Sentiment vs Fundamentals

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

Markets enter the second quarter at a crossroads, with sentiment weakening meaningfully while underlying fundamentals remain broadly intact. A sharp rise in geopolitical tensions — particularly around energy markets — has pushed oil prices higher, reigniting inflation concerns and contributing to tighter financial conditions. This has, in turn, weighed heavily on both consumer confidence and investor sentiment, which have deteriorated more quickly than underlying economic data would suggest.

At the same time, equity market weakness has been driven largely by valuation compression rather than a breakdown in earnings, underscoring the disconnect between perception and reality. As a result, markets are increasingly being shaped by uncertainty, risk narratives, and shifting expectations, even as corporate profitability, investment, and overall economic activity continue to show resilience.

It is important to remember that in periods like this, investors are best served by looking beyond near-term uncertainty in order to capture longer-term opportunities.

March and Q1 2026 at a glance

- Economic Growth: Economic activity remained resilient through Q1, supported by steady consumer spending and continued business investment, particularly in AI and infrastructure.

- Earnings: S&P 500 profits are on track for another quarter of double-digit growth and full-year expectations continued to move higher. Earnings strength remains concentrated in energy and mega-cap technology, while some cyclical sectors show some emerging margin pressure.1

- Equity markets: US equities entered correction territory, with the S&P 500 down almost 5% in March, after posting five consecutive weekly losses to end the quarter.2 The drawdown was the result of multiple compression rather than earnings deterioration.

- Inflation and Employment: The labor market showed signs of gradual cooling, with softer job growth but unemployment remaining low and stable. Inflation, while still well below prior peaks, reaccelerated due to rising energy prices, pushing up short-term inflation expectations.3 4 5 6

- The Federal Reserve: The Fed held rates steady in March, adopting a clear “wait-and-see” stance as it assesses the inflationary impact of higher energy prices and evolving geopolitical risks. Chair Powell indicated that he views the shock as potentially transitory.

- Trade and tariff policy: After the Supreme Court February ruling that sharply constrained executive tariff authority, trade policy shifted to a secondary, but still persistent, source of uncertainty, especially as a contributor to elevated goods inflation.

- AI revolution questions: AI continues to be the dominant structural growth driver across markets, underpinning corporate investment, earnings growth, and capital allocation decisions. However, the pace of spending has raised questions around returns, efficiency, and sustainability.

- Geopolitical risks (Iran): The Iran conflict emerged as the defining macro risk in March, triggering the largest global energy disruption in decades and driving a sharp increase in oil prices. The closure of key supply routes, including the Strait of Hormuz, has disrupted roughly 20% of global oil flows, amplifying inflation concerns and tightening financial conditions.

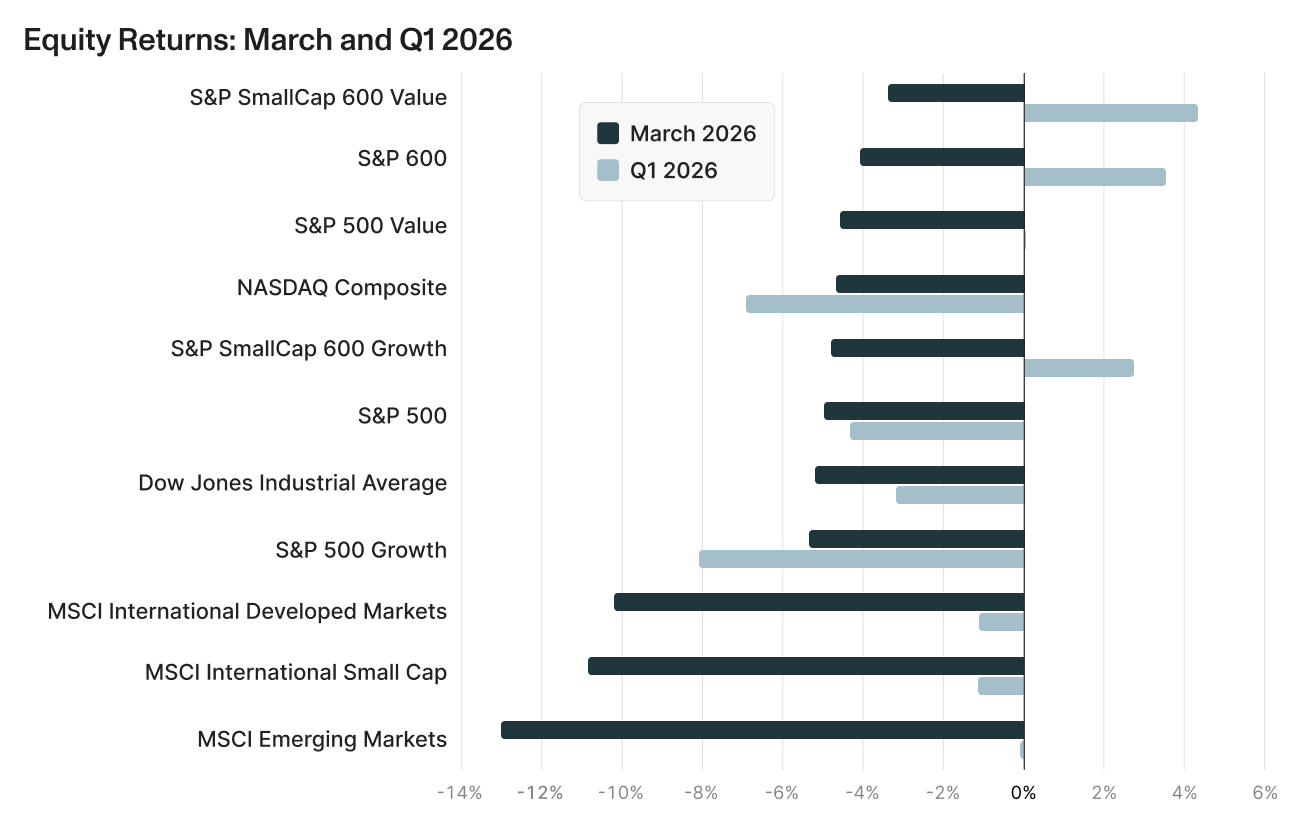

Stocks slip on geopolitical concerns

Equity markets declined in March and finished the quarter under pressure, driven primarily by valuation compression as rising oil prices and bond yields weighed on sentiment. The selloff was broad-based, though energy was a notable outperformer, benefiting from the surge in crude prices. Importantly, market weakness was driven more by shifting macro expectations than a deterioration in underlying fundamentals.

- US large cap growth stocks fell sharply in March and have seen the largest declines among major indices this year. Rising discount rates and increasing scrutiny around AI-related capital spending pressured valuations.

- U.S. Small Cap and Value stocks also fell in March, but were the best performers for the month and are still up solidly for the year.

