Rewards and Risks

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

Investing is always about balancing potential rewards against real risks. Today’s backdrop remains supportive for investors, with earnings growth broadening, industrial activity improving, and AI-driven productivity gains which, in our view, have begun to bolster corporate profits in specific sectors. At the same time, February brought meaningful developments in trade policy, geopolitical tensions, and private credit that warrant careful attention. Markets can advance amid uncertainty, but concentration and complacency carry their own risks. While diversification does not ensure a profit or protect against loss, we believe a balanced approach is appropriate in periods of heightened uncertainty.

February 2026 at a glance

- Economic Growth: Fourth-quarter GDP growth slowed to 1.4%, weighed down by the government shutdown, though consumption remained firm.1 More recent indicators suggest growth continues near the current pace, with industrial activity notably improving.2

- Earnings: S&P 500 companies delivered approximately 9% revenue growth in Q4 — the strongest pace in three years — with earnings growth broadening beyond mega-cap technology.3

- Equity market leadership: Market participation has rotated meaningfully. Older economy utilities, energy and materials companies led in February, while previously dominant technology stocks fell amidst heightened volatility.4

- Inflation and Employment: CPI came in slightly below expectations, though core services inflation remains sticky and PPI and PCE were firmer.5 6 7 Employment growth continues at a slower but steady pace.8

- The Federal Reserve: With inflation hovering near 3% and unemployment near historically low levels, the Fed remains cautious. Policy is modestly restrictive, and further easing will likely depend on clearer labor market softening.

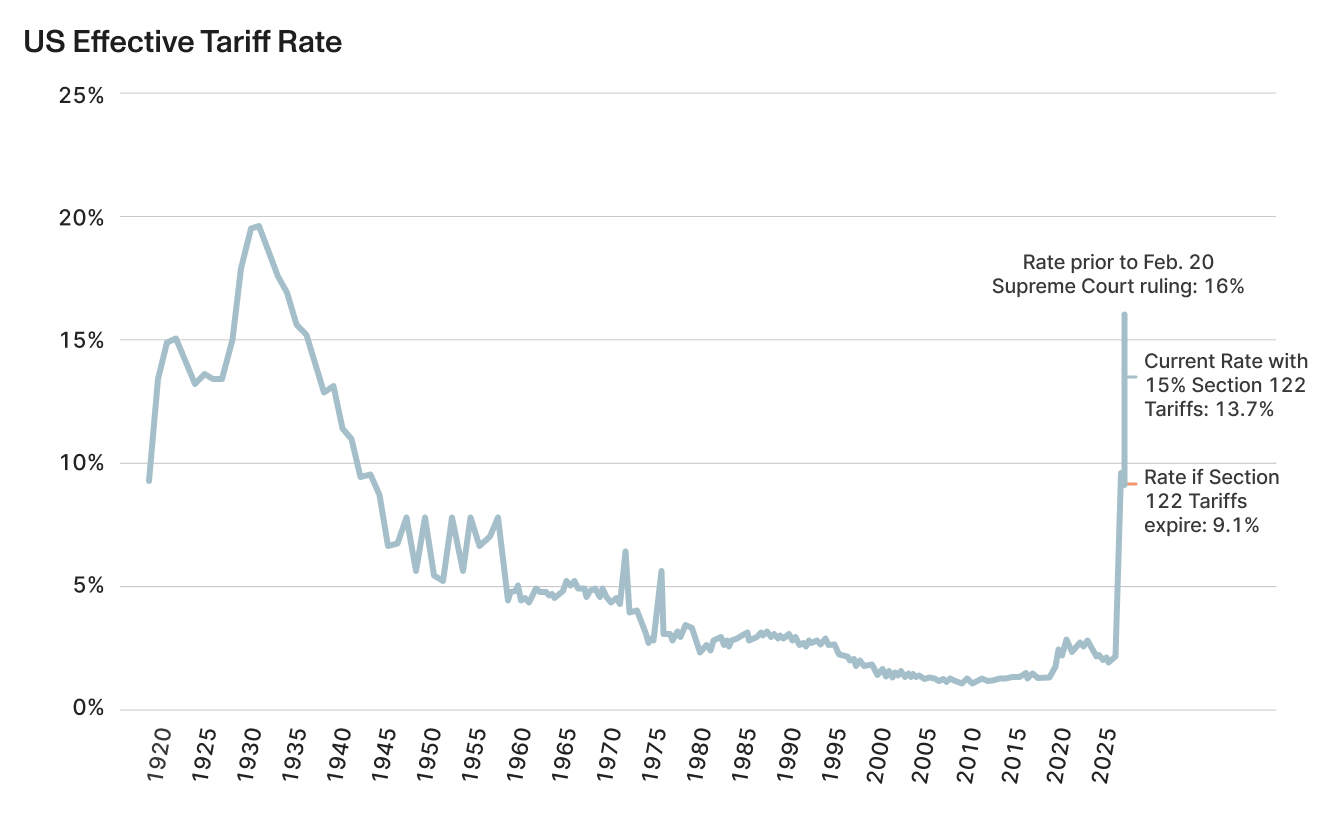

- Trade and tariff policy: The Supreme Court ruling on February 20th sharply constrained executive tariff authority, eliminating emergency tariff powers used since last April and replacing them with a temporary and lower 10% to 15% global tariff under Section 122. The extent and timing of possible refunds of the $150B tariffs paid so far remains uncertain.9

