Fundamentals in Focus

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

Markets entered 2026 with a familiar mix of optimism and unease. The S&P 500 reached new highs early in January before modest pullbacks tied to earnings volatility and renewed questions around valuations, growth durability, and policy uncertainty.1 Importantly, recent gains have been driven increasingly by earnings growth rather than multiple expansion, suggesting a more fundamentally grounded advance than in earlier phases of the cycle.2 While consumer confidence is subdued and geopolitical headlines remain persistent, returns may continue to be strong, but with a less smooth path than in recent years.

Beneath the surface, economic momentum continues to outweigh evolving risks. Growth is accelerating, earnings remain resilient, and inflation is moderating, providing a supportive backdrop for risk assets. Market leadership has broadened meaningfully, with smaller companies, cyclicals, and value stocks outperforming, an environment more consistent with expansion than contraction. In addition, productivity gains and rising capital investment have allowed output and profits to rise even as job growth slows, reinforcing the view that recession risks are currently perceived as low. While current tailwinds may moderate later in the year, the overall foundation entering 2026 remains strong.

January 2026 at a glance

- Growth momentum stayed firm in January. Economic data continued to point to expansion, with real activity holding up despite slower job growth — reinforcing the view that productivity, not weakening demand, is driving this cycle.3 4

- Earnings expectations remained healthy. Analysts continue to forecast low-to-mid-teens earnings growth for 2026, and early Q4 reporting kept the S&P 500 on track for its 10th consecutive quarter of year-over-year earnings growth.5

- Leadership broadened meaningfully. Smaller and more cyclical areas outperformed during the month, with the Russell 2000 up mid-single digits, alongside strength in value stocks, cyclicals, and select international markets.6 7 8

- Inflation continued to cool. Core measures eased further in January, while longer-term expectations remained anchored near the Fed’s target.9

- The Federal Reserve paused rate cuts. After 75 basis points of rate cuts last year, the Fed held rates steady in January, signaling patience and a data-dependent path rather than imminent further easing. The announcement of the new Fed Chair may change expectations around that path.10

- Commodities reasserted themselves — with more volatility. Gold and silver prices rose in January until a sharp sell off on the last day of the month. Gains in the past year have been supported by strong central-bank demand, persistent fiscal concerns, and diversification flows, while increased ETF and investor participation contributed to larger price swings.

- Market stress indicators remained calm. Despite elevated headlines, equity volatility stayed low and credit spreads remained tight, signaling confidence in continued economic expansion rather than rising systemic risk.

- Geopolitical risks resurfaced but remained contained. Trade rhetoric and global tensions involving Iran, Venezuela, and NATO drew attention in January, yet markets largely viewed these as potential rather than immediate economic threats.