- International developed and emerging market stocks underperformed meaningfully in March (Developed -10.2%, Emerging -13.0%), reflecting greater sensitivity to the global energy shock and weaker growth dynamics abroad.

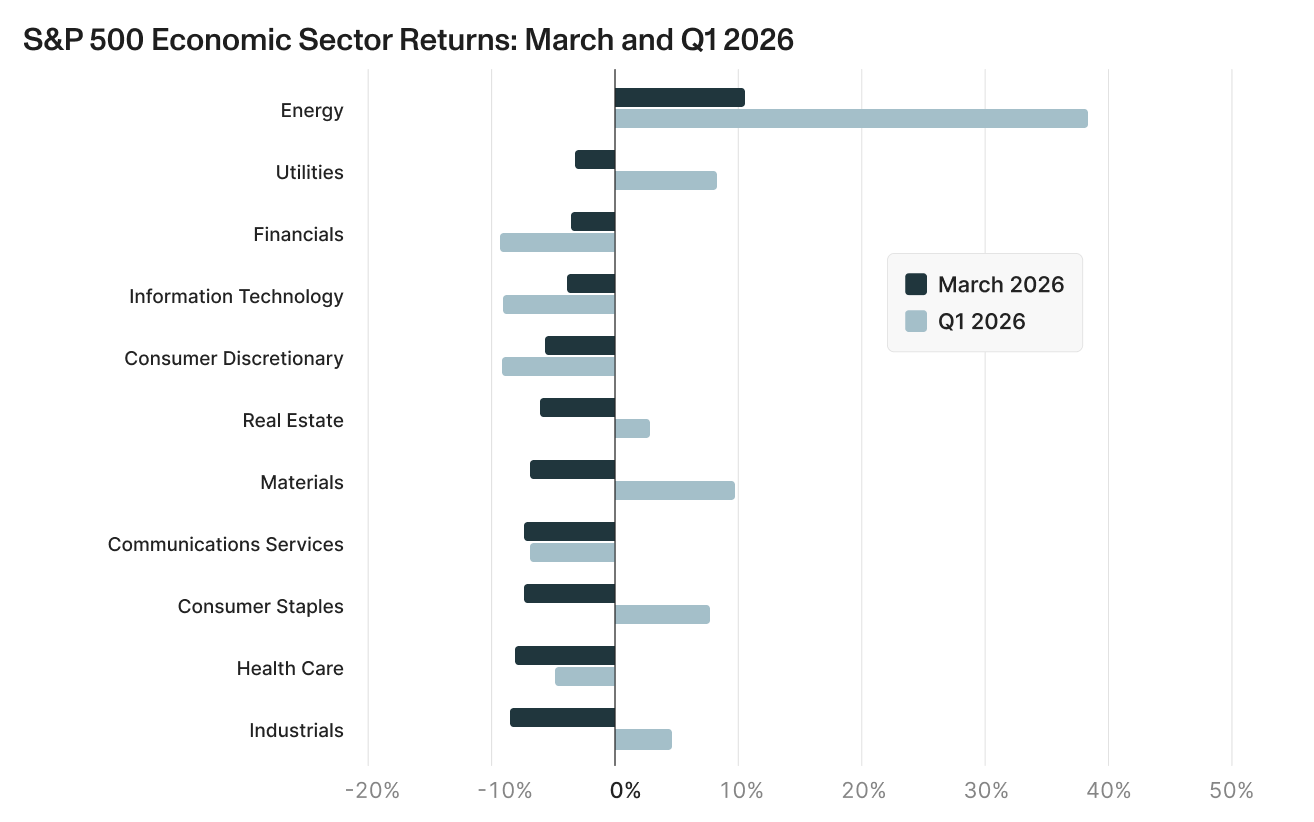

- S&P Sector returns:

- Energy stocks were the lone positive. The surge in energy prices pushed Energy up +10.4% in March and +38.3% in Q1, significantly outperforming all other sectors.

- Industrials fell the most in March on rising inflation expectations.

- Defensive sectors weaken. Consumer Staples and Health Care were among the laggards for March, but still show relatively better returns for the year.

- Growth-oriented sectors mixed. Information Technology held up a bit better than other sectors in March as their earnings growth remained solid, but the sector remains down almost 10% for the year.

- Energy stocks were the lone positive. The surge in energy prices pushed Energy up +10.4% in March and +38.3% in Q1, significantly outperforming all other sectors.