- AI revolution questions: Nvidia reported Q4 earnings results that exceeded analyst expectations, but the downward market price reaction reflected growing debate about the impact of AI investments.10

- Geopolitical risks (Iran): The U.S.–Israel strikes on Iran have increased short-term volatility, particularly in energy markets, though most analysts expect the conflict to be measured in weeks, not months or years.11

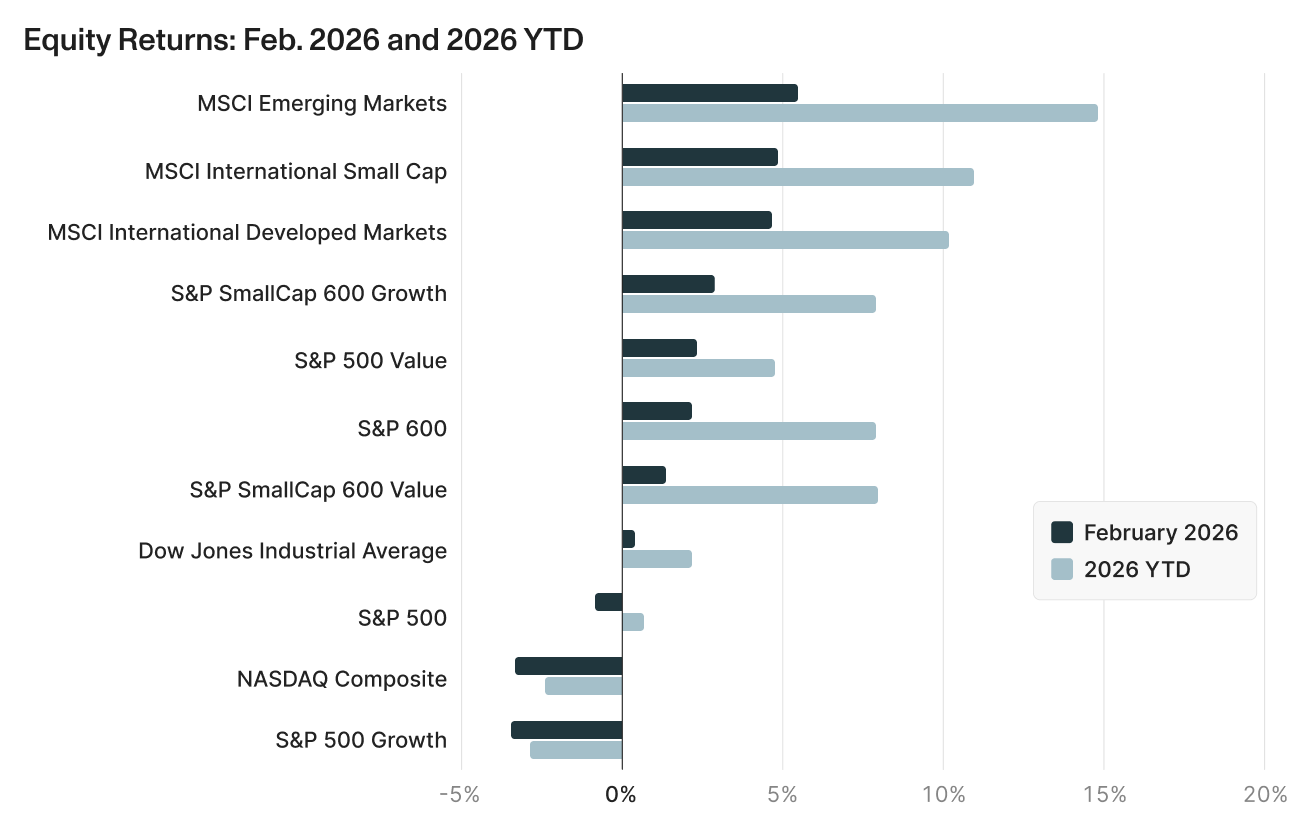

Stock leadership continues to broaden

Equity markets sent a clear message in February: leadership continues to broaden. While the S&P 500 declined modestly and is up just 0.68% year-to-date, performance beneath the surface was stronger, with international equities, emerging markets, and small-caps outperforming large-cap U.S. growth stocks.12 This rotation reflects several ongoing dynamics: strong earnings breadth beyond mega-cap technology, improving industrial momentum globally, a weaker U.S. dollar supporting international returns, and investor repositioning away from crowded growth exposures.

- International and Emerging Markets equities continued to lead in February as a softer dollar, improving global manufacturing data, and easing trade-policy tail risks supported returns abroad.

- U.S. Small Cap and Value stocks also fared well for the month, benefiting from broader participation across financials, industrials, and energy.

- Large Cap U.S. Growth & Tech stocks trailed meaningfully in February as valuation sensitivity and concentration risk in AI-related names as well as profit-taking weighed on mega-cap leaders.