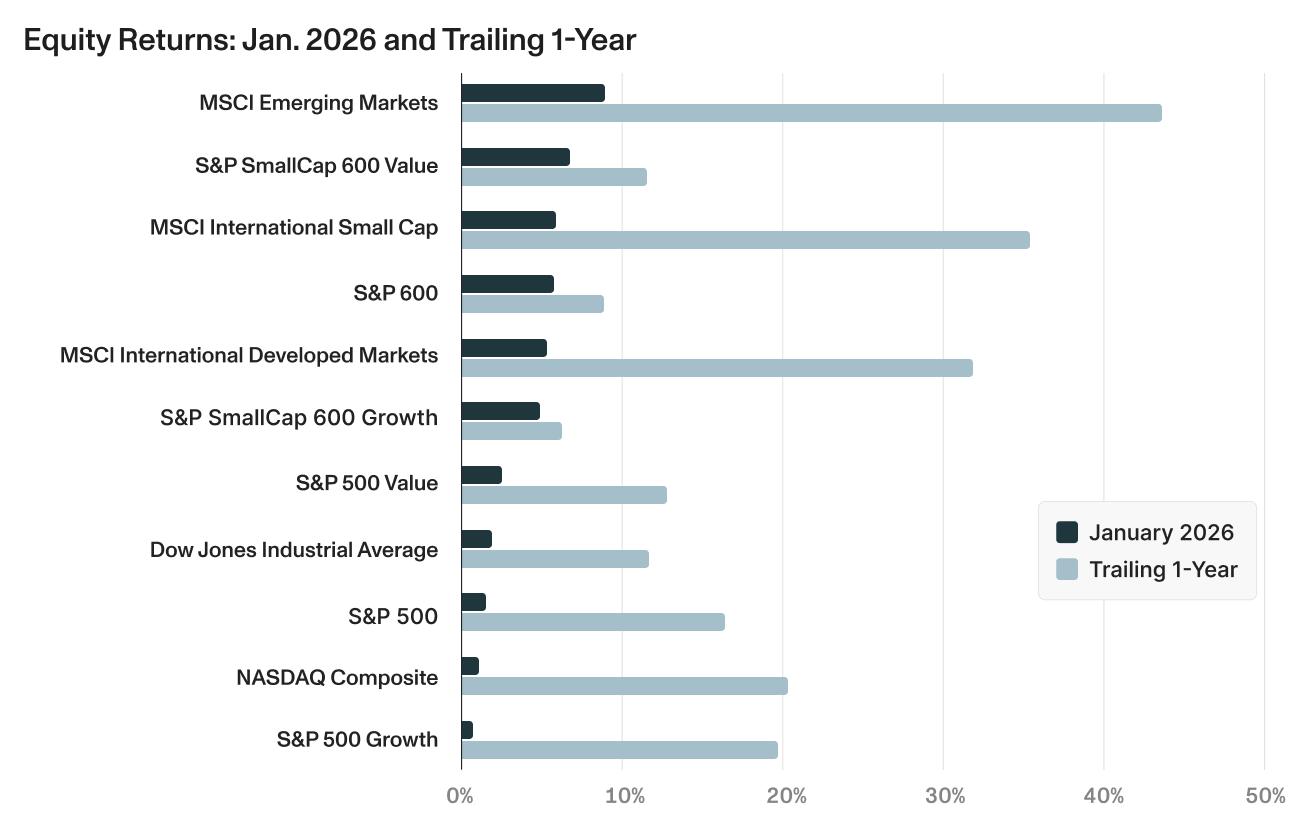

Stocks Start Strong

Equity markets advanced in January, supported by resilient earnings expectations, moderating inflation, and continued economic momentum.11 12 13 While major indices experienced modest volatility after reaching early-month highs, leadership broadened, with smaller companies, cyclicals, and value-oriented sectors outperforming. This pattern reflects a market increasingly driven by fundamentals rather than valuation expansion, as investors looked beyond short-term uncertainty toward earnings growth and a lower probability of recession heading into 2026.

- Leadership tilted toward smaller and international markets. Emerging markets led in January, while international developed and international small caps rose solidly, extending strong trailing one-year gains.

- Small-cap value outpaced large-cap growth. U.S. small caps gained over 5% in January, led by Small Cap Value, showing the rotation toward more economically sensitive areas.

- Mega-cap growth lagged despite solid longer-term returns. The S&P 500 rose modestly in January, while growth-heavy indices like the NASDAQ trailed, even as their trailing 1-year returns remain strong.

