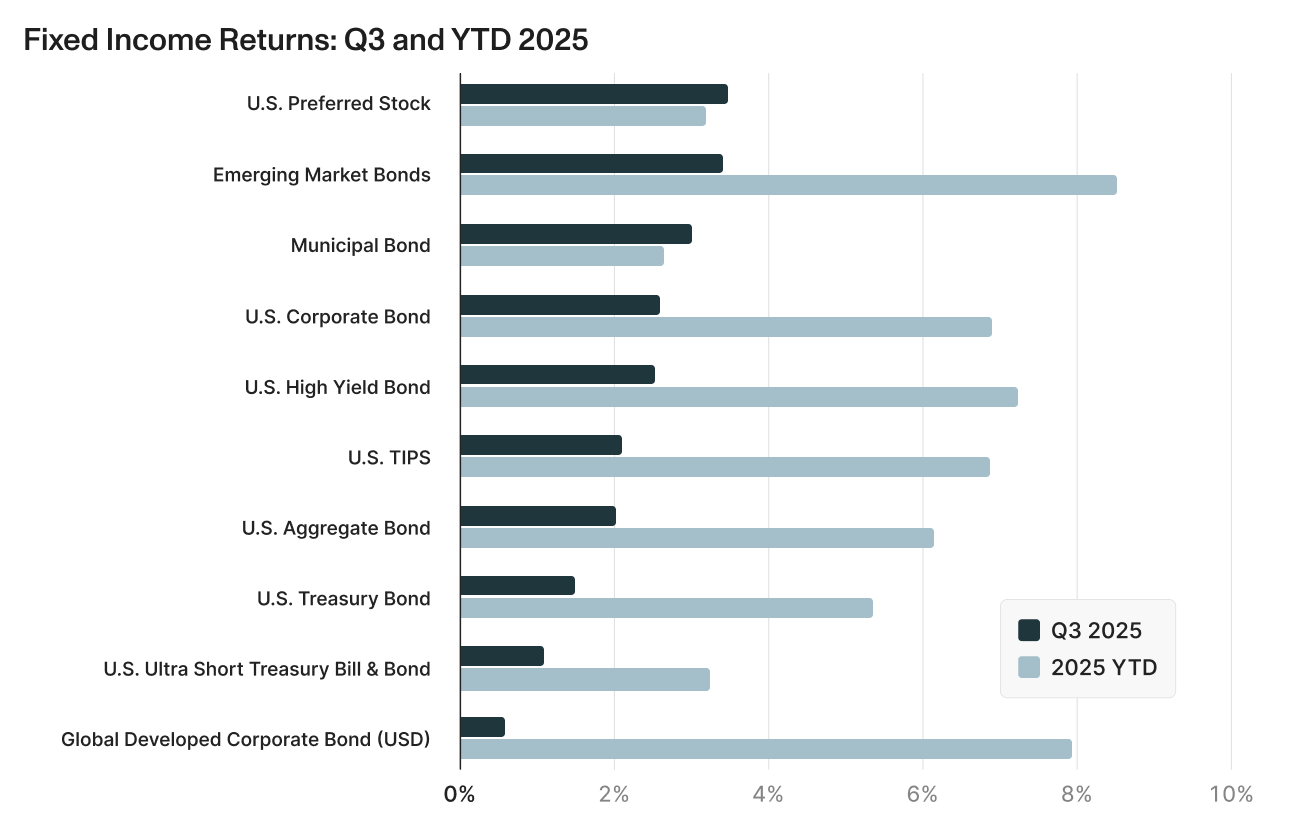

(Short) rates fall and boost fixed income

Fixed income markets posted modest positive returns in Q3 as the Fed initiated its first rate cut since December, though persistent inflation concerns and tariff-related uncertainty limited gains. Despite the Fed lowering short-term rates, these inflation worries have caused longer term rates to remain elevated. Credit spreads remain tight.18

- Credit outperformed duration as strong corporate fundamentals, reduced leverage in the private sector, and lower volatility compared to longer duration government bonds boosted results.

- Municipal bonds showed strength in September and Q3 after a very weak first half of the year. The solid returns came despite concerns about potential government shutdown impacting federal funding and causing rising state and local deficits.

