Innovation Takes Flight

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

Financial markets continued their remarkable advance in May, supported by exceptionally strong corporate earnings fueled by accelerating investment tied to artificial intelligence. The S&P 500 reached new all-time highs, extending one of the strongest rallies in recent years, as first-quarter earnings results exceeded expectations across nearly every sector.1 2 Despite concerns surrounding inflation, interest rates, and geopolitical tensions in the Middle East, investors remained focused on the underlying strength of corporate America and the growing economic impact of technological innovation.

As we close out the first half of 2026, the investment landscape is increasingly defined by the intersection of three powerful forces. First, earnings growth remains robust, led by technology companies but increasingly broadening across sectors. Second, inflation remains above the Federal Reserve's target, creating uncertainty around the path of monetary policy as Kevin Warsh begins his tenure as Federal Reserve Chair. Third, artificial intelligence continues to reshape capital markets, business investment, and investor expectations, culminating in the anticipated SpaceX IPO — one of the largest and most closely watched public offerings in history. Together, these themes will help shape the opportunities and risks facing investors in the months ahead.

May 2026 at a glance

- Economic Growth: Economic activity remained resilient despite slower headline GDP growth, supported by healthy consumer spending, strong business investment, especially in AI-related infrastructure and technology spending.3

- Earnings: Q1 earnings season exceeded expectations, with earnings growth tracking nearly 30% year-over-year. More than 85% of companies reported results above analyst forecasts, marking one of the strongest earnings seasons in several years.4

- Equity markets: U.S. equities continued their upward trajectory, with the S&P 500 extending its rally and reaching new record highs during the month. Performance remained strongest in growth and technology-related sectors, driven by robust corporate earnings and accelerating artificial intelligence investments.5

- Fixed Income: Bond markets generated modest positive returns as Treasury yields declined late in the month on hopes of easing geopolitical concerns that would stabilize energy markets and moderate inflation pressures.6