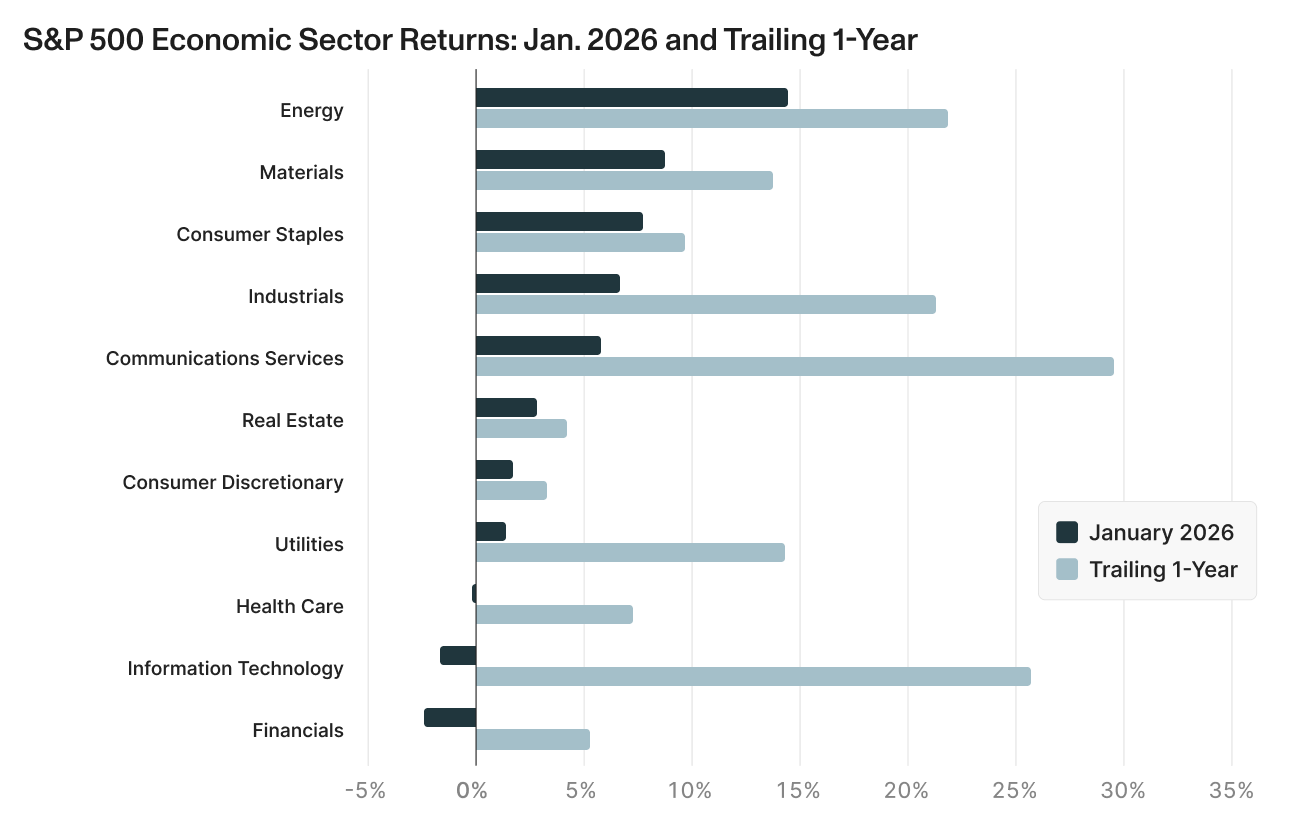

- S&P Sector returns:

- Cyclical sectors led. Energy and Materials outperformed, extending solid one-year gains as markets priced in stronger growth.

- Breadth extended beyond growth. Industrials and Consumer Staples posted strong returns, with Industrials up over 20% over the past year.

- Growth leadership paused. Information Technology and Financials lagged on questions about tech earnings sustainability and expectations for fewer rate cuts in 2026.

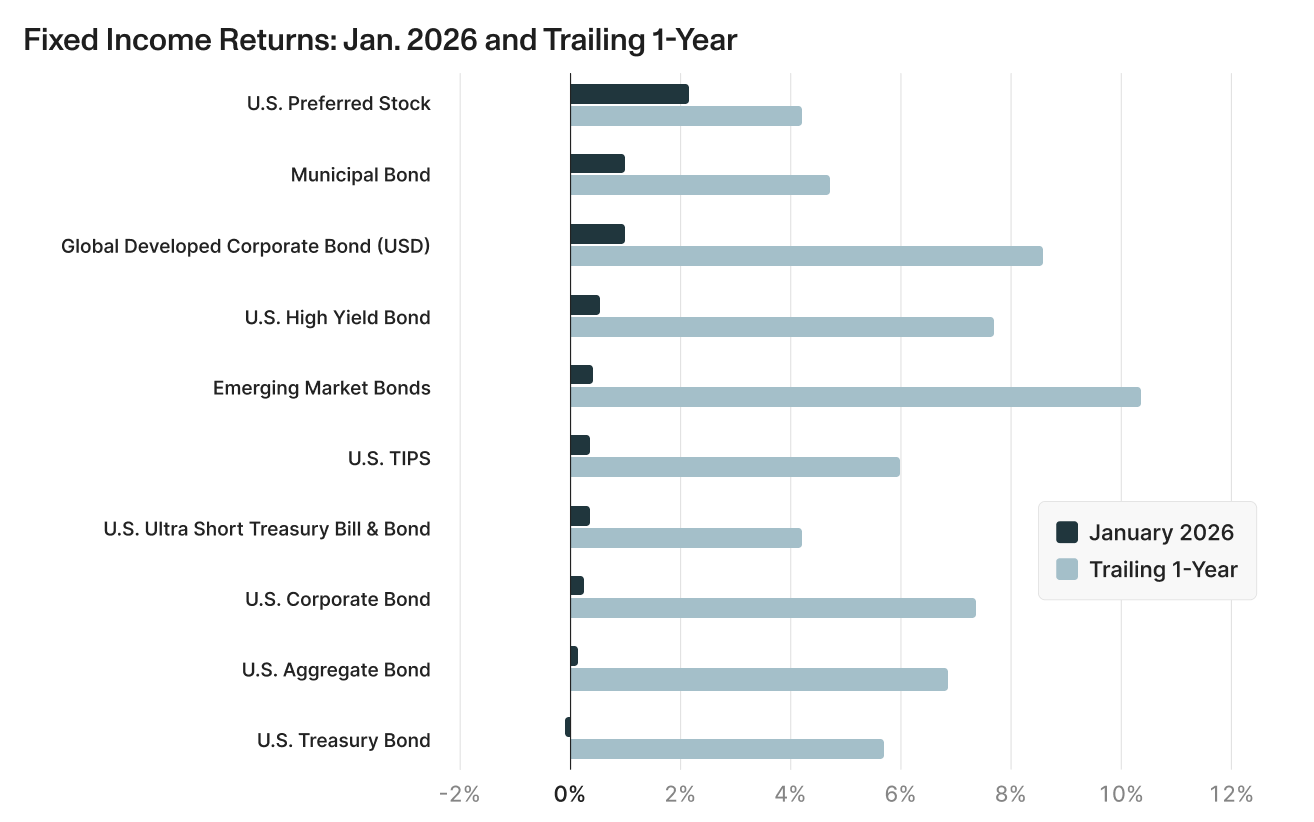

Steepening Yield Curve Supports Bonds

Credit markets continue to signal confidence in the economic outlook. Spreads remain tight, default expectations are low, and bond market volatility has been far more contained than equity volatility.