- Emerging market bonds outperformed during the quarter and are the leading fixed income sector so far in 2025. Developed market bonds had a weak Q3, but are the second best performing fixed income sector for the year. Both segments benefited from dollar weakness this year.

Private Markets show steady growth

All private market asset classes showed positive performance for the quarter and first half of the year.19 The stability across private market returns during a tumultuous period demonstrates the impact of less frequent pricing and multi-year holding periods. These features have allowed private markets to show lower volatility overall and modest correlations with their public market counterparts.20

- Private equity posted a 4.3% return, its strongest quarterly result since 2021. Results were solid across equity strategies, with venture capital showing a notable rebound after several quarters of weakness. Exit activity remains limited creating challenges for investors to capture these returns.

- Private credit continued to show solid returns, rising at a slightly higher rate than in Q1. Direct lending funds outpaced other credit strategies.

- Real-asset funds posted positive returns, led by infrastructure’s 3.75% Q2 gain. Real estate funds rose 1.3% for the quarter, a welcome change in the face of continued refinancing pressures and valuation uncertainty and mostly negative quarters since 2021.21

Looking forward: Key areas to watch

1. Rate cut expectations

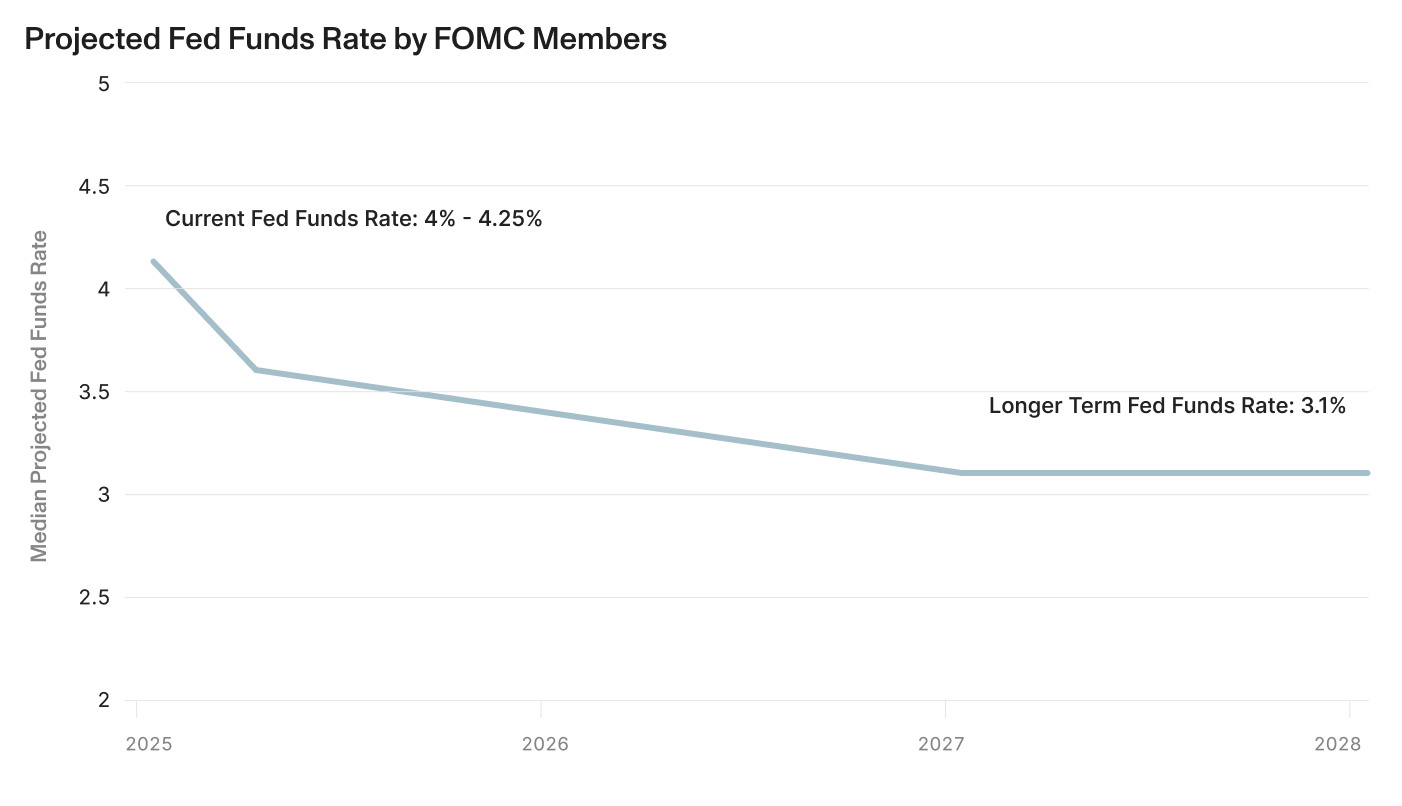

There is a notable divergence between current market expectations for rate cuts and the most recent Fed guidance. The Fed's “dot plot” projections from September 17 suggest two more 25 basis point cuts in 2025 (at the October and December meetings), one cut in 2026, and one in 2027, leaving rates at 3.0% to 3.25% (or a median of 3.1% as shown in the chart) when normalization finishes. Markets are pricing in the same 2 cuts in 2025 but 3 more by end of 2026, more aggressive than the Fed's projected path.

The reason for the divergence is uncertainty around inflation and employment, the Fed’s dual mandates. So far, it appears that corporations are absorbing most of the costs of the tariffs, but if that changes, inflationary pressures could rise. On the employment front, with companies absorbing more costs, slowing hiring is a natural response, but may not indicate the kind of weakness that would prompt a more aggressive rate cutting path.

Another uncertainty is the evolving makeup of the Fed board. New Governor Stephen Miran's dissent in September — where he favored a 50 basis point cut versus the 25 basis points delivered — suggests at least one Fed member sees the need for more aggressive action to support employment. Miran has also highlighted the Fed’s “third mandate” to maintain moderate long-term interest rates. Most current FOMC members ignore this mandate, but if a new Fed chair attempts to suppress long-term rates while inflation remains above target and the economy is near full employment, bond markets could sell off sharply.22