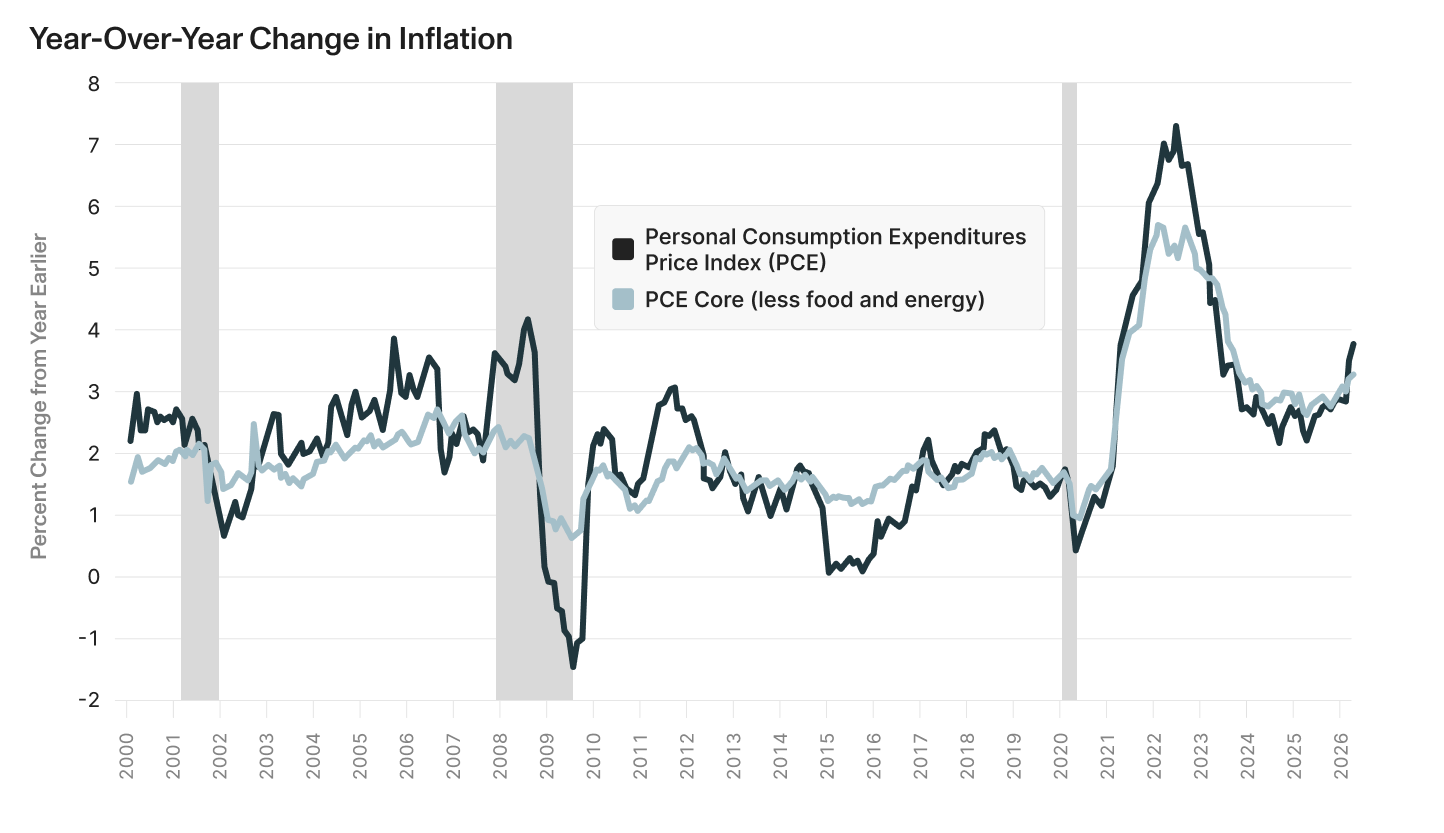

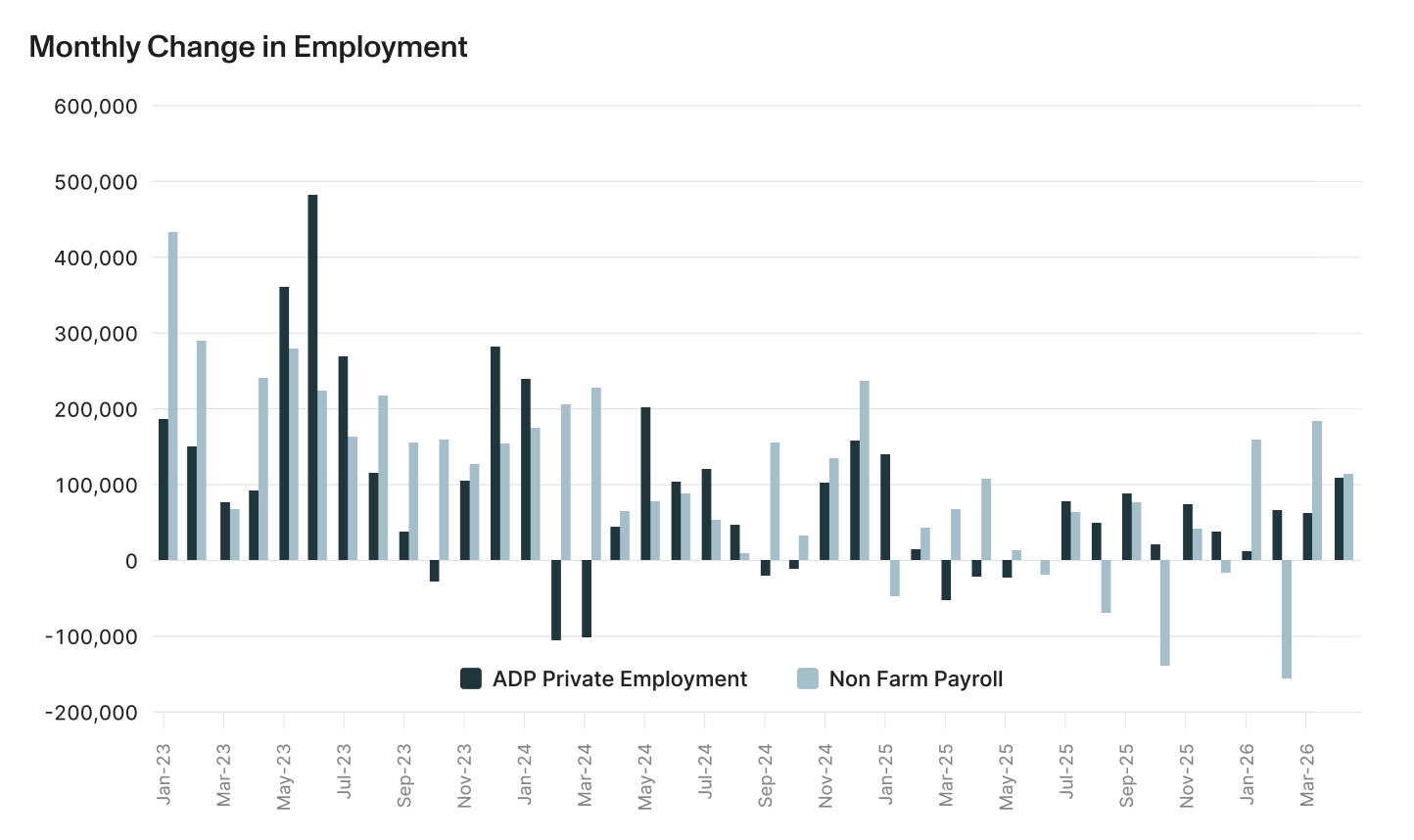

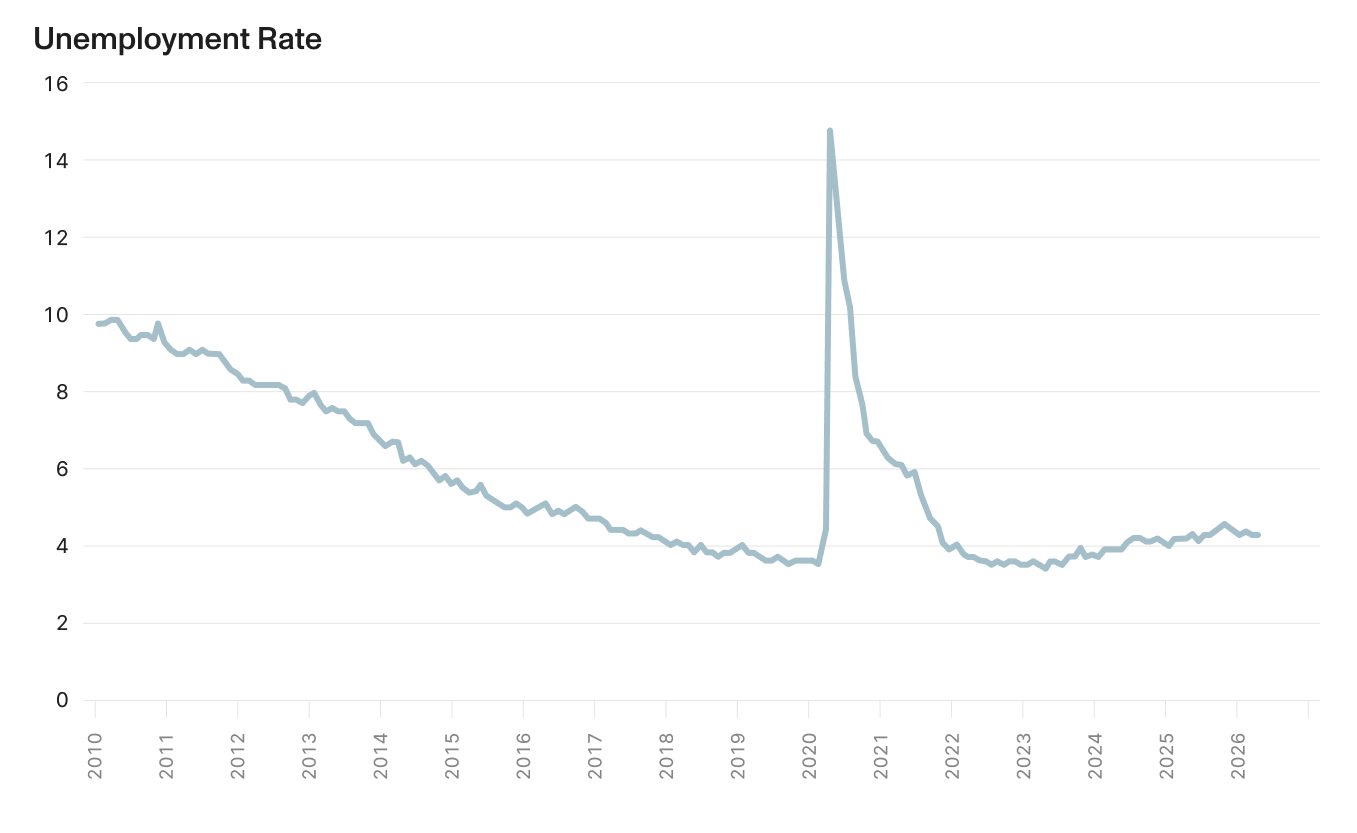

- Inflation and Employment: Inflation accelerated due primarily to higher energy prices, while labor market conditions remained stable. Unemployment remained low and job growth continued at a slower but healthy pace.7 8

- The Federal Reserve: The Fed maintained its data-dependent approach while markets increasingly focused on the transition to new Chair Kevin Warsh. Inflation has re-emerged as the primary policy challenge, creating uncertainty around the timing of future rate cuts.

- AI and the IPO Market: Artificial intelligence remains the dominant investment theme across public and private