The yield curve has fully un-inverted, potentially marking a transition into a new phase of the cycle.18 While fiscal concerns persist, bond markets appear more focused on growth and inflation dynamics rather than potential stresses.

- Income sectors led. Preferred stocks and municipal bonds outperformed in January, extending solid trailing one-year gains.

- Credit remained steady. High yield and corporate bonds posted modest gains for the month, bolstering strong one-year returns.

- Treasuries were flat to slightly negative. U.S. Treasuries slipped in January, though trailing one-year returns remain solid, reflecting range-bound rates.

Private Markets: Adjusting but Solid

Repricing across private assets continues, but at a gradual pace that reflects stable economic growth, healthy credit conditions, and improving financing availability rather than forced deleveraging.20 Exit activity remains muted, with a growing share of transactions occurring sponsor-to-sponsor as strategic buyers remain selective. Underlying fundamentals like cash-flow durability, productivity gains, and access to capital, remain supportive. Improving financial conditions and a steeper yield curve should gradually improve transaction activity in 2026, even if valuations normalize rather than re-inflate.

- Private Credit: Credit appetite remains healthy, supported by tight spreads, improving liquidity, and demand for income-oriented capital.

- Private Real Estate: A steepening yield curve is beginning to relieve pressure on rate-sensitive sectors, though recovery is likely to be uneven and favor income-producing assets.

- Private Equity & Venture Capital: Exit activity remains constrained, with sponsor-to-sponsor transactions filling the gap as venture markets shift toward monetization and earnings discipline.