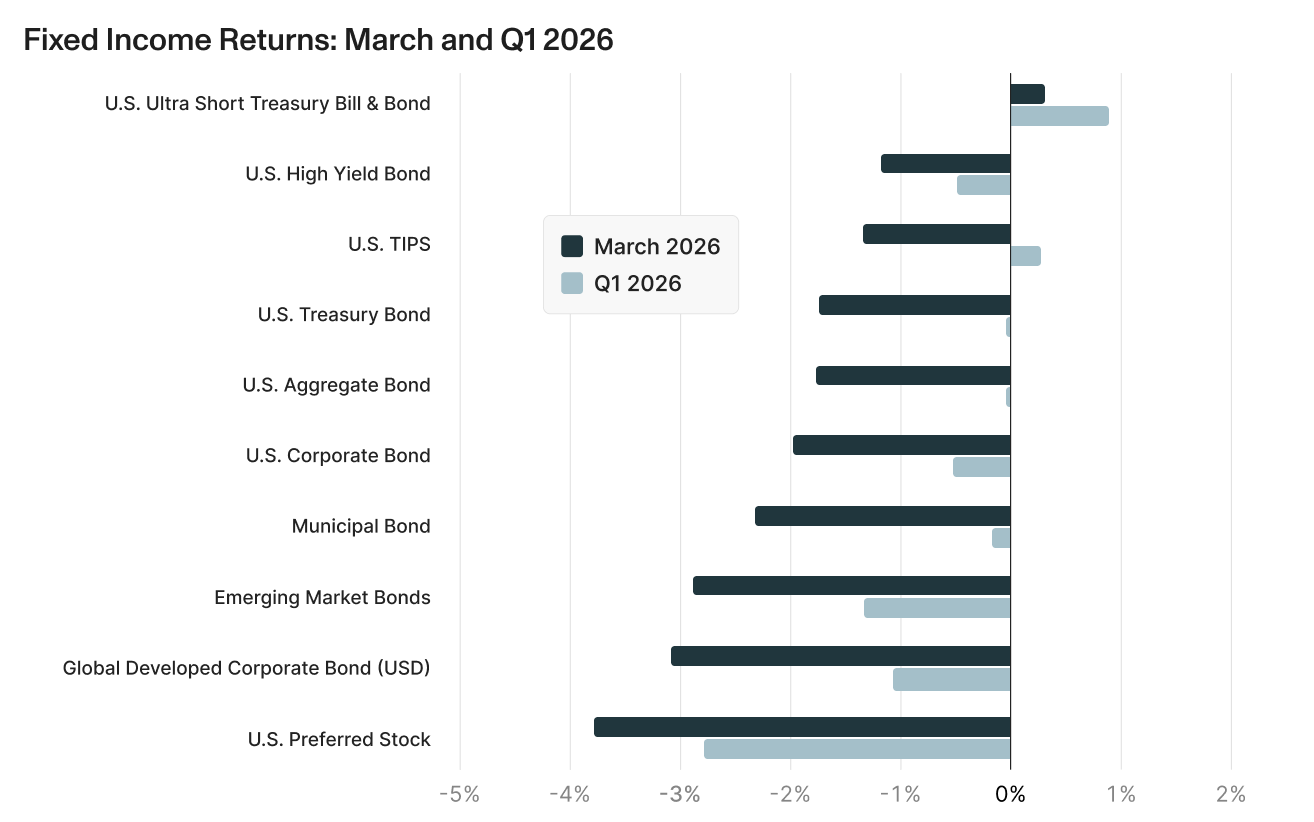

Bonds weaken on rising yields

Fixed income markets came under pressure in March as rising oil prices and inflation concerns pushed yields higher across the curve. The Bloomberg Aggregate Bond Index declined -1.76% in March, leaving returns roughly flat for the quarter (-0.05%), as the market repriced expectations for a Fed pause and fewer rate cuts this year. While credit spreads remained relatively contained, duration-sensitive assets bore the brunt of the selloff.

- Short Duration Outperformed: Ultra-short Treasuries were the lone positive performer (+0.30% in March, +0.88% Q1), benefiting from minimal interest rate sensitivity as rates moved higher.

- Rate-Sensitive Core Bonds Lagged: Core fixed income sectors declined in March, including Treasuries (-1.74%), Investment Grade Corporates (-1.98%), and Aggregate Bonds (-1.76%), as yields rose sharply.

- Spread & Global Sectors Underperformed: Higher-risk and global segments lagged, including Emerging Market Debt (-2.89% March, -1.35% Q1) and Global Developed Bonds (-3.07% March, -1.07% Q1), reflecting both rising global yields and geopolitical stress. High Yield held up somewhat better (-1.18% March) due to still-resilient credit fundamentals.

- Municipals (-2.32% March) and Preferreds (-3.78% March) also underperformed, pressured by higher rates and weaker technicals.

Private Markets: Challenges and excitement

- Private Equity & Venture Capital: Private equity activity showed signs of stabilization in Q1, supported by improving deal flow and continued capital deployment, though elevated volatility weighed on exit activity. The IPO market, in particular, lost momentum as public market weakness delayed new issuance, with just 34 deals raising ~$10 billion during the quarter.

Still, the IPO pipeline remains robust, highlighted by anticipated listings from SpaceX and OpenAI and others that could be among the largest in history. These would not be typical IPOs and represent more than a reopening of the IPO market; they reflect a transition toward public ownership of the next generation of AI and infrastructure platforms, with valuations and scale that will test the capacity of public markets.

Valuation estimates for SpaceX range from recent secondaries levels of around $800B to IPO scenarios ranging from $1.5T to $1.75T.12 At those IPO valuations, SpaceX would immediately become one of the largest publicly traded companies. Estimates for a possible OpenAI IPO are equally impressive, supported by its most recent fund raising round valuing the company at $850M.13

Retail and institutional interest in exposure to these companies is extremely high, a sign of both the strength of the innovation and growth story surrounding the companies as well as a potential sign of late-stage over enthusiasm. If they come to pass this year, these IPOs would require the public markets to absorb a tremendous amount of new equity issuance and substantially reshaping index composition.

- Private Credit: Private credit markets are facing a meaningful stress test of this cycle, as elevated redemption requests have begun to pressure semi-liquid structures. While many funds have successfully returned capital, redemption limits and proration have resulted in unmet withdrawal demand, highlighting the structural tradeoff between liquidity and return in the asset class. Despite these challenges, underlying credit fundamentals remain relatively stable, with moderate leverage and manageable default expectations. The key risk seems less about credit quality and more about liquidity dynamics and valuation transparency, particularly if investor sentiment weakens further.

- Private Real Estate: Private real estate is becoming more defined by income generation than price appreciation, as higher financing costs continue to weigh on valuations. Transaction activity has begun to recover modestly, though cap rate compression remains limited, and returns are increasingly dependent on asset-level execution. Within the sector, dispersion persists, with areas tied to infrastructure, logistics, and select residential segments showing relative resilience compared to more rate-sensitive property types.

- Democratization of Alts: While alternative investment assets remain concentrated among the largest managers, a proposed rule to allow private assets within 401(k) plans could meaningfully expand the investor base over time, creating a new structural source of demand for alternative investments.