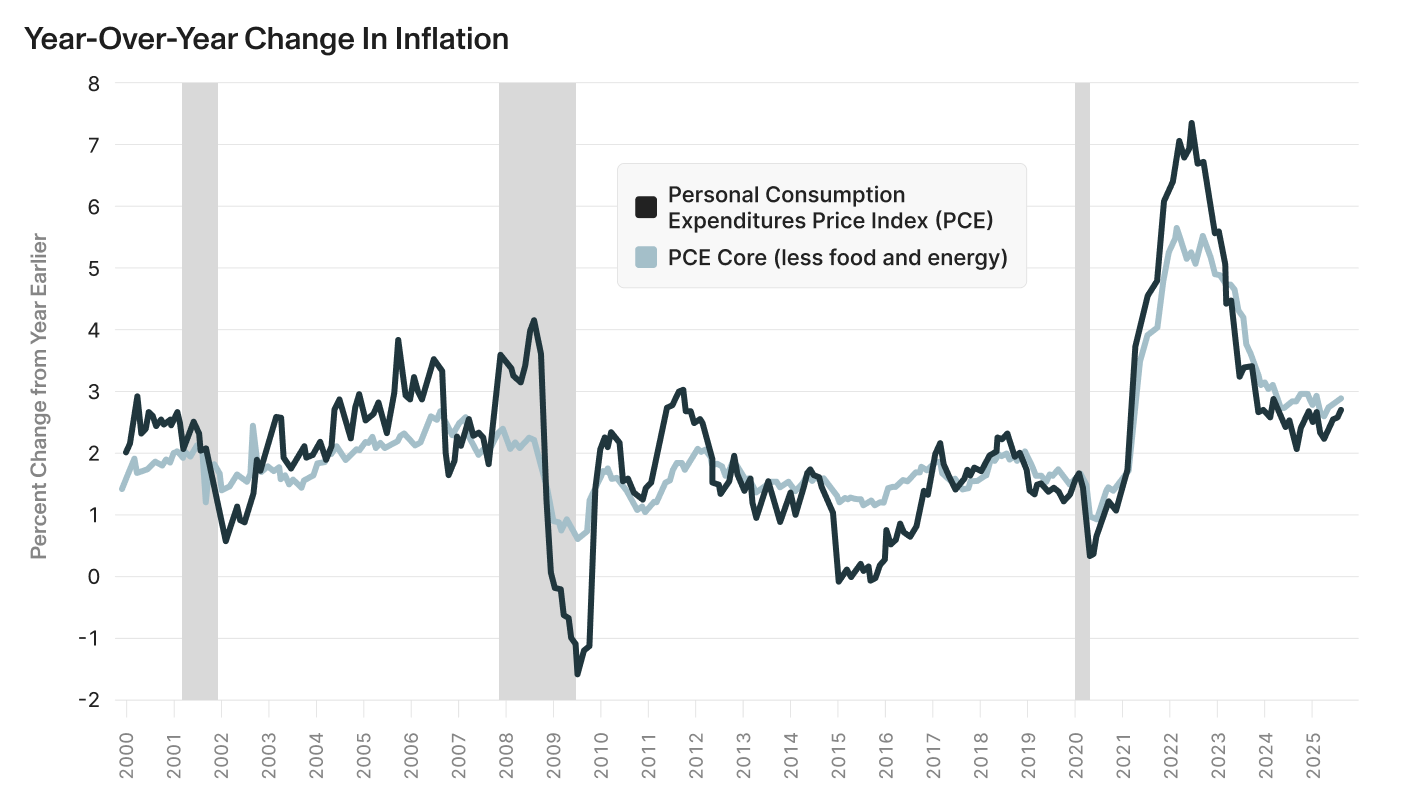

Persistent inflation remains the primary constraint on aggressive rate cuts. Both total and core PCE inflation has ticked up over the past several months when compared to year earlier levels.24 Currently at 2.9%, PCE inflation has been above the Fed's 2% target for over 50 months and is expected to remain elevated until 2028. Notably, 72% of CPI components are growing faster than the Fed's 2% target.25 Looking forward, short-term inflation expectations are significantly elevated at 3.3% over the next year, gradually declining to 2.69% over four years. This inflation picture suggests deep Fed cuts appear unlikely unless the labor weakens further.

The labor market presents a mixed picture that limits the case for aggressive easing. The August jobs report showed only 22,000 nonfarm payrolls added versus 75,000 expected, with the unemployment rate rising from 4.2% to 4.3%.27 Weekly initial jobless claims spiked to 263,000, though some of the weakness was attributed to large layoffs at ConocoPhillips and Halliburton in Texas.28

The more timely, but often more volatile, private sector employment report from ADP showed that the economy shed 32,000 jobs in September. Commenting on the September report, ADP’s chief economist Dr. Nela Richardson noted that, “U.S. employers have been cautious with hiring.”29 With the government shutdown which will stall or delay the monthly payroll employment release from the Bureau of Labor Statistics, this ADP jobs report becomes a key indicator of the labor market.

Why is job growth slowing in an economy that has shown strong GDP and earnings growth? Some observers, including Fed Chair Powell have suggested that companies are in a “no hire, no fire” mode, perhaps in response to having to absorb, rather than pass on, the costs of tariffs.30 In addition, many analysts are now suggesting both labor supply and demand curves have declined, reducing "breakeven payrolls" (the job growth where the unemployment rate will remain steady) to around 50,000-100,000 jobs per month, well below historical norms.31 Fed Chair Powell, estimated this equilibrium level to be 50,000 jobs per month.32 Analysts at Carlyle suggested that in a zero net migration scenario, domestic population growth would only be sufficient to generate 19,000 net new jobs each month at full employment.33

This slower job growth equilibrium, rather than seeing increased layoffs, combined with strong corporate profits, suggest the economy is not on the verge of recession, limiting the urgency for aggressive easing.

At this stage, it seems likely that the Fed will deliver less easing than markets currently expect. The path forward depends heavily on whether inflation proves stickier than expected and whether the labor market truly deteriorates or simply stabilizes at a lower equilibrium. This suggests that regardless of the near-term path of rate cuts, longer-term interest rates are likely to remain elevated due to persistent inflation concerns and structural factors in the economy.