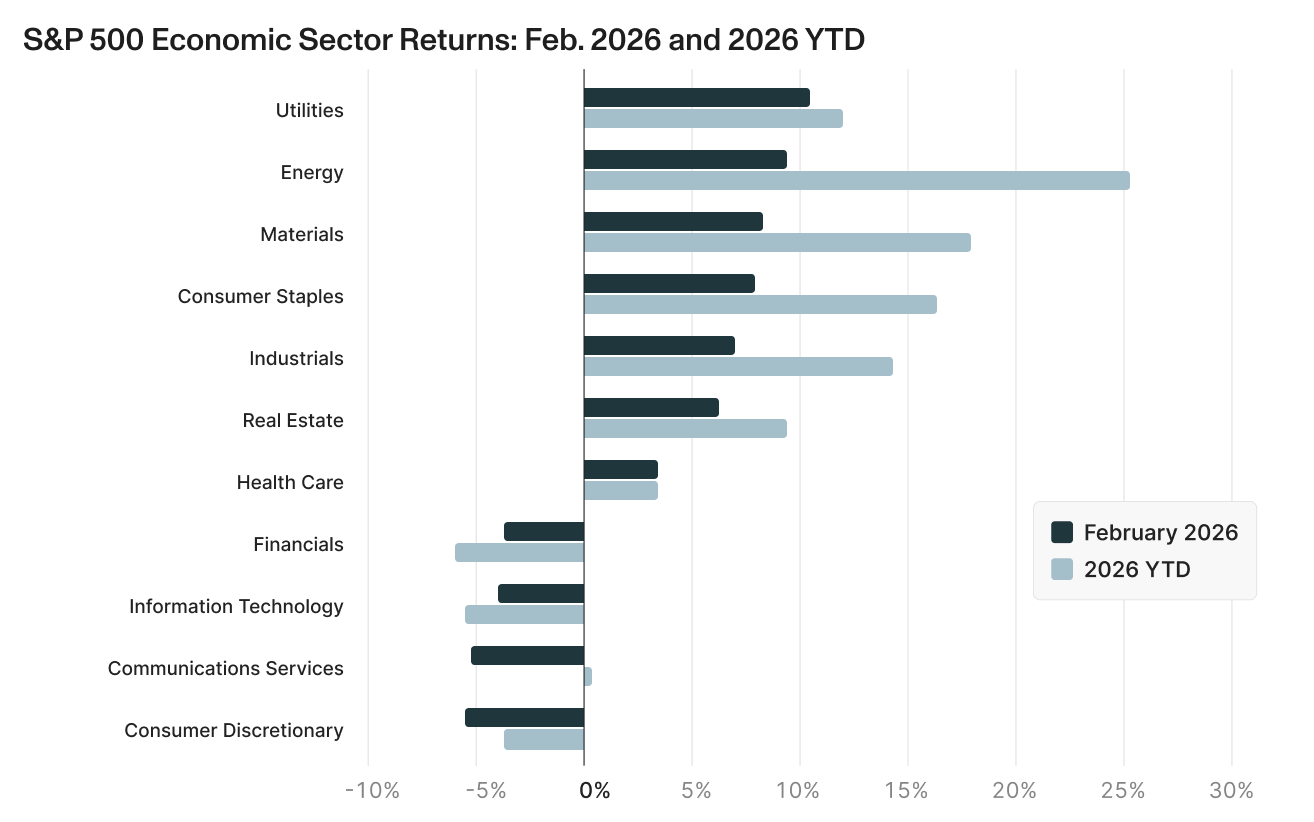

- S&P Sector returns:

- Defensive and real asset sectors led performance. Utilities, Energy, and Materials posted the strongest gains in February, reflecting demand for income, inflation sensitivity, and geopolitical risk hedging.

- Cyclical participation broadened beyond technology. Consumer Staples, Industrials, and Real Estate delivered solid returns, signaling improving global manufacturing momentum and rotation toward more economically sensitive areas of the market.

- Growth-oriented sectors lagged. Information Technology, Financials, Communication Services, and Consumer Discretionary trailed, reflecting valuation compression in mega-cap growth stocks and sensitivity to interest rate changes.

- Defensive and real asset sectors led performance. Utilities, Energy, and Materials posted the strongest gains in February, reflecting demand for income, inflation sensitivity, and geopolitical risk hedging.