Looking forward: Geopolitical risks cloud fundamental strength

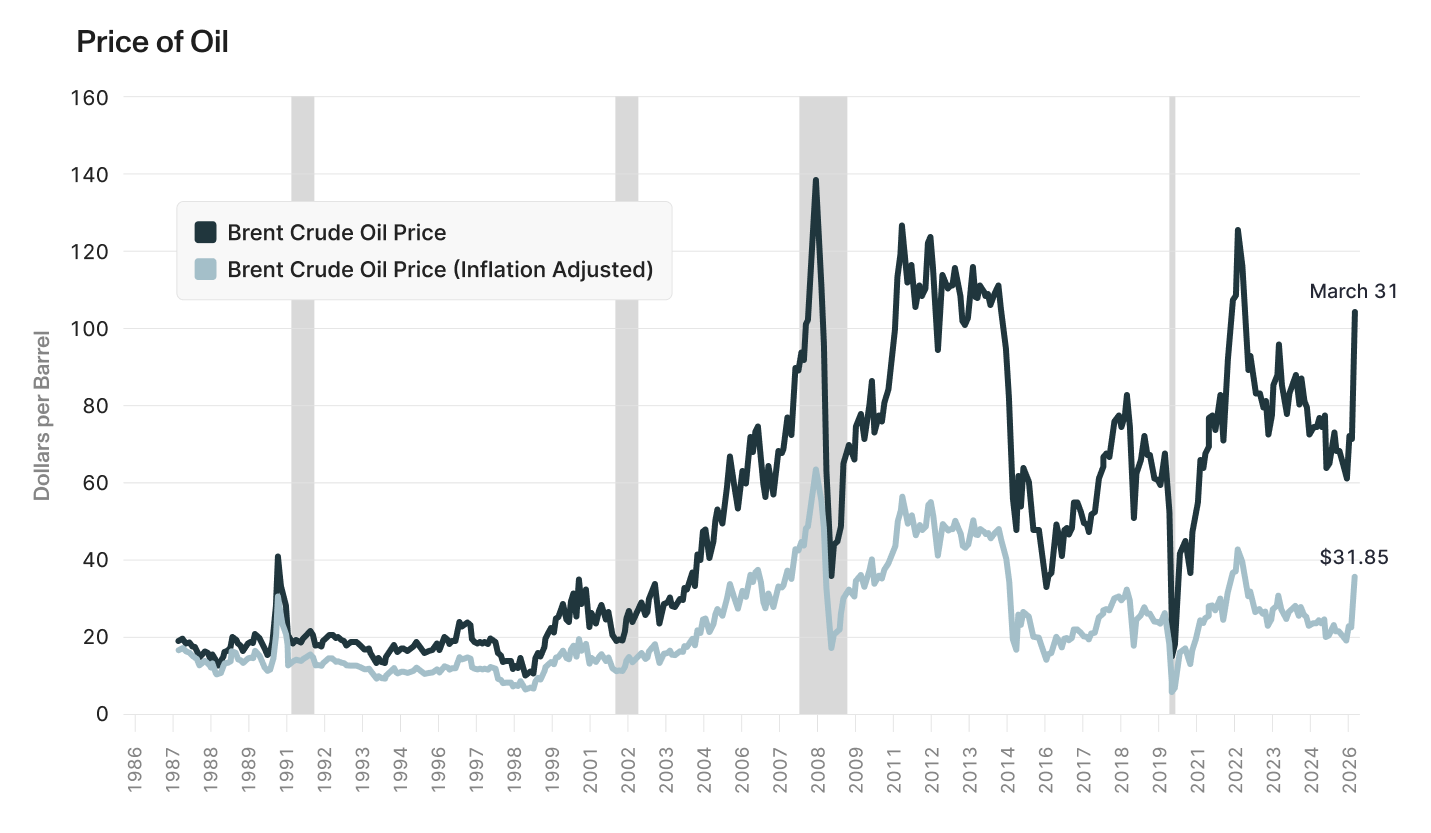

Oil price shocks

The recent escalation in geopolitical tensions has placed oil markets back at the center of the macro narrative. Brent crude prices have surged to over $100 per barrel, a level that historically has been associated with periods of economic stress.14 While oil price spikes are not uncommon, they have tended to coincide with recessions or significant slowdowns when sustained — highlighting the importance of both magnitude and duration. The current move reflects a rapid repricing of geopolitical risk, particularly around supply disruptions tied to the Strait of Hormuz.

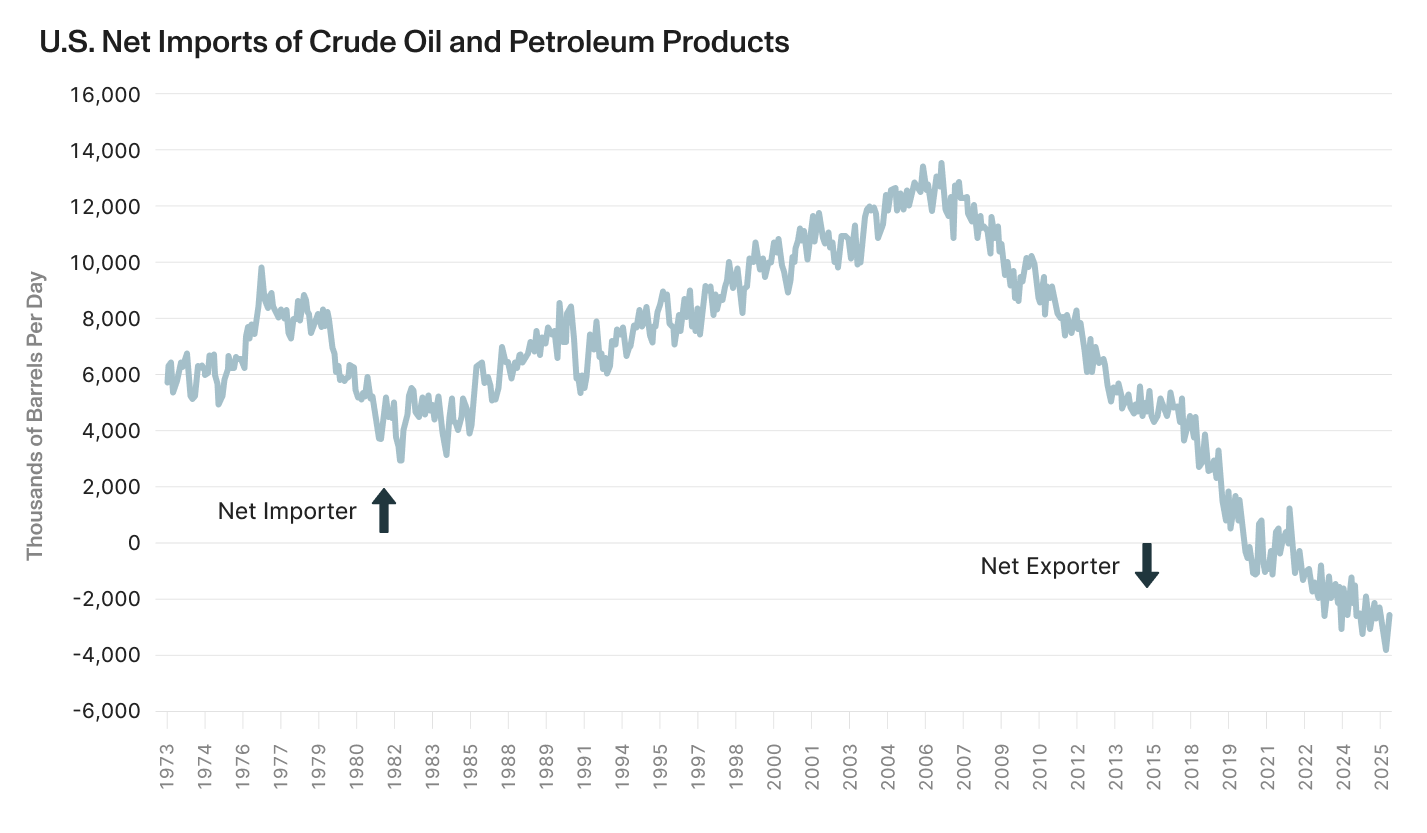

However, the broader economic impact of higher oil prices may be more muted than in past cycles. There has been a structural shift in the U.S. energy position — from a large net importer oil in prior decades to a net exporter today.17 This transition reduces the direct drag of higher oil prices on domestic growth and improves resilience relative to past oil shocks. While higher energy costs still act as a tax on consumers and businesses, the U.S. economy is now better positioned to absorb these shocks than in prior cycles.