Rate Cuts — What to look out for:

- Signs of sticky inflation. Will companies pass on more of the cost of tariffs? Will surveys show higher longer term inflation expectations?

- Job growth. Wherever the data comes from, assessing the strength of employment relative to a possibly new lower equilibrium rate.

2. Earnings growth, especially for AI leaders

Corporate profitability remains remarkably strong despite recent concerns about weakening labor market and a broader economic slowdown. Market-implied long-term S&P 500 earnings growth currently stands at 11%, above its historical average of 9%, but below the levels reached during the Dot Com Bubble. There really are few, if any, signs of corporate earnings deteriorating. Much of the strength has come from the astounding earnings growth of AI related companies. Some analysts suggest that what may be unfolding is "a profit boom driven by rising productivity," potentially linked to early stages of AI adoption improving efficiency even before major revenue generation from AI products.34 In this scenario, investors will have more confidence that earnings will continue to support equity upside.35

Still, the earnings outlook for AI-exposed companies presents a complex picture beneath the surface optimism. Oracle's September experience provides a revealing case study of the market dynamics at play. Despite missing consensus estimates on both revenue and earnings, Oracle's stock surged 36% in a single trading session — a massive one day move for a company like Oracle. The catalyst was Oracle's announcement of a five-year, $300 billion cloud infrastructure deal with OpenAI, which increased Oracle's contract backlog by 359% to $455 billion.36

The underlying economics of this deal are instructive. To deliver on the deal with OpenAI, Oracle will need to increase its capital spending to $38 billion in fiscal 2026 and $60 billion in fiscal 2027, representing a 47% cumulative annualized growth rate from current levels. Oracle's free cash flow, which had already turned negative for the first time since 1990, will be further under pressure. This represents the central tension in AI earnings: massive revenue opportunities require even more massive capital investment, with profitability remaining elusive or distant.37

Meta's Mark Zuckerberg recently commented that his company might be "misspending a couple of hundred billion dollars" on AI infrastructure. Yet he insisted that "when it comes to AI, the risk of underinvesting far outweighs the risk of overinvesting".38 Whether it proves to be overinvesting or not, the massive spending will create demand across many industries that AI development will rely on. The capex boom is helping offset declines in other categories that drove growth in recent years, such as industrial structures and renewable energy investment.39

The concern is not that AI won't transform the economy and our lives (it will!), but rather that the path to profitability may be longer, more capital-intensive, and more uncertain than current public market valuations suggest, with significant risks that current leaders may not be the ultimate winners from the AI revolution.

Earnings — What to look out for:

- Increased stories of concern of delayed or uncertain profitability from AI investments

- Any slowing in the exceptional future earnings outlook for technology and AI related companies will hit the stock prices of those companies, and likely the overall market, very hard.

- Competition to the leading companies. In free markets, competition is usually what erodes exceptional profitability and earnings.

3. The government shutdown

The U.S. government shutdown began at midnight on September 30 after Congress failed to pass any of the 12 required annual appropriation bills, with the Senate rejecting the House's funding bill over disagreements including extensions for Affordable Care Act subsidies set to expire at the end of 2025. There have been 21 shutdowns since 1950, most lasting only a few days. The longest previous shutdown lasted 35 days from December 2018 to January 2019, during which the S&P 500 corrected 13% and 10-year Treasury yields fell 13 basis points in the 12 preceding days, with the Congressional Budget Office estimating it permanently reduced GDP by approximately $3 billion.40

Markets typically overlook brief shutdowns as they rarely affect corporate earnings directly, but this shutdown may have larger and unique risks for several reasons. The uncertainty around ongoing tariff policies and persistent inflation as well as slowing labor markets, may make the economy more sensitive to additional negative shocks. Deep political divisions over fundamental policy provisions like healthcare subsidies increase the likelihood of a prolonged impasse. In addition, the shutdown will disrupt federal agencies that collect key economic indicators on inflation and employment at a time when Fed policy is closely watching those aspects of the economy.