Looking forward: Emerging Themes for 2026

Equity Market Broadening and Rotation

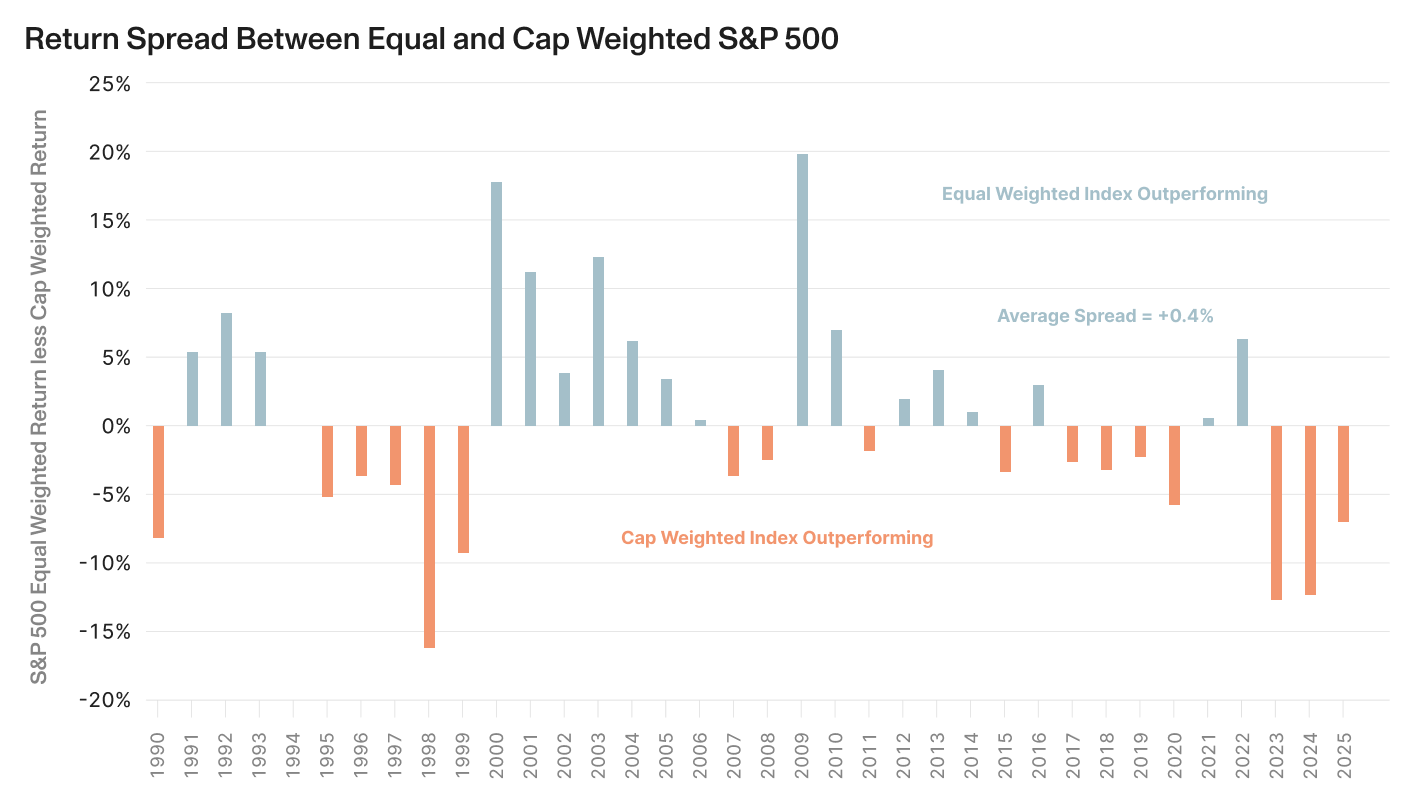

One of the most important developments early in 2026 has been the broadening of equity market leadership. After several years of extreme concentration, performance has begun to rotate away from a narrow group of mega-cap technology stocks toward smaller companies, cyclicals, value stocks, and select international markets. This environment is more consistent with economic expansion than late-cycle stress.

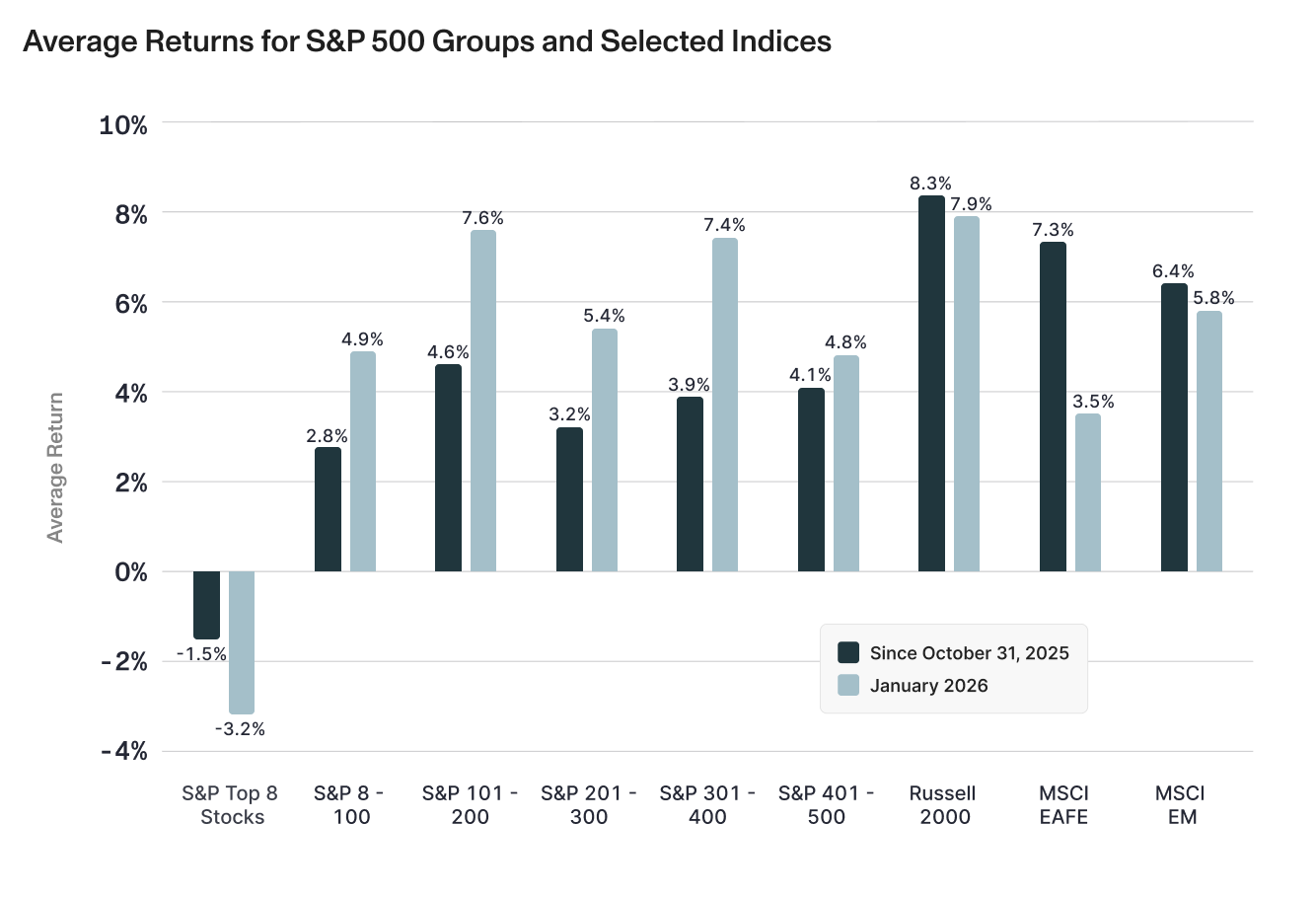

The charts below illustrate how the mega caps have dominated returns for the past three years and the notable rotation in leadership since last fall. The first chart shows that the cap weighted S&P 500, led by the mega cap growth stocks, has substantially outperformed the equal weighted index where mid and small cap stocks have a greater influence. The second chart shows how the segments of the equity market have far outpaced the largest S&P 500 stocks since October.