markets. Anticipation surrounding a now announced SpaceX IPO and continued AI-related capital spending helped support technology valuations and investor sentiment.

- Geopolitical risks (Iran): Tensions in the Middle East remained an important source of uncertainty, though optimism surrounding a ceasefire and the reopening of key energy shipping routes helped ease market concerns by month-end.

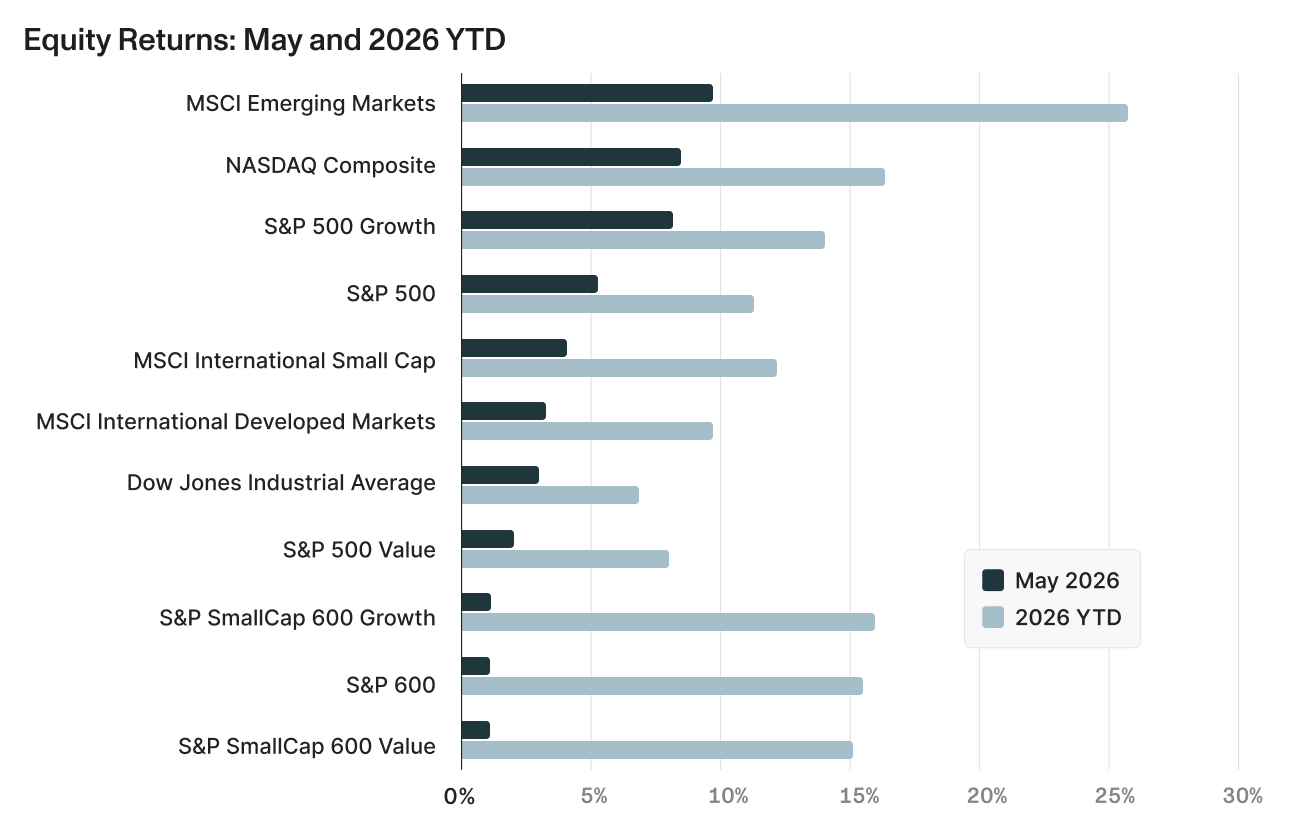

Stocks continue to rally on strong earnings and AI theme

Equity markets extended their gains in May as investors focused on strong corporate earnings, resilient economic activity, and continued exceptional AI-related investment. While inflation and Federal Reserve policy remained important considerations, the market's attention largely remained fixed on earnings growth and improving fundamentals.

- Major U.S. indices posted solid gains, led by the NASDAQ Composite and S&P 500 Growth, while the broader S&P 500 also extended its recent rally. Growth continued to outperform value during the month, though leadership has broadened across both styles on a year-to-date basis.

- Emerging markets (+9.71%) outperformed all major developed-market indices, reflecting improving global risk sentiment.

- Growth continued to outperform value in May, with the S&P 500 Growth index rising 8.09% compared to 1.96% for the S&P 500 Value index. For the year, however, leadership has broadened, with both styles posting strong double-digit gains.