Oil Prices — what to watch:

- Duration and magnitude of supply disruptions

- Whether oil remains above ~$100/barrel and feeds into broader inflation

- Spillover into consumer spending and corporate margins

Soft sentiment

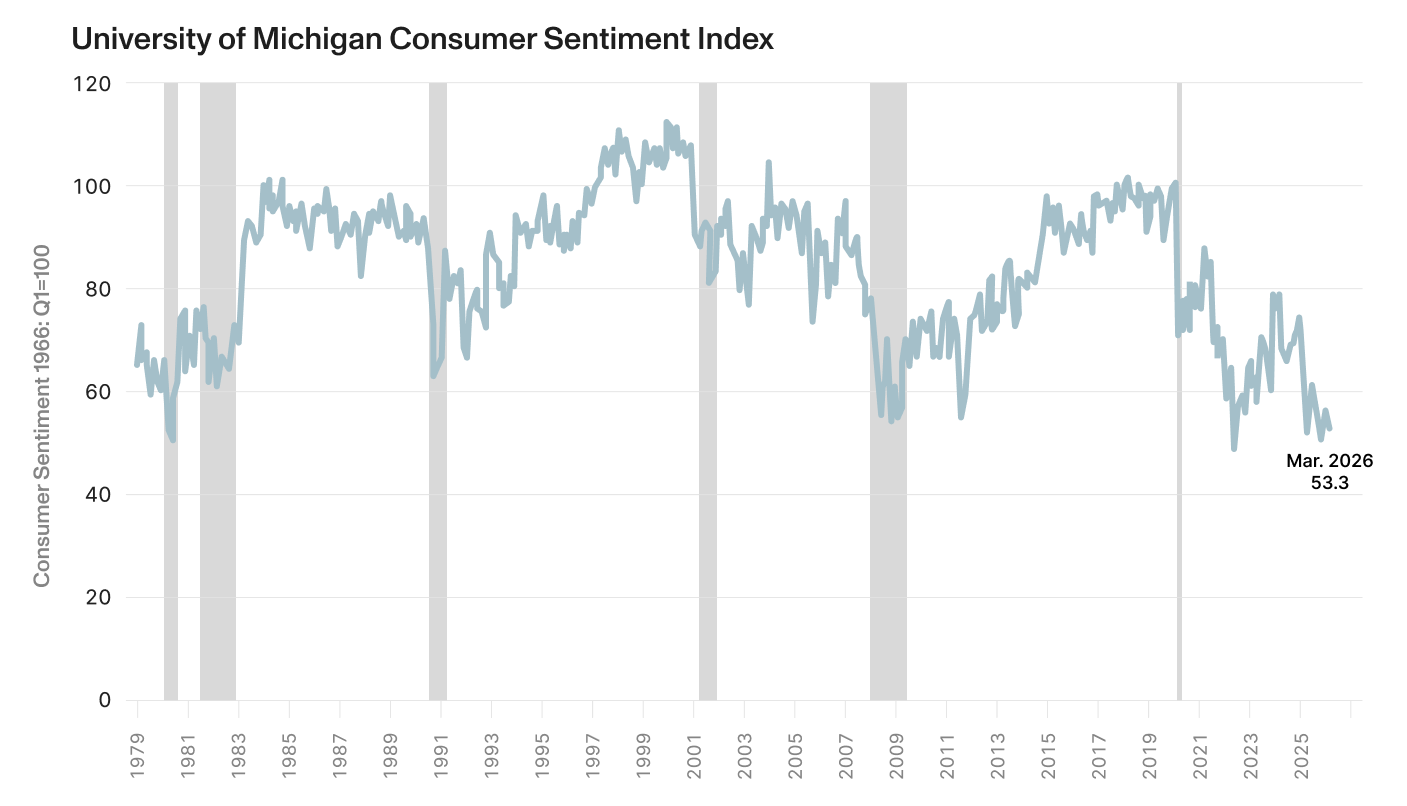

Even as underlying economic activity in the U.S. remains relatively stable, sentiment has deteriorated sharply. The University of Michigan Consumer Sentiment Index has fallen to 53.3 in March 2026, levels historically associated with periods of significant economic stress.19 This decline reflects the combined impact of higher gasoline prices, market volatility, and increased geopolitical uncertainty. Importantly, sentiment has weakened more quickly than hard economic data, suggesting that perceptions of risk are outpacing actual deterioration in activity.

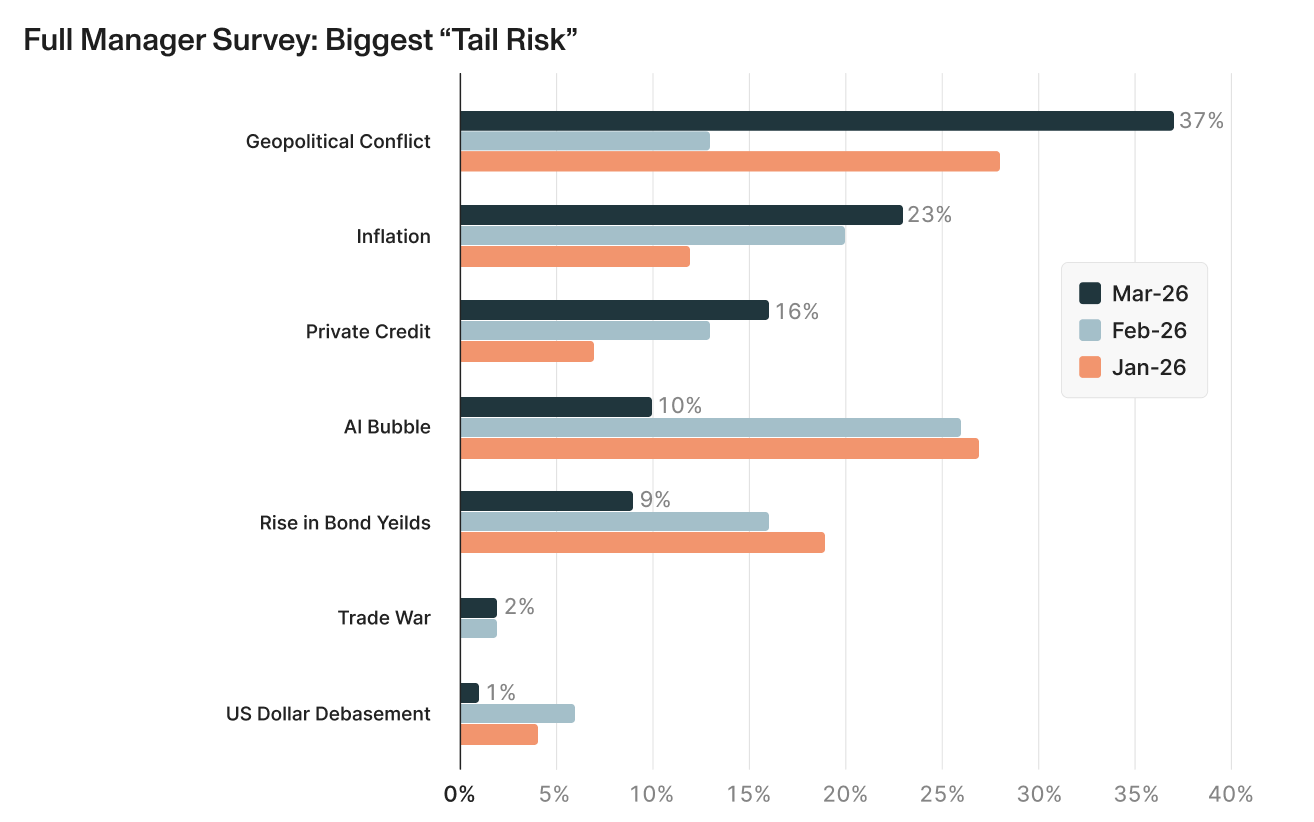

This shift in sentiment is echoed in institutional positioning. The most recent Bank of America global fund manager survey shows geopolitical conflict rising to the top perceived “tail risk,” cited by 37% of respondents — well ahead of inflation (23%) and other concerns.21 Notably, fears of an AI bubble have declined substantially relative to just a month ago, indicating that investor attention has pivoted decisively toward macro and geopolitical risks. Together, these indicators suggest that markets are being driven as much by uncertainty and risk perception as by underlying fundamentals.

