U.S. Govt Debt Downgraded, Inflation Moderates, Earnings Beat Expectations

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

What's happened recently?

Markets have been turbulent over the past two weeks. The S&P 500 is down 2.4% over this period – the weakest two-week market performance since the banking stress (March) and debt ceiling debates (May). While the magnitude isn’t severe, this period of volatility follows a relatively calm couple of months and marks the highest count of down days in a two-week span this year.

Here are a few things standing out in the news:

- U.S. government debt downgraded

- Inflation below expectations, still relatively high

- Earnings growth beat expectations, revenue growth underwhelming

- Job growth steady but slower than expected

Why is this important?

The past two weeks have confirmed a recent trend that the U.S. economy has weathered the Fed’s increase in rates and companies have been able to limit the effects of a more difficult earnings environment.

- On August 1st, Fitch downgraded the debt of the U.S. government debt to one notch below its highest quality, catching many investors off-guard and creating additional volatility in the market. The rating agency mentioned that the downgrade was based on the "anticipated fiscal deterioration over the next three years" and the existence of "a high and growing general government debt burden." Fitch also acknowledged an "erosion of governance" spanning the previous two decades, a trend manifested through recurrent episodes of debt limit stand-offs and eleventh-hour resolutions.

- Consumer prices rose 3.2% over the last year coming in below expectations, providing some relief to investors. After reaching a peak of 9.1% last summer, headline inflation figures have been gradually approaching the Federal Reserve's 2% target. Yet, core inflation (excluding food and energy) has moderated at a much slower rate, compelling the central bank to maintain higher interest rates for an extended period. The Fed is closely monitoring consistent wage growth, which is supporting consumer spending.

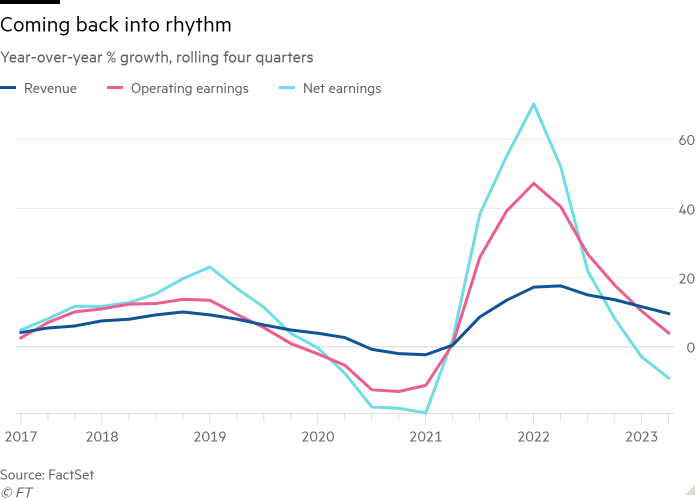

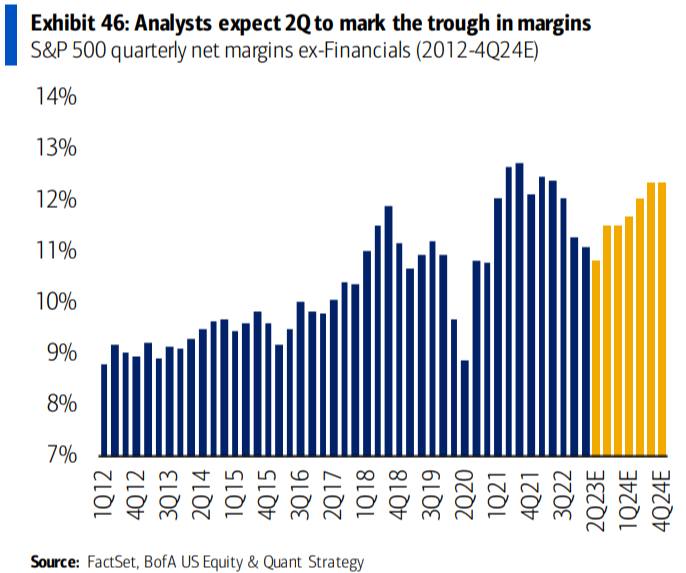

- As earnings season wraps up, the headline numbers may look a little soft. However, the underlying details show a resilient economy supporting decent corporate performance. Things aren’t quite as good as they were a year ago, but they are holding up well. Second quarter S&P 500 earnings fell a little over 5% from last year. Importantly, the declines are concentrated in just a few sectors (see chart below). This quarter’s numbers seem to indicate more of a normalization from the extraordinary conditions post-pandemic. Of greater concern is the low revenue growth, which makes an increase in earnings harder, especially as margins compressed. Analysts expect margins to widen going forward, which could lead to volatility if the lofty expectations are not met.

{kind=link}

{kind=link}

What's our take?

We believe the economy is still in a fragile state and the effects of rising rates remain uncertain. Economic data has been strong, leading to a sustained rise in markets even after the past couple of weeks of volatility. Expectations for a “soft landing” have been steadily increasing, along with valuations on riskier assets. However, we remain cautious, recognizing that heightened expectations could become harder to fulfill.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).