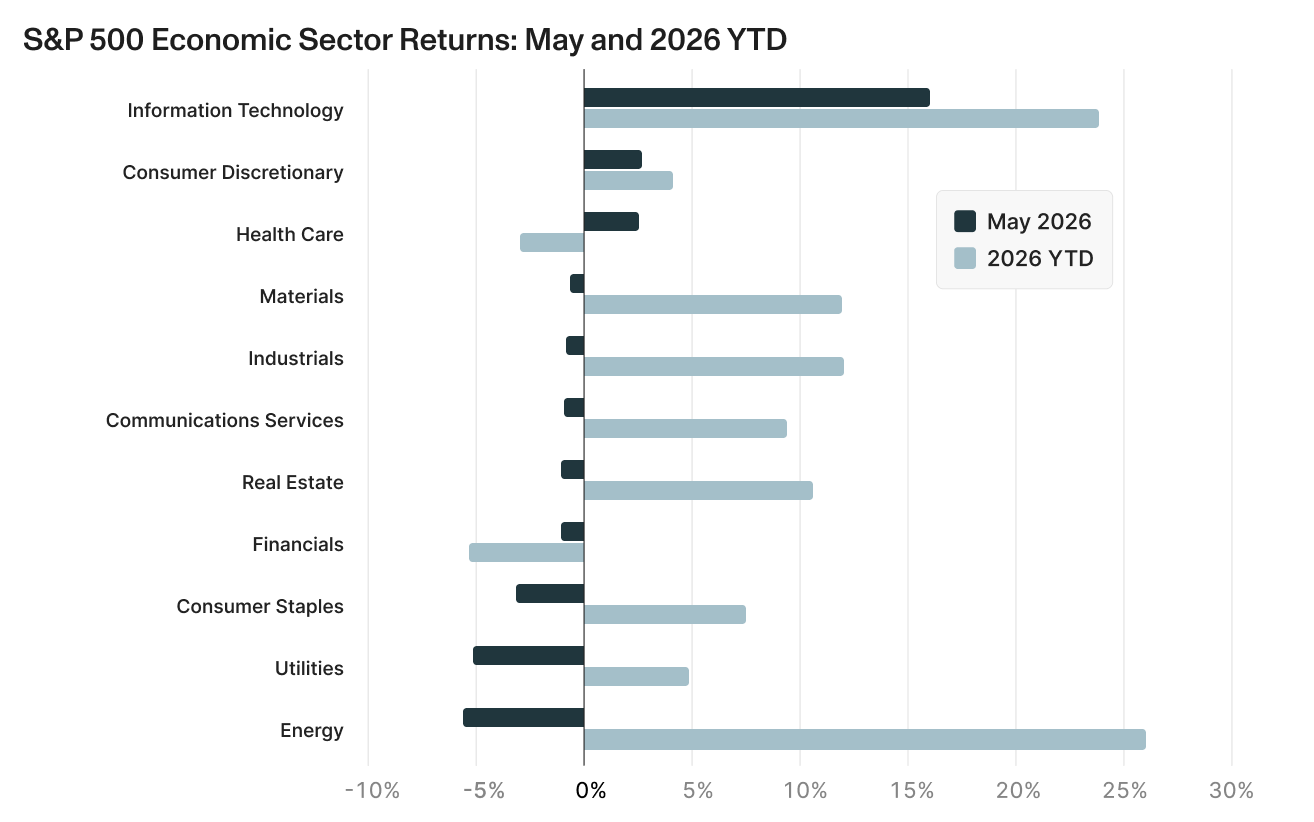

- S&P Sector returns:9

- Information Technology (+15.99%) overwhelmingly led sector performance as investors rewarded companies benefiting from a range of AI-related demand.

- More defensive sectors lagged. Utilities (-5.14%), Energy (-5.56%), Consumer Staples (-3.17%), and Real Estate (-1.05%) declined as falling oil prices weighed on energy shares and investors favored higher-growth opportunities.