Sentiment — what to watch:

- Further decline in consumer confidence levels

- Broadening of risk aversion beyond geopolitics into spending patterns

Increased inflation worries

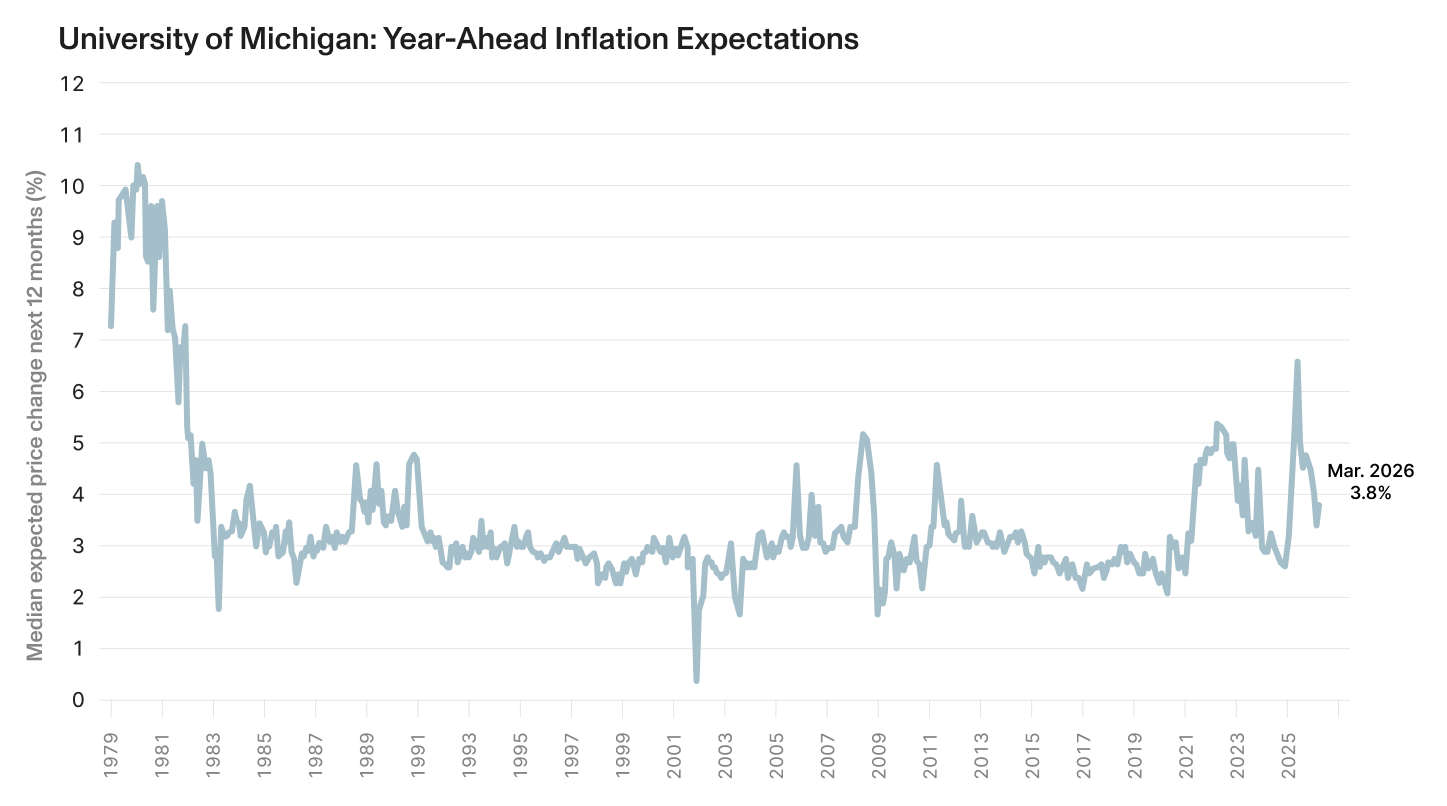

Higher oil prices are already feeding into renewed inflation concerns. The University of Michigan’s survey also shows that year-ahead inflation expectations ticked up to 3.8% in March, reversing some of the progress seen in the disinflationary trend over the past year.23 While still well below the peaks of prior inflationary episodes, the recent increase highlights the sensitivity of inflation expectations to energy prices and underscores the risk that temporary shocks could become more persistent if oil prices remain elevated.