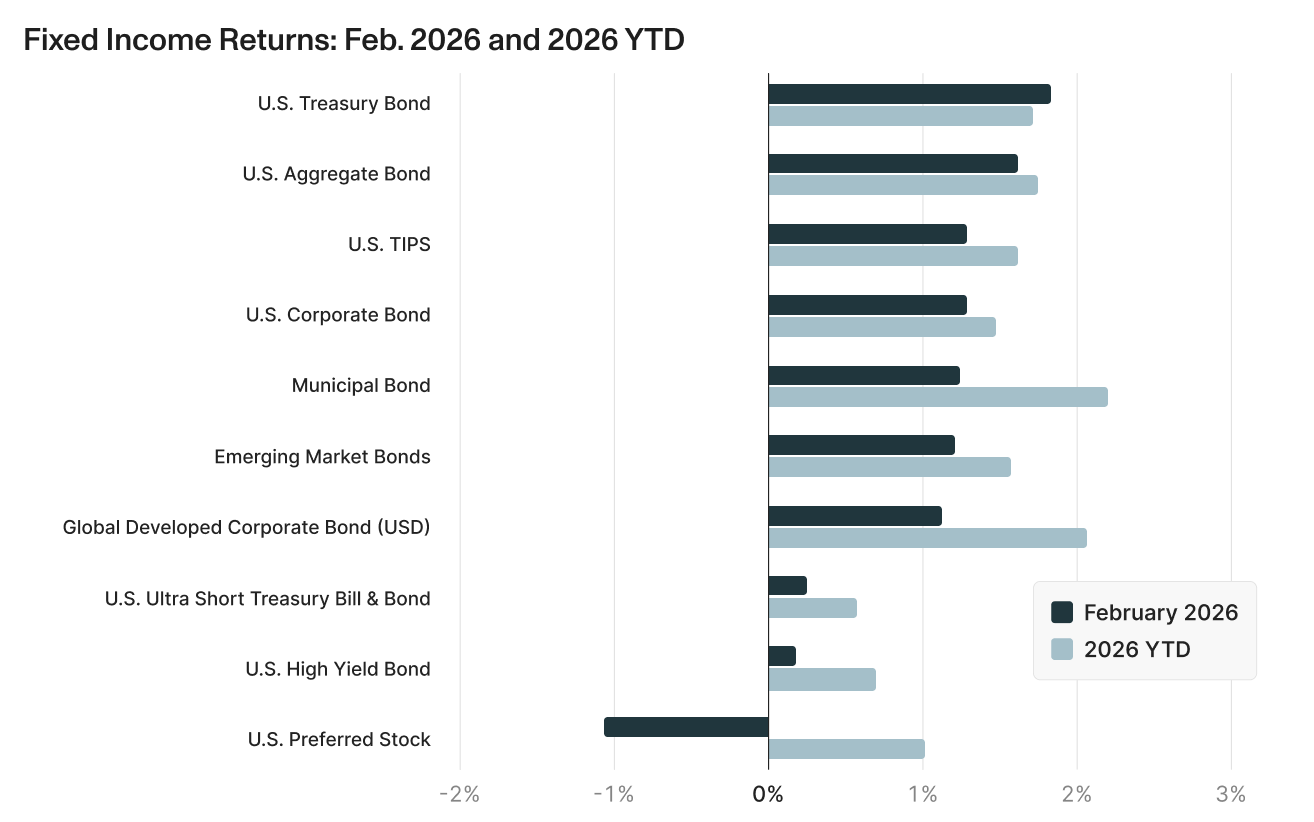

Bonds playing their historical role

Fixed income markets delivered broadly positive returns in February as yields stabilized amid a complex macro backdrop. Treasury yields moved modestly lower during the month, supporting duration-sensitive sectors. Credit markets remained stable, with spreads contained despite growing scrutiny in parts of private credit. Results were solid for high-quality fixed income, with more muted gains in riskier credit segments.17

- High-Quality Duration Performed Well: U.S. Treasury Bonds and the U.S. Aggregate Bond Index led in February and are solidly positive year-to-date, reflecting steady demand for high-quality bonds as a portfolio stabilizer.

- Inflation Protection and Global Bonds Added Value: U.S. TIPS, Municipal Bonds, and Global Developed Aggregate Bonds delivered healthy gains both for the month and year-to-date, benefiting from moderating inflation expectations and a steady global rate environment.

- Credit Positive but More Subdued: Investment-grade corporate bonds and emerging market bonds posted respectable gains, while high yield and ultra-short bonds lagged as their lower duration profiles limited upside. Preferred securities were the only segment to post a decline in February but remain modestly positive year-to-date.

Private Markets: A more selective environment

Private asset markets entered 2026 on stable footing, though dispersion beneath the surface is increasing. At the same time, higher interest rates relative to the past decade, liquidity scrutiny in retail-oriented vehicles, and evolving AI-driven disruption risks are forcing more careful underwriting and capital allocation decisions.

- Private Credit: Institutional demand for senior secured lending remains firm, and loan loss rates are still relatively contained.19 However, the gating of certain semi-liquid retail credit funds has highlighted structural liquidity mismatches.20 Concerns are concentrated in areas such as software lending and highly levered borrowers, reinforcing the importance of conservative loan-to-value ratios, senior positioning, and experienced managers.

- Private Real Estate: Residential housing, data centers, and certain necessity-based retail segments continue to show improving fundamentals, supported by demographic demand and AI-driven infrastructure investment.21 In contrast, traditional office and highly leveraged properties remain challenged. Transaction activity is gradually improving, but capital remains disciplined and valuation-sensitive.

- Private Equity & Venture Capital: Private equity continues to work through a backlog of several years of slower distributions. While deal volume has improved from 2024 lows, liquidity events remain below historical averages.22 Venture capital activity remains concentrated in AI and infrastructure-related themes, while broader technology and growth sectors are seeing more measured capital deployment. The environment favors operational value creation over multiple expansion.