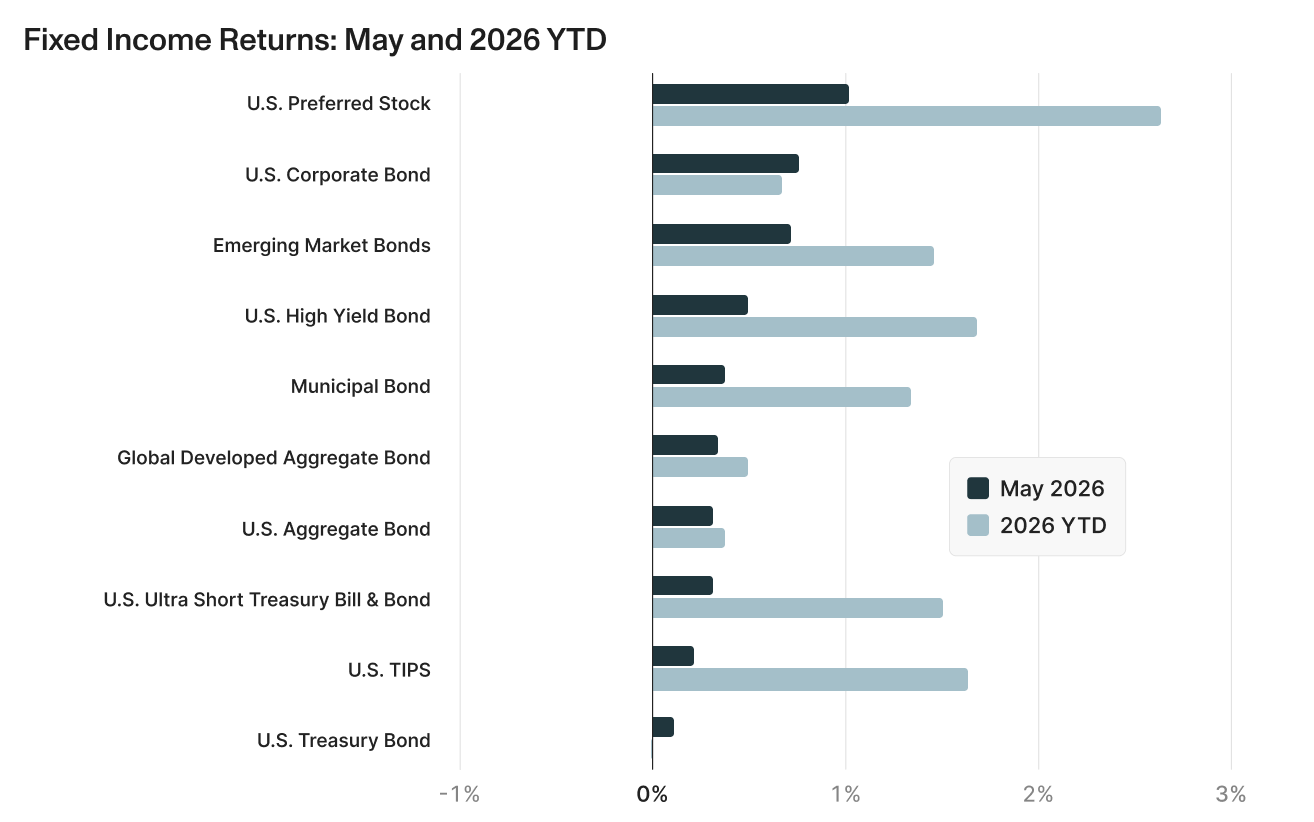

Bonds stabilize as inflation concerns ease modestly

Fixed income markets delivered positive returns in May as Treasury yields moved lower late in the month.14 Investors became increasingly optimistic that inflation pressures stemming from higher energy prices may prove temporary if geopolitical tensions continue to ease. While returns remained modest relative to equities, bond markets benefited from improving risk sentiment and stable economic conditions.

- Credit-sensitive sectors continued to lead fixed income performance, with Preferred Securities (+1.02%), Corporate Bonds (+0.76%), Emerging Market Bonds (+0.71%), and High Yield Bonds (+0.49%) posting the strongest gains.

- Core bond markets generated more muted, but still positive returns, with the U.S. Aggregate Bond Index rising 0.31% and Global Developed Aggregate Bonds gaining 0.34%.

- Treasury performance remained relatively weak. The U.S. Treasury Bond Index gained 0.11% in May, while ultra-short Treasury and cash-like investments continued to provide attractive yields with limited volatility.

Private Markets: A more selective environment

- Private Equity & Venture Capital: Private equity activity continues to be shaped by constrained liquidity and growing enthusiasm for AI-related investments. Exit activity and fundraising remain challenged, but optimism is building around a broader reopening of the IPO market. Capital is increasingly concentrated in AI, infrastructure, defense technology, and energy-related investments, while several large private equity firms have shifted focus away from traditional software holdings.16 Anticipation surrounding potential IPOs from SpaceX, OpenAI, and Anthropic has increased expectations that successful listings could help improve liquidity across venture capital and private equity.17

- Private Credit: Private credit continues to attract investor demand, supported by attractive yields and expectations for long-term growth. However, higher interest rates and slower exit activity are creating pressure for some borrowers, with default rates and unrealized losses gradually increasing.18 While structural protections in credit facilities have historically sought to insulate senior lenders, these escalating defaults signal an environment requiring strict underwriting discipline, making manager selection paramount.

- Private Real Estate: Commercial real estate continues to recover unevenly as higher interest rates drive a repricing of assets and financing conditions. Industrial, logistics, and data center properties remain among the strongest sectors, benefiting from supply constraints and growing demand tied to AI infrastructure.19 Office markets continue to face structural challenges, while multifamily and rental housing fundamentals are stabilizing.20 As a result, performance is increasingly dependent on property type, location, and access to capital.

Looking forward

The Fed's dual mandate enters a new chapter

The Federal Reserve's dual mandate is codified in legislation: maintain stable prices while supporting maximum employment. In practice, however, those objectives are becoming increasingly difficult to balance. Inflation has moved back to the forefront of the policy discussion following the surge in energy prices earlier this year. While core inflation has remained more stable than headline measures, both remain above the Federal Reserve's 2% target.21

At the same time, the labor market continues to show signs of resilience. Job growth has slowed from the rapid pace seen in recent years, but unemployment remains historically low.23 There is little evidence of a meaningful deterioration. As a result, the Fed faces an economy that is still generating growth and employment while inflation remains higher than policymakers would prefer.

This combination creates a challenging policy environment where the two sides of the mandate point in different directions. If inflation remains elevated, tighter policy may be warranted. If employment weakens meaningfully, lower rates may be appropriate. Today, neither condition is fully present. Inflation has not returned to target, but the labor market has not weakened enough to clearly justify easier policy. Importantly, policymakers must determine whether recent inflation pressures represent a temporary energy-driven shock or a more persistent challenge to price stability.

The transition at the helm of the Fed from Jerome Powell to Kevin Warsh adds another dimension to that debate. While both leaders operate under the same statutory mandate, Warsh has been more critical of the Federal Reserve's post-pandemic policy framework and has expressed a preference for a stricter interpretation of the 2% inflation target.27 He has also questioned the Fed's reliance on forward guidance and large-scale balance sheet programs, favoring a more traditional approach centered on interest rates and a smaller role for the central bank in financial markets. Investors should keep in mind that monetary policy decisions remain the responsibility of the full Federal Open Market Committee, making a dramatic shift in policy unlikely in the near term.

For investors, the key question is not whether Warsh will immediately change policy, but whether the Federal Reserve's rate setting framework begins to evolve. Markets have spent much of the past decade operating under the assumption that policymakers would tolerate temporary inflation overshoots and provide significant support during periods of stress (ie. Quantitative Easing programs). Of course, these recent decades have seen several periods of stress (GCF and Covid). Still, if the Fed adopts a more traditional approach to monetary policy under Warsh, those recent assumptions could change and investors will need to adjust to a potentially less aggressively accommodative Fed.

The Fed — what to watch:

- Will inflation move back toward 2%?

- Does employment remain resilient?

- How quickly does Warsh alter Fed communications and policy framework?