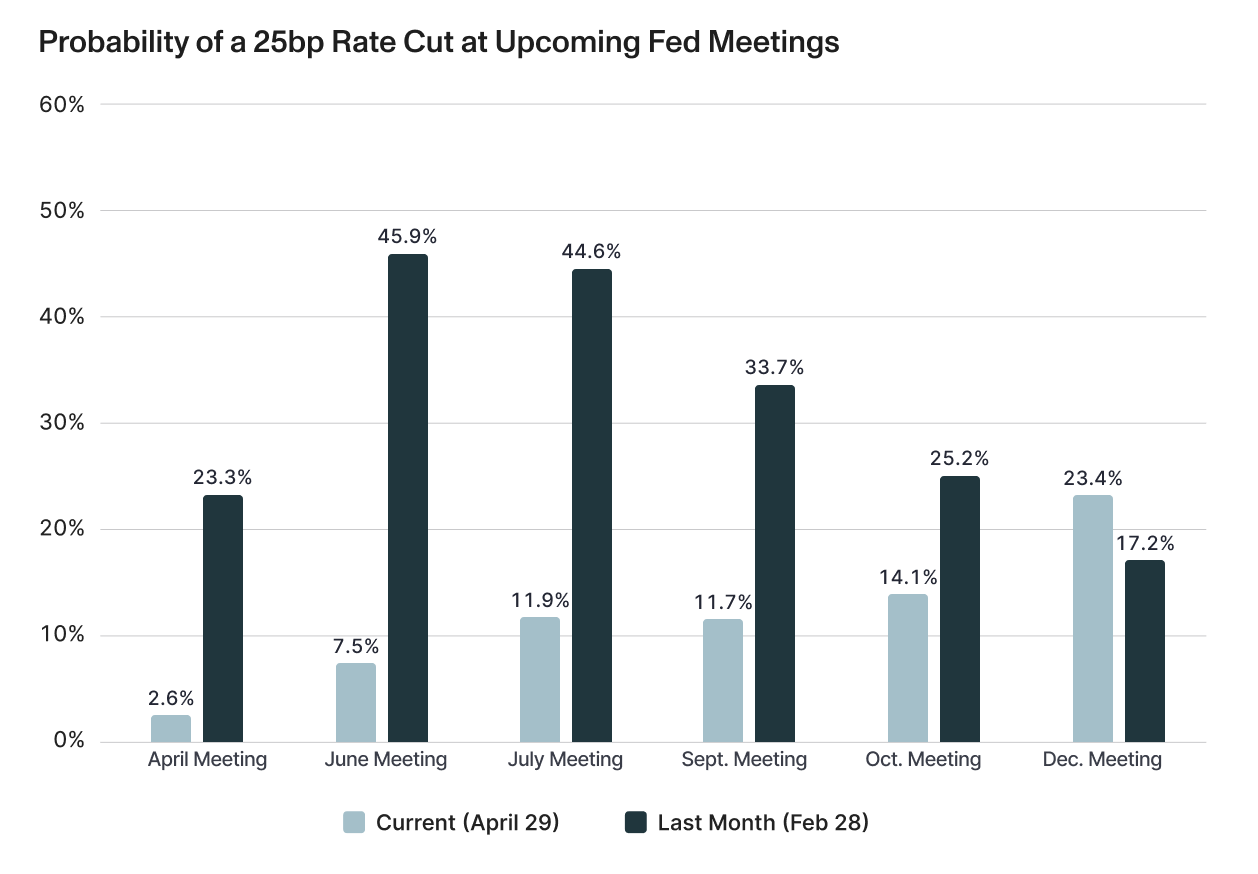

This shift in inflation expectations has had a direct impact on interest rate expectations. Markets have significantly reduced the probability of near-term rate cuts compared to just one month ago. For example, the implied probability of a June rate cut has fallen sharply, while expectations have shifted toward later in the year or fewer total cuts.25 This repricing reinforces a “higher-for-longer” rate environment, tightening financial conditions even in the absence of additional Fed action and contributing to recent market volatility.

Inflation and rate cuts — what to watch:

- Broadening of inflation beyond energy

- Persistence of elevated inflation expectations

- Further higher-for-longer rates expectations

AI fueled fundamentals remain strong

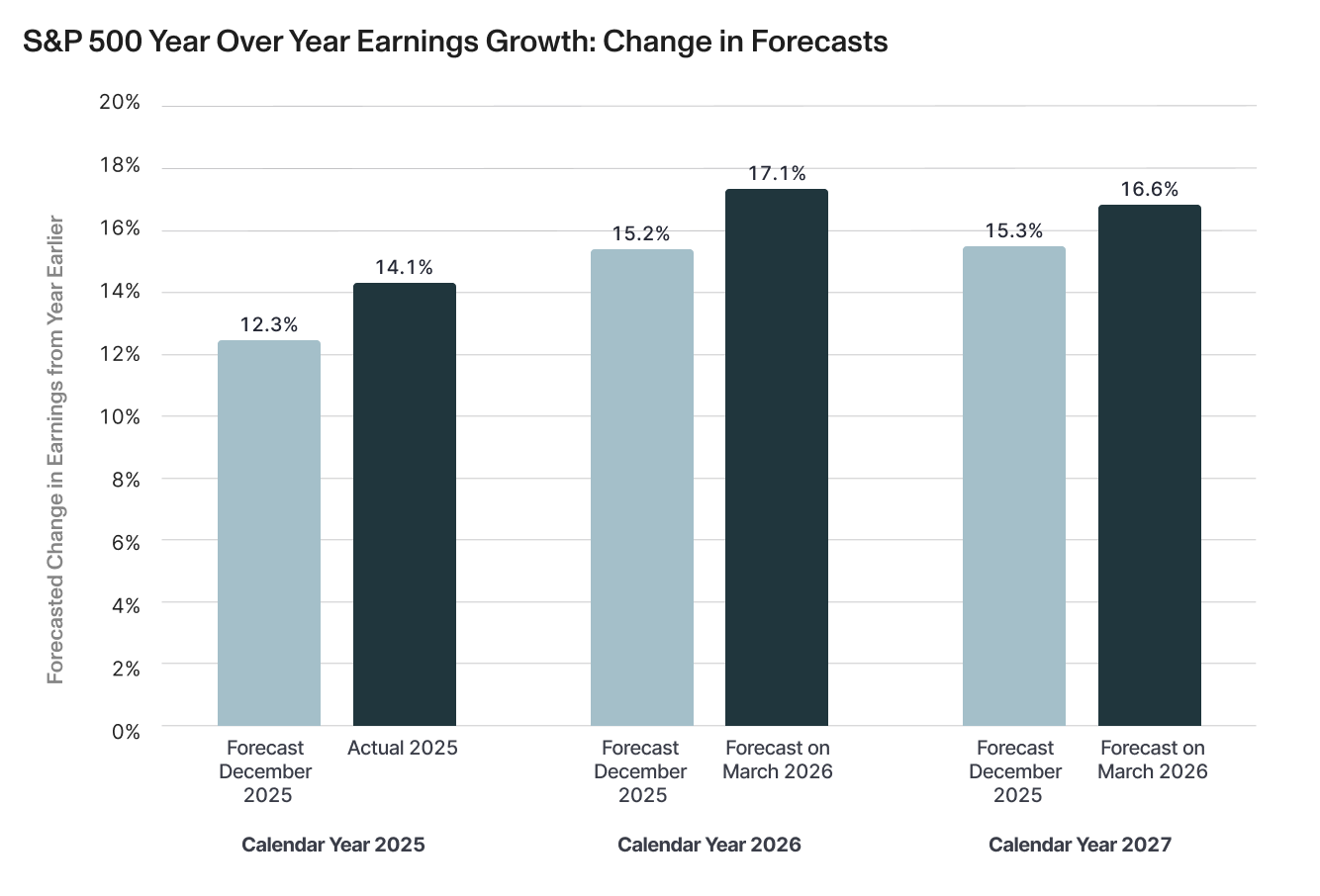

Despite rising geopolitical risks and macro uncertainty, the fundamental backdrop — particularly corporate earnings — remains constructive. S&P 500 earnings growth expectations for 2026 and 2027 have been revised higher since the end of last year, with 2026 earnings now expected to grow over 17% year-over-year, up from prior forecasts.27 This continued upward revision reflects resilient demand, strong margins in key sectors, and ongoing investment in productivity-enhancing technologies.