This rotation reflects widening valuation dispersion, improving earnings visibility outside technology, and a steeper yield curve that supports banks, housing, and other capital-intensive sectors. While headline indices remain influenced by mega-caps, equal-weight and cyclical areas have shown increasing relative strength.

Technology and AI remain critical long-term drivers, but durable bull markets typically require broader participation. Consensus expectations for low-to-mid-teens earnings growth reinforce the view that returns are increasingly driven by fundamentals rather than valuation expansion. Elevated valuations remain a consideration, but strong earnings and economic stability have historically supported returns even in expensive markets.

Market leadership — What to look out for:

- Earnings delivery beyond mega-caps

- Sustained strength in small caps and cyclicals

- Rotation without broad market stress

Inflation, the Fed, and Policy Uncertainty

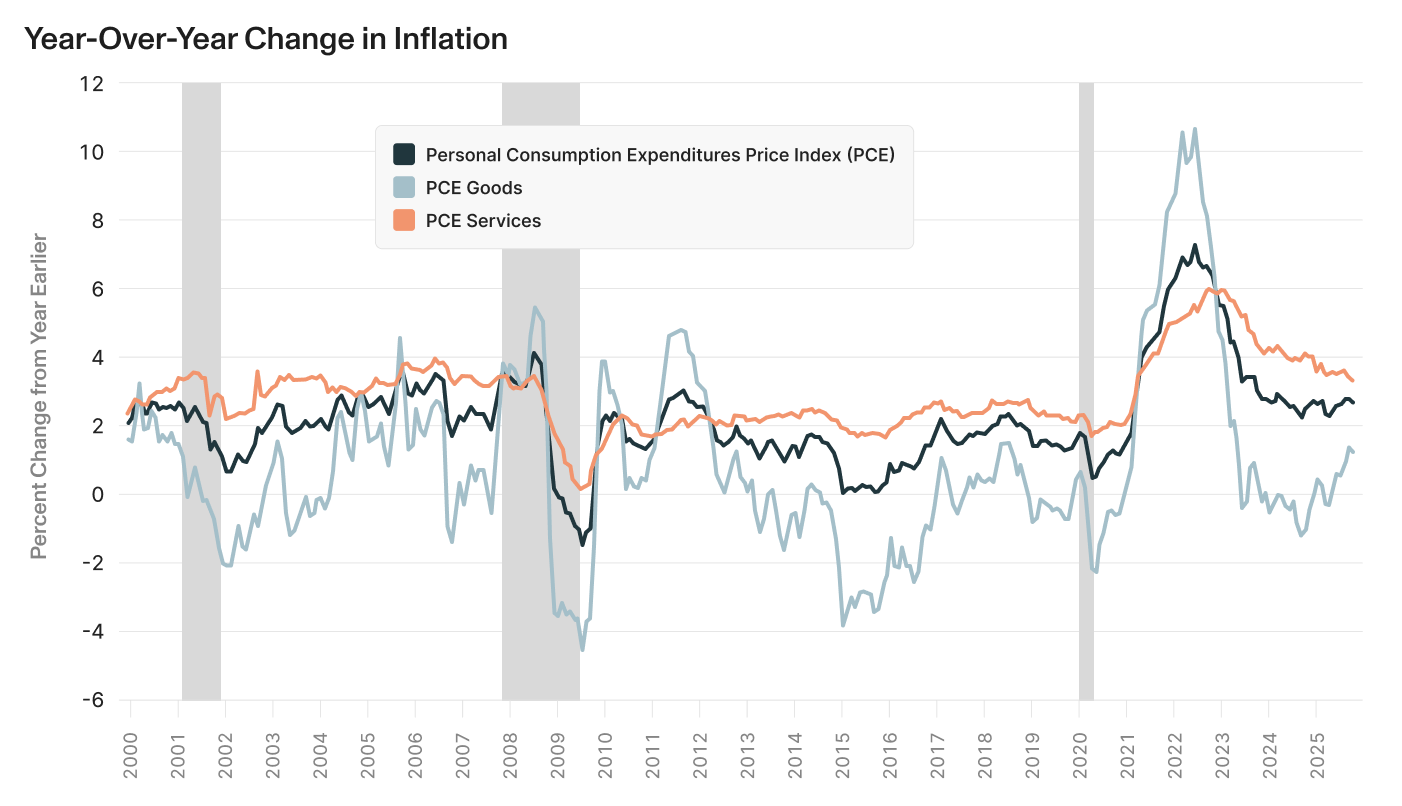

Inflation continues to move in the right direction, though the Federal Reserve remains cautious about declaring the job complete. At his January 28 press conference, Chair Jerome Powell emphasized that while inflation has fallen substantially from its 2022 peak, it remains somewhat above the Fed’s 2% target.25