AI Momentum and the SpaceX IPO

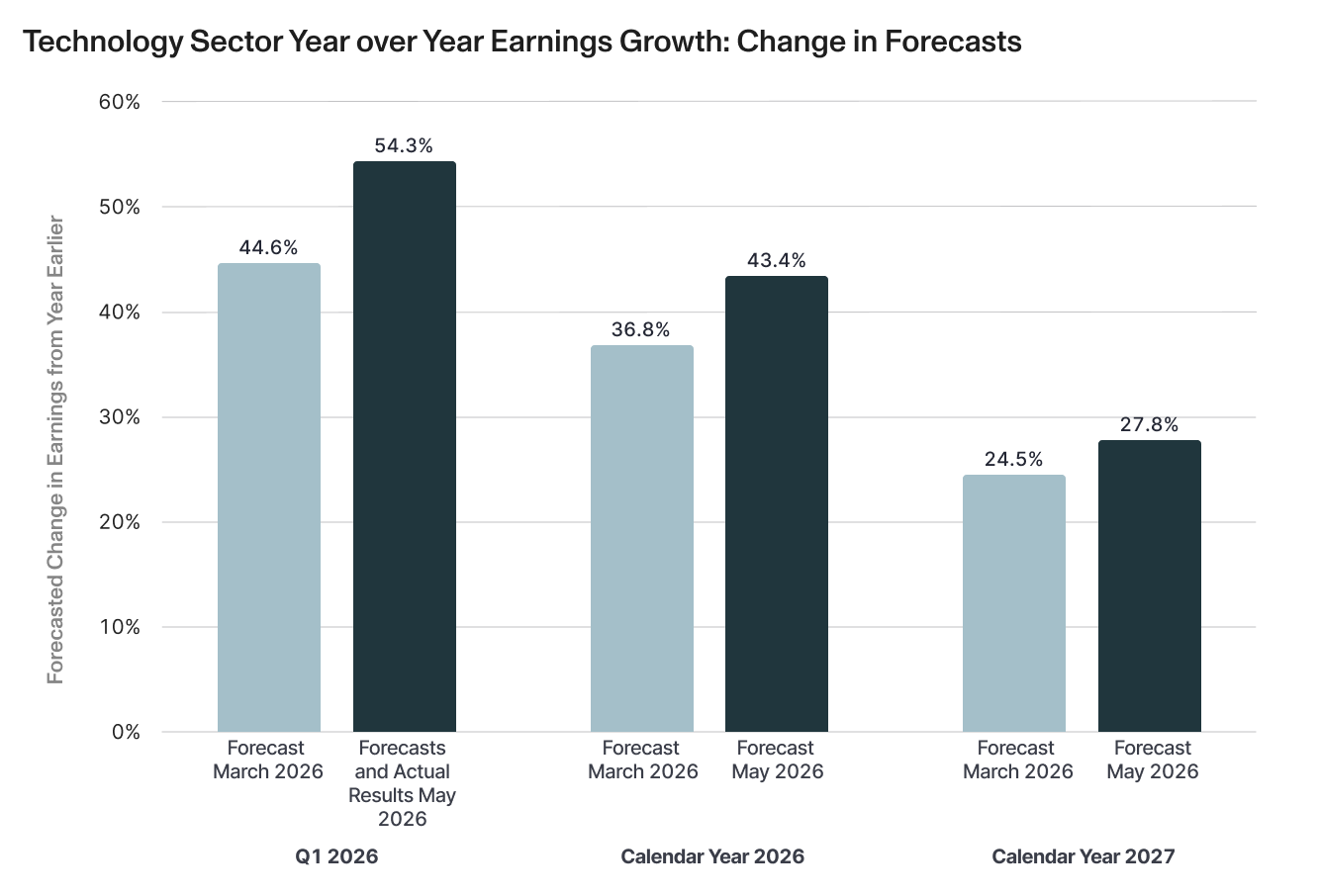

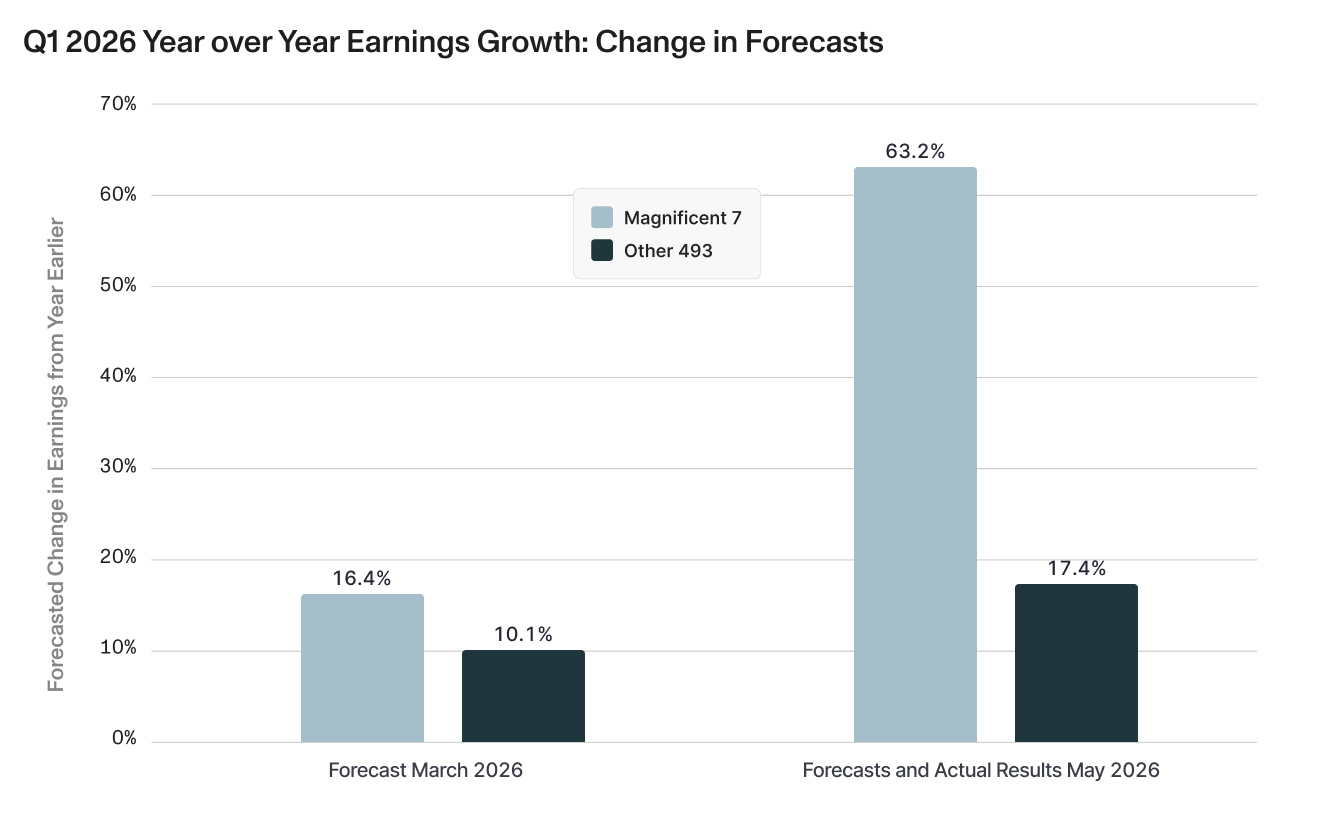

The artificial intelligence investment cycle continues to be one of the most important drivers of both corporate earnings and market performance. Technology and communication services companies once again led earnings growth during the first quarter, while analysts continue to raise expectations for many of the largest AI beneficiaries.28 Importantly, earnings leadership is beginning to broaden beyond the original "Magnificent Seven" companies and into the broader technology ecosystem of semiconductor manufacturers, cloud providers, data-center operators, software companies, and infrastructure suppliers. While valuations remain elevated in some areas of the market, much of the recent enthusiasm has been supported by tangible revenue growth, expanding profit margins, and rising capital investment rather than speculation alone.

Against this backdrop, SpaceX's anticipated IPO has become a focal point for investors. With an expected valuation of approximately $1.75 trillion to $2.0 trillion, the company would immediately rank among the largest publicly traded companies in the United States.31 Yet unlike most of today's technology leaders, SpaceX is expected to enter public markets while still reporting significant accounting losses as it invests heavily in Starship development and broader space infrastructure. Investors are therefore valuing SpaceX less on current earnings and more on its potential to dominate several emerging industries, including satellite communications, launch services, national security applications, and space-based infrastructure.32 In that respect, the company may have more in common with Amazon during its early growth years than with today's mature technology giants.33 Amazon spent years prioritizing investment and market share over profitability before ultimately becoming one of the most valuable companies in the world. Whether SpaceX follows a similar path remains uncertain, but investors appear willing to pay a substantial premium for the possibility.