Looking forward: Emerging risks and rewards

Changes in tariff and trade Policy

On February 20, the Supreme Court struck down the administration’s use of emergency powers under IEEPA to impose broad-based tariffs, ending the brief era of open-ended executive tariff authority. The administration responded with a temporary 10%–15% global tariff under Section 122 of the 1974 Trade Act. These tariffs would expire after 150 days unless Congress extends them. The change narrows the range of possible outcomes and increases policy predictability.23

The new blanket rate lowers tariffs for some countries and modestly raises them for others. Overall, the trade-weighted tariff rate appears below last year’s peak but above pre-2018 norms. More important than the exact rate is the reduced risk of sudden escalation.24

The decision also raises the prospect of significant tariff refunds. Estimates suggest that roughly $150 billion in previously collected tariffs could be subject to repayment, though the legal and administrative process is likely to be complex and prolonged.27 Questions remain about how refunds will flow through importers, distributors, and end consumers, and whether litigation could stretch the timeline into years. If ultimately paid, refunds would function as a modest fiscal stimulus — roughly half a percent of GDP — returning cash to businesses and potentially consumers.28 At the same time, they could widen the federal deficit and add marginal upward pressure to longer-term yields.

From an economic standpoint, the overall effect appears modestly pro-growth. Tariffs act as a tax on consumers and businesses, so limiting their scope and duration reduces that drag. Inflation pressures so far have been driven more by labor-intensive services and prior fiscal stimulus than by tariffs themselves. With inflation near 3% and goods prices stabilizing, the ruling is unlikely to materially alter the Federal Reserve’s near-term path.

Trade policy — what to watch:

- Congressional action before the 150-day expiration.

- Legal progress on tariff refunds.

- Retaliatory trade measures from Europe or China.

Iran conflict

The U.S. and Israeli joint strikes against Iran is the most serious Middle East flare-up in over a year, though markets are treating it as a contained event rather than a structural shock. The main economic impact comes through energy. Roughly 20% of global oil and LNG flows transit the Strait of Hormuz, and even partial disruption introduces a “security premium” into oil and gas prices.29 Crude prices have already moved higher, with estimates suggesting a limited conflict could push oil into the $80–$90 range, while a prolonged disruption lasting several weeks could see prices spike meaningfully higher.30 However, most strategic assessments suggest the conflict is likely measured in weeks rather than months, reducing the probability of a sustained supply shock. Importantly, the U.S. is now a net energy exporter, which partially cushions the domestic macro impact relative to past decades.31

From a market perspective, the pattern has been familiar: energy producers and defense stocks outperform, safe-haven assets such as gold move higher, and fuel-sensitive sectors like airlines face pressure.32 Thus far, broader equity markets have experienced volatility but not disorder, reflecting the view that while geopolitical risk has risen, the conflict does not yet threaten global growth outright. The larger question is whether elevated energy prices become persistent enough to complicate the inflation outlook. A temporary spike is unlikely to materially shift Federal Reserve policy, but a sustained oil price move toward triple digits could reintroduce inflation pressures just as goods prices were stabilizing. For now, markets are weighing short-term headline volatility against a base case of contained conflict.

Iran conflict — What to Watch:

- Whether shipping flows are disrupted beyond a brief period.

- Oil price movements

- Expanded involvement from Gulf states, Hezbollah, or other proxies.