A key distinction highlighted by the Fed is where inflation pressures are coming from. As the chart shows, recent inflation has been concentrated in goods prices, largely reflecting delayed tariff effects rather than excess demand. In contrast, services inflation has continued to ease. The Fed views tariff-related price increases as a one-time adjustment to the price level, not the start of a renewed inflation cycle. Consistent with this view, both market-based and survey measures of inflation expectations have improved, and longer-term expectations remain well anchored.26

After cutting rates by 75 basis points in 2025, the Fed held rates steady in January. Policy now sits in the range of neutral, neither expansionary or contractionary. Powell pushed back against expectations for near-term rate cuts, noting that with growth firm, unemployment stabilizing, and inflation still above target, additional easing will require clearer evidence of further disinflation or renewed labor market weakness.28

While markets briefly reacted to the announcement of Kevin Warsh as the next Fed Chair, the move appears to be increasingly assessed as a repositioning rather than a major shift in the monetary policy outlook. Warsh is widely viewed as experienced, market-savvy, and institutionally credible, and while his leadership style and regulatory emphasis may differ from Powell’s, the Fed’s mandate and policy framework are not likely to change substantially.29

From an investor perspective, this marks a transition in monetary policy’s role in recent years. The Fed is shifting from being a tailwind to markets to a more neutral stance. This has allowed economic and corporate fundamentals to take a larger role. Strong productivity growth has raised potential output, reducing the likelihood that above-trend growth alone forces tighter monetary policy, placing greater emphasis on earnings, productivity, and fundamentals as the primary drivers of market returns.

Fed Policy — What to look out for:

- Services and shelter inflation trends

- Fading tariff-related goods inflation

- Labor market data influencing path of future rate cuts

Earnings are the Engine of This Cycle

Earnings growth has become the primary driver of market returns as multiple expansion has largely stalled. The S&P 500 has now delivered positive year-over-year earnings growth for ten consecutive quarters, reinforcing the fundamentally driven nature of the rally.30