The shutdown could also impact investor confidence and capital flows. International investors were already allocating less to U.S. assets than in previous years due to concerns about Federal Reserve independence, global trade policy uncertainty, and rising U.S. debt burdens. A government shutdown risked accelerating this reallocation away from U.S. Treasuries and dollar-denominated assets toward alternatives like gold. Treasury yields faced competing pressures: upward from political uncertainty and deficit concerns, but downward based on historical precedent as investors seek safe-haven assets during shutdowns.

If history is any guide, the shutdown will be resolved in short order with limited impact, but the rhetoric so far suggests that this is far from guaranteed.

Government shutdown — What to look out for:

- Political stalemate in negotiations

- Widespread government job cuts beyond furloughs

Navigating the Path Forward

The third quarter demonstrated markets' remarkable resilience in the face of multiple uncertainties, but the path forward appears increasingly dependent on how several key narratives resolve. The divergence between market pricing of aggressive Fed rate cuts and the central bank's more measured guidance suggests potential volatility ahead, particularly if inflation proves stickier than hoped or if the labor market stabilizes at a new, lower equilibrium rather than deteriorating further. The extraordinary rally in AI-related stocks reflects genuine optimism about transformative technology, with a natural tension between massive revenue opportunities and the even more massive capital requirements needed to capture them, raising legitimate questions about timing and ultimate profitability. Meanwhile, the government shutdown that began on September 30th serves as a reminder that politics can create real economic consequences. Despite these crosscurrents, strong corporate fundamentals, resilient consumer spending, and continued productivity gains provide a solid foundation for markets. As we enter the final quarter of 2025, careful attention to inflation trends, labor market evolution, and the sustainability of AI-driven earnings growth will be critical in navigating what promises to be a dynamic period for financial markets.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.spglobal.com/spdji/en/index-family/equity/

[2] https://fred.stlouisfed.org/series/DGS10

[5] https://www.federalreserve.gov/monetarypolicy/fomcprojtbl20250917.htm

[6] https://www.bea.gov/news/2025/personal-income-and-outlays-july-2025

[7] https://adpemploymentreport.com/

[8] https://www.bea.gov/news/2025/personal-income-and-outlays-july-2025

[9] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q2

[11] https://www.spglobal.com/spdji/en/index-family/equity/

[12] https://www.msci.com/end-of-day-data-search

[13] https://www.spglobal.com/spdji/en/index-family/equity/

[14] https://www.spglobal.com/spdji/en/index-family/equity/

[15] https://www.msci.com/end-of-day-data-search

[16] https://www.nasdaq.com/market-activity/index/comp/historical

[17] https://www.spglobal.com/spdji/en/index-family/equity/

[18] https://www.spglobal.com/spdji/en/index-family/fixed-income/composite-global/#overview

[19] Cliffwater Alternatives Fund Report, Q3 2025

[20] https://www.carlyle.com/the-carlyle-compass

[22] Alpine Macro, “Fed Easing, ‘Third Mandate’ And Financial Markets”, September 22, 2025

[23] https://www.federalreserve.gov/monetarypolicy/fomcprojtbl20250917.htm

[24] https://www.bea.gov/news/2025/personal-income-and-outlays-july-2025

[26] https://www.bea.gov/news/2025/personal-income-and-outlays-july-2025

[27] https://www.bls.gov/news.release/empsit.nr0.htm

[28] https://fred.stlouisfed.org/series/ICSA

[29] https://adpemploymentreport.com/

[30] https://www.federalreserve.gov/monetarypolicy/fomcprojtbl20250917.htm

[31] Alpine Macro, “Fed Easing, ‘Third Mandate’ And Financial Markets”, September 22, 2025

[32] https://www.federalreserve.gov/monetarypolicy/fomcprojtbl20250917.htm

[33] Carlyle, Economic Indicators, September 2025

[34] Alpine Macro, “Fed Easing, ‘Third Mandate’ And Financial Markets”, September 22, 2025

[37] https://www.carlyle.com/the-carlyle-compass

[38] https://finance.yahoo.com/news/mark-zuckerberg-says-meta-misspending-100400585.html?guccounter=1

[39] Carlyle, Economic Indicators, September 2025