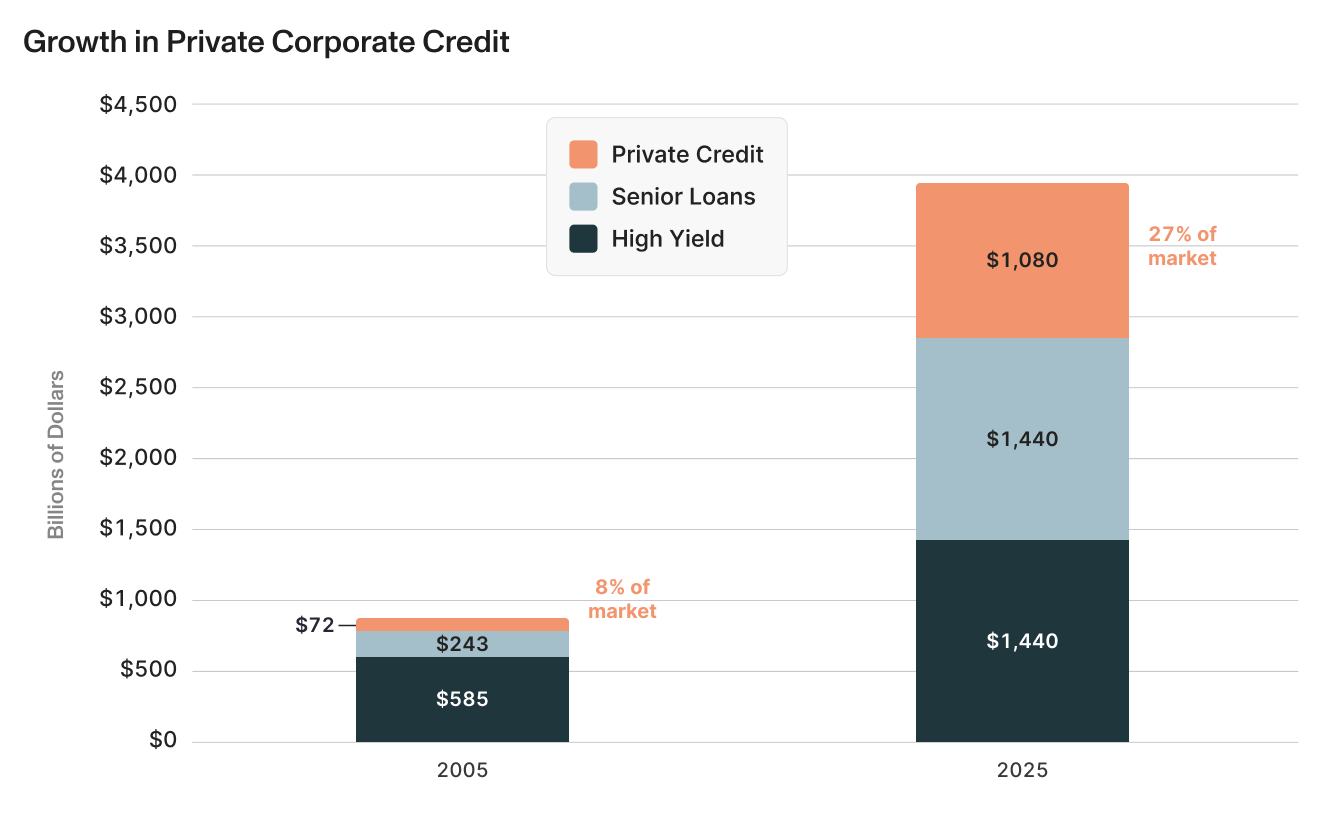

Private credit worries

Private credit has grown from a niche strategy into a core component of the below-investment-grade credit markets. Over the past two decades, assets in private credit have expanded nearly twentyfold, driven by tighter bank regulation post-GFC, sustained investor demand for higher yields, and the willingness of institutional allocators to provide long-duration capital.33 More recently, the asset class has moved further into the mainstream through semi-liquid and evergreen vehicles. Assets in evergreen alternative funds now approach $500 billion, with strong inflows over the past several years.34 The growth has been structural, not cyclical, with private credit now playing a meaningful role in corporate capital structures.

However, that rapid expansion has brought heightened scrutiny. The most visible recent catalyst was Blue Owl’s decision to halt quarterly redemptions in one of its retail-focused private credit vehicles and instead move toward an orderly wind-down funded by asset sales and loan repayments.36 While assets were reportedly sold near par value — suggesting no forced distress pricing — the gating decision highlighted a structural tension: inherently illiquid loans funded through vehicles offering periodic liquidity. At the same time, analysts have raised concerns about concentration risk, particularly exposure to software and technology borrowers that could face disruption from artificial intelligence. Some analysts have projected materially higher default rates in extreme AI-driven disruption scenarios, raising concerns about concentration risk.

Context matters. Thus far, realized loan losses across much of the private credit universe remain low by historical standards, and most portfolios are positioned in senior secured, first-lien structures with meaningful equity cushions beneath them. Institutional capital — which represents the majority of the investors in the asset class — has generally continued allocating, even as retail redemption requests have risen modestly. Several large managers have emphasized conservative loan-to-value underwriting, diversified portfolios, and active monitoring processes, noting that secondary market transactions have validated current valuations near par.37 38

While private credit continues to offer attractive income and senior positioning in the capital structure, the risk is dispersion in manager and fund results. As the asset class has grown, underwriting standards, liquidity structures, and sector exposures vary widely. In a higher-rate environment, manager selection and structural discipline matter more than ever.

Private Credit risks — What to Watch:

- Worsening defaults and loan losses

- Liquidity challenges in semi-liquid and evergreen vehicles

- Loosening underwriting standards and declining secondary market valuations

Earnings and the AI debate

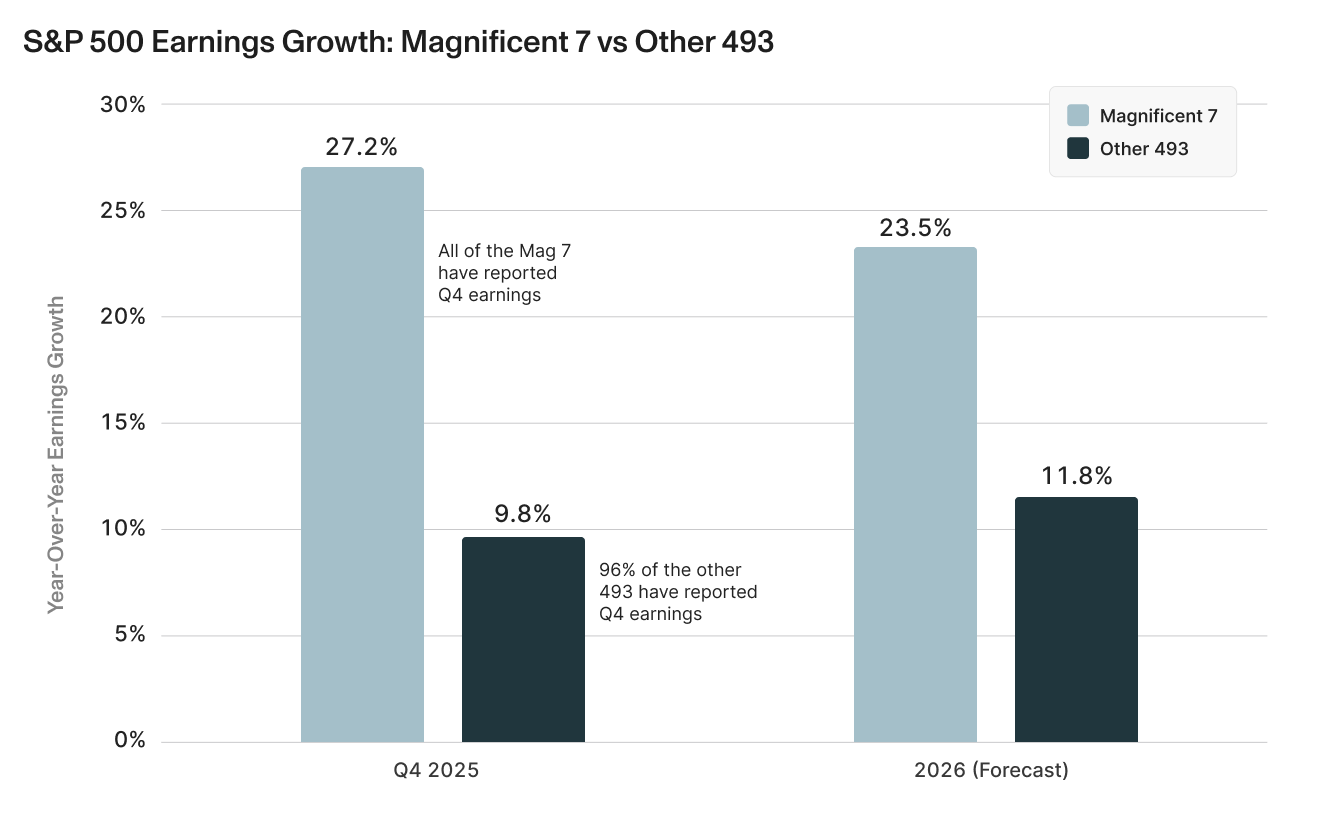

Corporate earnings remain one of the strongest pillars supporting the current market environment. Fourth-quarter results were solid again, with the S&P 500 delivering approximately 9% revenue growth — the strongest pace in three years — and earnings growth exceeding expectations in several key sectors. Importantly, growth is broadening beyond a narrow group of mega-cap technology names. Information Technology, Health Care, Communication Services, and Industrials were among the largest contributors to upside revenue surprises, signaling that demand remains resilient across both cyclical and secular segments of the economy. While analysts expect revenue growth to moderate slightly as 2026 progresses, current forecasts still call for mid- to high-single-digit sales growth and double-digit earnings growth for the full year.39

The “Magnificent 7” once again posted exceptional results in Q4, marking the tenth time in the past eleven quarters that the group has delivered earnings growth above 25%. Nvidia, in particular, reported another exceptional quarter, with revenue growth accelerating and forward guidance exceeding already-elevated expectations. Yet the market reaction was more muted than in prior cycles. Shares declined post-earnings, not because results disappointed, but because investors are increasingly focused on the sustainability of growth into 2027 and beyond. The debate has shifted from “Is growth strong?” to “How long can it persist at this level?” Data center demand remains robust and AI infrastructure build-out appears early in its cycle, but customer concentration and normalization risk remain key discussion points for investors.

