Debt Ceiling Debates, Inflation High but Easing, Employment Strong

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

What's happened recently?

Markets are still digesting a slew of data that suggests the U.S. economy is still experiencing high inflation (albeit at a declining rate), a robust employment backdrop, and is holding up against the Federal Reserve’s rate increases over the past year. Debt ceiling discussions in Washington ramped up and markets are taking notice.

Here are a few things standing out in the news:

- Ongoing debt ceiling debates

- U.S. inflation eases slightly, but remains elevated

- U.S. employment and wages show continued strength

Why is this important?

U.S. economic growth is being sustained by one important driver: consumption. This is a mixed blessing. We are seeing a historically strong employment backdrop providing consumers with strong wage growth and a high ability to spend. However, this makes it harder for the Fed to bring down inflation. We are still feeling the effects of the Fed’s previous tightening on bank lending and the economy, potentially cooling consumption and inflation going forward.

{kind=link}

Another factor impacting markets was Treasury Secretary Janet Yellen's notification to Congress that the U.S. might default on its debt as early as June 1st. This has sharpened both Congress’s focus and the political rhetoric.

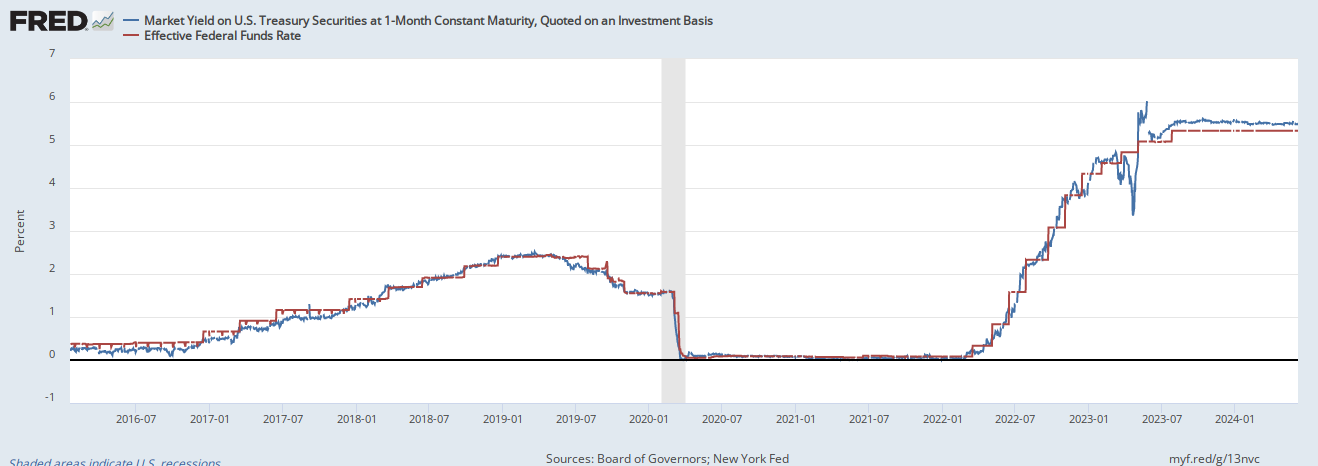

- The debt ceiling debate has led some investors to shun Treasury bills (T-bills) ahead of any potential default. This is evident in the chart above with the one-month T-bill traded at a much lower yield (higher price) than the Fed Funds Rate, indicating investors were willing to pay a premium to be ahead of any default concerns. As Yellen indicated the default might be sooner than expected, we’ve seen a sharp increase in the one-month T-bill yield (trading at a discount) above the Fed Funds Rate and the three-month T-bill, as the one-month’s expiration is now beyond the projected default date.

- U.S. consumer prices rose 4.9% year-over-year through April. Prices remain elevated due to persistently strong shelter costs, though many economists expect this to cool over the coming months as the effects of lower home prices and higher rates generally impact inflation with a lag.

- Employment remains strong, beating expectations. While there are some signs of cooling (and notably in tech and construction), the overall picture remains quite healthy, shrugging off the effects of rising rates. The unemployment rate decreased from last month to historically low levels while wages increased a solid 4.4% over the past year. This backdrop provides the consumer the ability to keep spending, but keeps the economy hotter than the Fed might like.

{kind=link}

{kind=link}

What's our take?

Over the coming weeks, we should continue to see markets react to news around the debt ceiling negotiations.

- We have high certainty that Washington will avoid a default, even if it might be at the 11th hour.

- Defaulting is highly unlikely, but were it to occur, it would have immediate and very large effects on the economy and markets.

- Our view is that the current debt ceiling situation creates an overhang in the short- to intermediate-term, but likely doesn’t create a strong deviation from the long-term trends.

Equity markets have historically been pressured the month before a debt ceiling resolution, but have usually made up for that negative performance after a deal has been made. A medium-term impact could potentially be the balance at the Treasury’s day-to-day expense account account has been drawn down as the U.S. hit the debt-ceiling in January. Rebuilding the Treasury account could provide a headwind to the economy as it drains liquidity from the system. We believe investors should take stock of the near-term risks to markets but also stay focused on the long-term implications, which historically have seen little impact from debt-ceiling debates.

For more information, please check out further disclosures here. Investment advisory services are provided by Compound Advisers, Inc. (“Compound Advisers”), an SEC-registered investment adviser (CRD# 306341/SEC#: 801-122303). Registration as an investment adviser does not imply any level of skill or training. The information contained in this communication is provided by Compound for general informational purposes and should not be considered as financial or tax advice, or an offer to sell securities to you. All investing involves risk, including the possible loss of any or all of the money invested, and past performance never guarantees future results. Please see Compound Advisers' Form CRS here , and ADV Part 2A Brochure here.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).