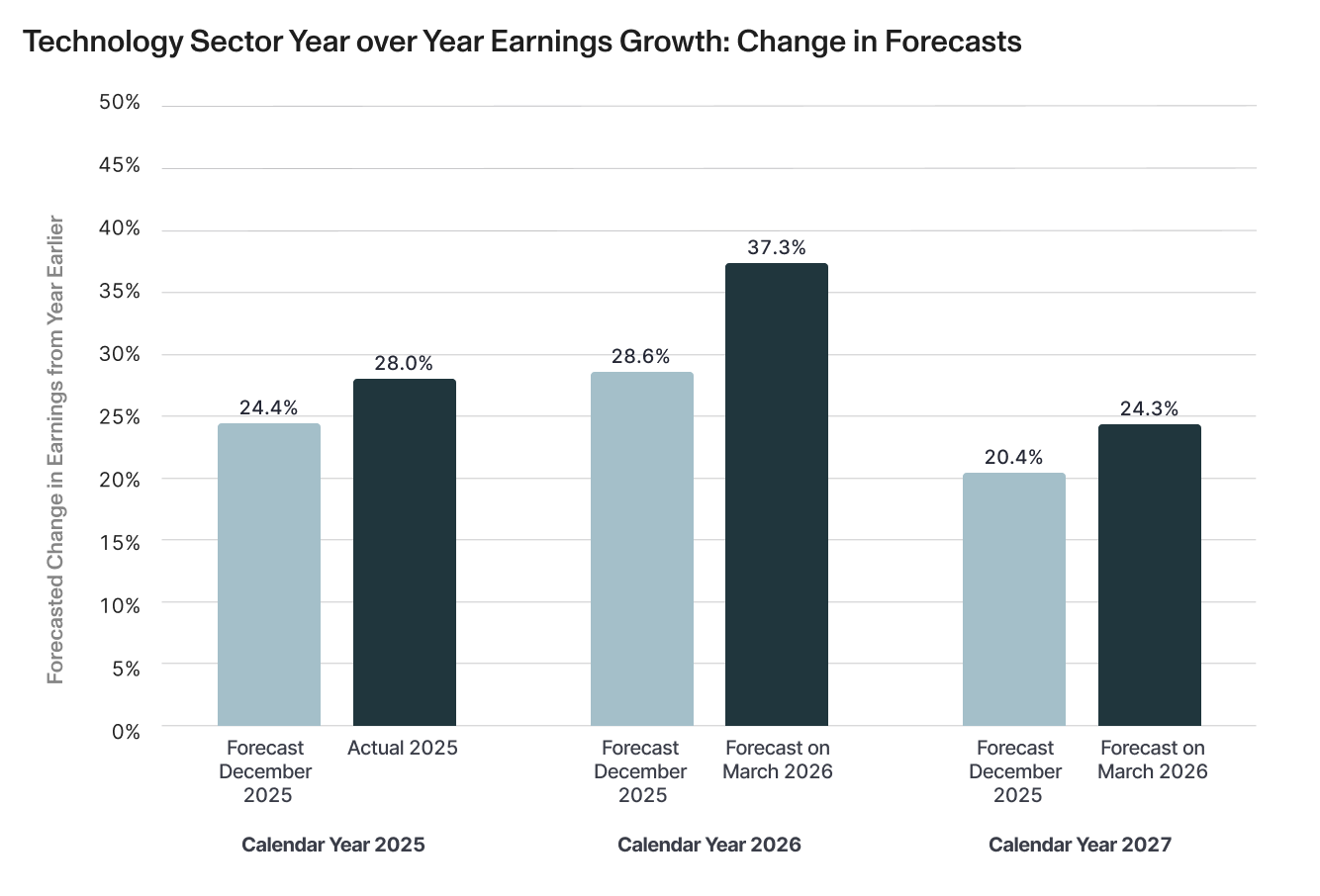

Strength is even more pronounced within the technology sector. Expected earnings growth for technology companies has been revised significantly higher just since the end of last year, with 2026 forecasts rising to over 37%. The increase reflects continued momentum from AI-driven capital expenditures and strong revenue growth across leading platforms. While this concentration of earnings growth raises questions around market breadth, it also highlights the durability of the structural growth drivers underpinning the current cycle.

Earnings trends — what to watch:

- Breadth of earnings growth beyond mega-cap technology

- Sustainability of AI-driven capex and revenue growth

- Early signs of margin pressure from higher input costs and wages

Looking ahead

Taken together, markets are being pulled between weakening sentiment and still-strong fundamentals. While geopolitical risks, higher oil prices, and rising inflation expectations are creating near-term headwinds and driving volatility, they have not yet translated into a meaningful deterioration in earnings or economic activity. Corporate profitability remains solid, forward earnings expectations continue to improve, and structural growth drivers — particularly in technology and AI — remain intact. For investors, the key question is whether sentiment ultimately converges with fundamentals through a slowdown in growth, or whether fundamentals prove resilient enough to support a recovery in confidence. For now, the balance of evidence suggests that while risks have increased, the underlying foundation of the market remains stronger than sentiment implies—reinforcing the importance of maintaining a long-term perspective and staying invested through periods of short-term volatility.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[2] https://www.spglobal.com/spdji/en/index-family/equity/

[3] https://www.bls.gov/news.release/cpi.nr0.htm

[4] https://www.bls.gov/news.release/archives/ppi_02272026.htm

[5] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[6] https://www.bls.gov/news.release/empsit.nr0.htm

[7] https://www.spglobal.com/spdji/en/index-family/equity/

[8] https://www.msci.com/end-of-day-data-search

[9] https://www.nasdaq.com/market-activity/index/comp/historical

[10] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[11] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[12] https://www.theguardian.com/technology/2026/apr/01/spacex-public-offering-stock-market?utm_source=chatgpt.com

[13] https://www.theguardian.com/technology/2026/mar/31/openai-raises-122-billion-ai-boom?utm_source=chatgpt.com

[14] https://www.eia.gov/dnav/pet/pri_spt_s1_d.htm

[15] https://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm

[16] https://www.bls.gov/cpi/

[17] https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MTTTNUS2&f=M

[18] https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MTTTNUS2&f=M

[19] https://www.sca.isr.umich.edu/

[20] https://www.sca.isr.umich.edu/

[21] https://aptuscapitaladvisors.com/the-market-in-pictures-march-27/

[22] https://aptuscapitaladvisors.com/the-market-in-pictures-march-27/

[23] https://www.sca.isr.umich.edu/

[24] https://www.sca.isr.umich.edu/

[25] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[26] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[27] https://insight.factset.com/industry-analysts-project-29-increase-in-sp-500-price-over-the-next-12-months

[28] https://insight.factset.com/industry-analysts-project-29-increase-in-sp-500-price-over-the-next-12-months

[29] https://insight.factset.com/industry-analysts-project-29-increase-in-sp-500-price-over-the-next-12-months