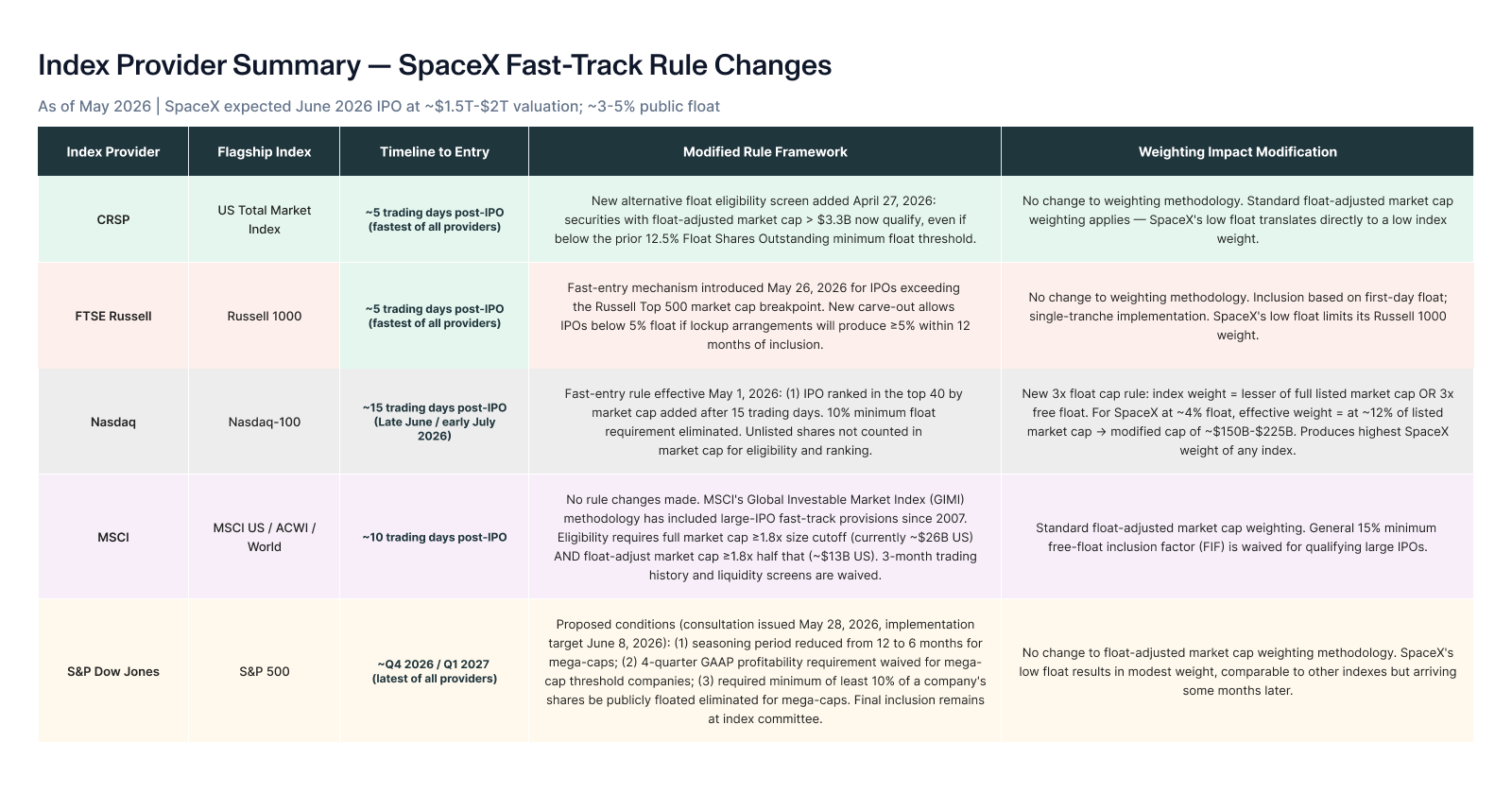

The IPO is also creating an unusual challenge for passive investors. Because the company is so large, major index providers have revised or proposed revisions to long-standing inclusion rules in anticipation of its listing. Nasdaq, FTSE Russell, CRSP, MSCI, and S&P Dow Jones have all modified or reviewed their approaches to large, low-float IPOs, accelerating the timeline under which companies such as SpaceX may enter major benchmarks.34 Initial weights of SpaceX in the indices will be based on the free float shares rather than all of the shares outstanding including those held by insiders/early investors. That difference is meaningful as SpaceX is expected to float only about 3 to 4% of its total shares at this IPO. That means the initial weight of SpaceX in the Russell 1000 Index, for example, could be around 0.1%, compared to a possible 3.2% weight based on the company’s expected full market cap.35 Over time, the initial index weights will increase toward this higher weight as the lock up periods for insider shareholders expire. SpaceX has announced staggered lock up periods starting at 70 days with full release of the non Elon Musk held shares at the standard 180 days. Musk’s 42% stake becomes unrestricted after 366 days.36 At that point, a year and a day after the IPO, the index weights are expected to evolve to reflect something closer to the full market cap of SpaceX, subject to float availability and individual index provider rebalancing methodologies.

The SpaceX offering may represent an important test for private markets and the broader innovation economy. Venture capital and growth-equity investors have faced a prolonged period of limited exits, constrained liquidity, and reduced IPO activity. A successful public offering could help reopen the market for other highly valued private companies, including firms operating at the center of the AI ecosystem. While investors should avoid extrapolating too much from a single transaction, the combination of accelerating earnings growth, record levels of AI investment, and a revitalized IPO market would represent a meaningful expansion of the themes that have driven markets over the past two years.

AI and SpaceX — what to watch:

- AI investment versus AI profits

- SpaceX valuation and execution

- The next wave of IPOs

The road ahead

As the first half of 2026 comes to a close, markets remain supported by strong corporate earnings, resilient economic growth, and accelerating investment in artificial intelligence. At the same time, inflation remains above the Federal Reserve's target, creating uncertainty around the future path of monetary policy under new Chair Kevin Warsh.

Looking ahead, investors will be watching whether earnings growth continues to support current valuations, whether inflation moves closer to the Fed's target, and whether the next generation of innovation-driven companies can sustain investor enthusiasm. The anticipated SpaceX IPO reflects both the opportunities and challenges of this environment. While uncertainty remains, maintaining a disciplined, diversified investment approach remains the best way to navigate a market shaped by both extraordinary innovation and evolving risks.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.spglobal.com/spdji/en/index-family/equity/

[2] https://insight.factset.com/analysts-making-largest-increases-in-quarterly-eps-estimates-for-sp-500-companies-since-2021

[3] https://www.bea.gov/news/2026/gdp-second-estimate-and-corporate-profits-1st-quarter-2026

[4] https://insight.factset.com/analysts-making-largest-increases-in-quarterly-eps-estimates-for-sp-500-companies-since-2021

[5] https://www.spglobal.com/spdji/en/index-family/equity/

[6] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[7] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[8] https://www.bls.gov/news.release/empsit.nr0.htm

[9] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[10] https://www.spglobal.com/spdji/en/index-family/equity/

[11] https://www.msci.com/end-of-day-data-search

[12] https://www.nasdaq.com/market-activity/index/comp/historical

[13] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[14] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[15] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[16] https://pitchbook.com/news/articles/public-pe-titans-are-saying-goodbye-to-software-hello-to-ai

[17] https://pitchbook.com/news/reports/q2-2026-forecasting-the-growth-of-north-americas-vc-aum

[18] https://www.fdi.co/markets/deep-higher-in-leveraged-credit-markets/

[19] https://irei.com/news/cw-tight-supply-cost-and-uncertainty-shift-power-back-to-industrial-landlords/

[20] https://www.connectmoney.com/stories/institutional-capital-returning-to-net-lease-select-office-assets/

[21] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[22] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[23] https://www.bls.gov/news.release/empsit.nr0.htm

[24] https://adpemploymentreport.com/

[25] https://www.bls.gov/news.release/empsit.nr0.htm

[26] https://www.bls.gov/news.release/empsit.nr0.htm

[27] https://www.cfr.org/articles/what-to-expect-from-kevin-warshs-fed-in-the-first-100-days

[28] https://insight.factset.com/analysts-making-largest-increases-in-quarterly-eps-estimates-for-sp-500-companies-since-2021

[29] https://insight.factset.com/analysts-making-largest-increases-in-quarterly-eps-estimates-for-sp-500-companies-since-2021

[30] https://insight.factset.com/analysts-making-largest-increases-in-quarterly-eps-estimates-for-sp-500-companies-since-2021

[31] https://www.investmentnews.com/practice-management/spacexs-index-fund-debut-will-look-nothing-like-what-most-investors-expect-says-jacob-friedman/266776

[32] https://www.fool.com/investing/2026/05/28/could-buying-spacex-stock-at-its-ipo-set-you-up-fo/

[33] https://bilello.blog/2026/the-week-in-charts-5-29-26

[34] https://www.schwab.com/learn/story/some-indexes-accelerate-entry-massive-ipos

[35] https://www.investmentnews.com/practice-management/spacexs-index-fund-debut-will-look-nothing-like-what-most-investors-expect-says-jacob-friedman/266776

[36] https://www.investmentnews.com/practice-management/spacexs-index-fund-debut-will-look-nothing-like-what-most-investors-expect-says-jacob-friedman/266776

[37] https://www.schwab.com/learn/story/some-indexes-accelerate-entry-massive-ipos