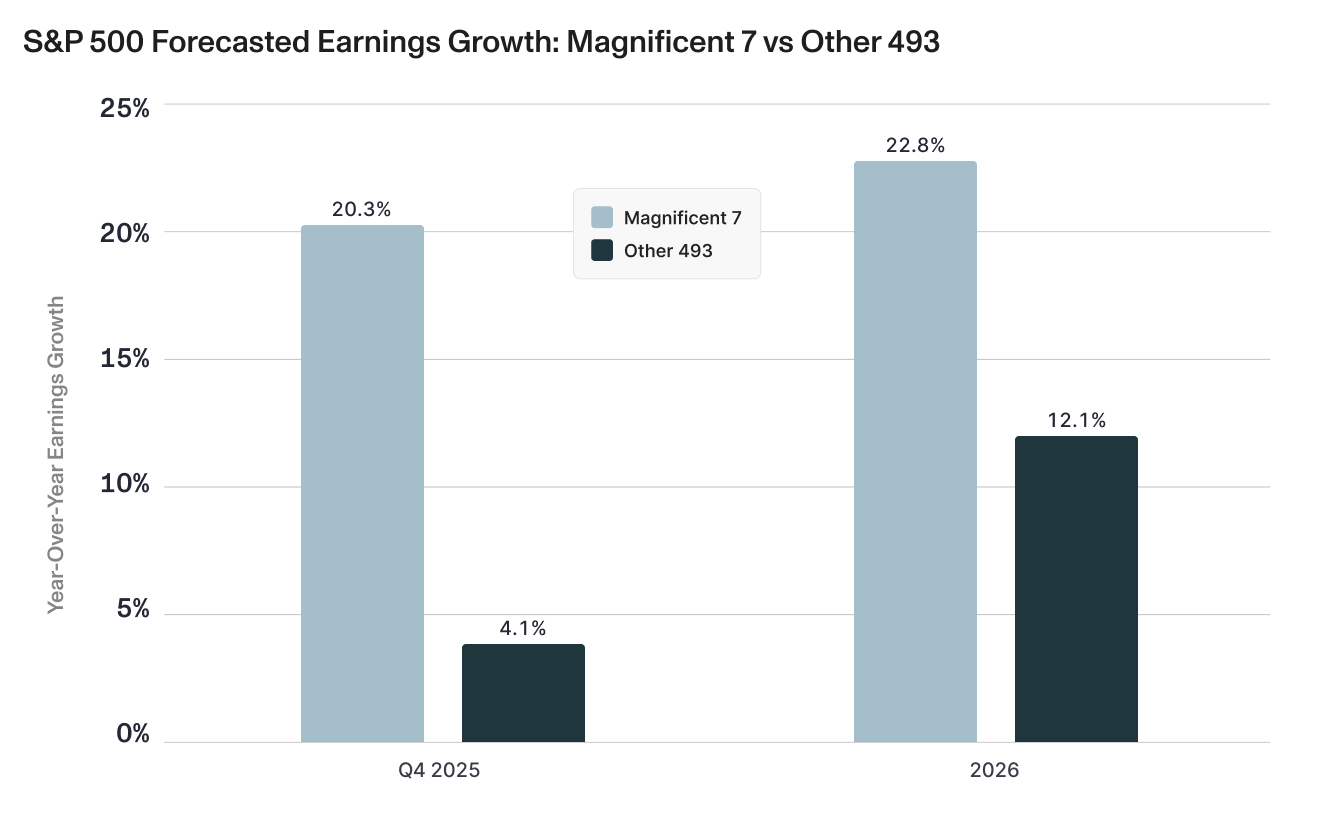

Consensus earnings expectations remain constructive. Estimates for late 2025 appear conservative relative to recent history, and early reporting suggests continued resilience. While technology remains the largest contributor to earnings growth, financials, industrials, and materials are playing an increasingly important role as economic momentum broadens. The chart shows that while the “Mag 7” are expected to continue to deliver over 20% year-over-year earnings growth, growth from the “other” companies in the S&P is forecast to almost triple in 2026.

The continued strong profit growth is being fueled by productivity gains, automation, and capital deployment. Looking ahead, consensus forecasts call for mid-teens earnings growth in 2026.32 While ambitious relative to nominal GDP, this outlook is plausible if productivity gains persist and margins remain resilient. The evolving AI investment cycle remains central to this view. With capital spending potentially slowing from extreme peaks as the base expands, the focus of investors should shift from early enthusiasm to monetization. While this transition may introduce volatility, the cycle remains closely tied to real earnings and investment rather than speculation.

Earnings trends — What to look out for:

- Earnings growth beyond mega-cap technology

- Margin resilience

- AI monetization keeping pace with expectations

Navigating the Path Forward

As we move deeper into 2026, markets are being shaped more by economic momentum and earnings growth than by hypothetical risks. Growth remains resilient, inflation continues to moderate, and monetary policy has shifted from a powerful tailwind to a steady backdrop. Equity leadership is broadening, returns are increasingly fundamentals-driven, and volatility reflects rotation rather than systemic stress. While uncertainties remain, history suggests that without economic or earnings deterioration, such risks tend to create noise rather than lasting damage.

For investors this means staying diversified, emphasizing earnings quality, and remaining disciplined through normal volatility is likely to matter more than reacting to short-term headlines.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.spglobal.com/spdji/en/index-family/equity/

[2] https://insight.factset.com/sp-500-earnings-season-update-january-30-2026

[3] https://www.bea.gov/data/gdp/gross-domestic-product

[4] https://www.bls.gov/news.release/empsit.nr0.htm

[5] https://insight.factset.com/sp-500-earnings-season-update-january-30-2026

[6] https://www.spglobal.com/spdji/en/index-family/equity/

[7] https://indexcalculator.ftserussell.com/

[8] https://www.msci.com/end-of-day-data-search

[9] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[10] https://www.federalreserve.gov/newsevents/pressreleases/monetary20260128a.htm

[11] https://www.spglobal.com/spdji/en/index-family/equity/

[12] https://insight.factset.com/sp-500-earnings-season-update-january-30-2026

[13] https://www.bea.gov/data/gdp/gross-domestic-product

[14] https://www.spglobal.com/spdji/en/index-family/equity/

[15] https://www.msci.com/end-of-day-data-search

[16] https://www.nasdaq.com/market-activity/index/comp/historical

[17] https://www.spglobal.com/spdji/en/index-family/equity/

[18] https://www.federalreserve.gov/releases/h15/

[19] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[20] SK Research and Due Diligence, LLC, January 30, 2026

[21] https://aptuscapitaladvisors.com/the-market-in-pictures-january-23/

[22] https://aptuscapitaladvisors.com/the-market-in-pictures-january-23/

[23] https://indexcalculator.ftserussell.com/

[24] https://www-cdn.msci.com/web/msci/index-tools/end-of-day-index-data-search

[25] https://www.federalreserve.gov/newsevents.htm

[26] https://www.sca.isr.umich.edu/

[27] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[28] https://www.federalreserve.gov/newsevents.htm

[29] https://www.cfr.org/articles/why-kevin-warsh-wont-revolutionize-the-federal-reserve

[30] https://insight.factset.com/sp-500-earnings-season-update-january-30-2026

[31] https://insight.factset.com/are-magnificent-7-companies-still-top-contributors-to-earnings-growth-for-the-sp-500-for-q4

[32] https://insight.factset.com/sp-500-earnings-season-update-january-30-2026