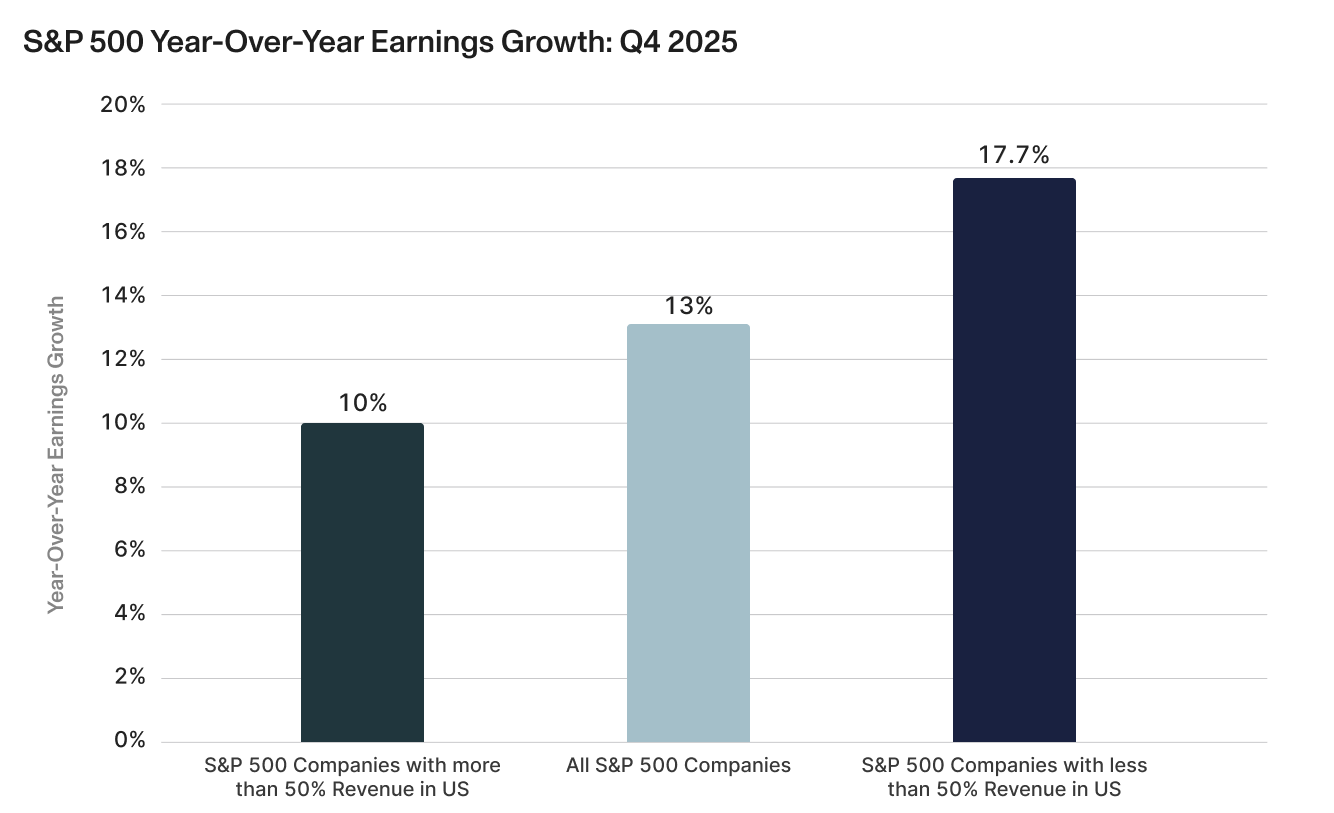

Another important development is the relative strength of companies with higher international revenue exposure. S&P 500 firms generating more than half of their revenue outside the United States reported materially stronger earnings and revenue growth than domestically focused peers.41 While Nvidia remains a significant contributor to that differential, the outperformance extends beyond a single company. A weaker U.S. dollar, trade rerouting, and stronger industrial activity abroad have supported multinational earnings, reinforcing the case for geographic diversification within equity portfolios.

Looking forward, analysts expect continued double-digit earnings growth for 2026, both for the Magnificent 7 and for the broader index.43 However, dispersion is increasing. Cyclical sectors tied to industrial recovery and capital spending are contributing more meaningfully, while growth expectations for certain technology names are being scrutinized more carefully.

At the center of this scrutiny is artificial intelligence. The bullish case argues that AI-driven capital expenditure, automation, and productivity gains could add meaningfully to U.S. GDP growth, support corporate margins, and sustain disinflation by reducing unit labor costs. Early signs of productivity improvement and strong AI-related capex lend credibility to this view.44 The more cautious perspective highlights risks: labor displacement in white-collar sectors, potential overinvestment in AI infrastructure, concentration risk among hyperscale buyers, and credit exposure in software and adjacent industries. In short, while AI may drive higher productivity and long-term value creation it also introduces transition risk and uneven outcomes across sectors.45 As with much of today’s market environment, the opportunity is significant, but so is the need for balance.

Earnings trends — what to watch:

- Breadth of earnings growth beyond mega-cap tech.

- Capex trends outside AI.

- Signs of labor market softening tied to productivity gains.

Navigating uncertainty

Periods of high perceived risks naturally tempt investors to overreact. In the current environment, the focus is on geopolitical headlines, shifting tariff policies, private credit scrutiny, or AI-driven enthusiasm. Yet markets are ultimately driven by more fundamental dimensions. Today’s backdrop includes solid and broadening earnings growth, improving industrial momentum, moderating inflation, set against elevated but contained geopolitical risk, alongside pockets of stress in more concentrated areas of the market.

The appropriate response for investors is not to position aggressively for one dominant outcome, but to recognize that rewards and risks always coexist. Diversification across geographies, styles, sectors, and asset classes remains the most reliable way to capture opportunity while managing risk. In an environment where leadership is rotating and dispersion is rising, balance in your investment portfolio is not a defensive posture — it is a strategic advantage.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.bea.gov/news/2026/gdp-advance-estimate-4th-quarter-and-year-2025

[2] https://www.ismworld.org/supply-management-news-and-reports/reports/ism-pmi-reports/pmi/february/

[3] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[4] https://www.spglobal.com/spdji/en/index-family/equity/

[5] https://www.bls.gov/news.release/cpi.nr0.htm

[6] https://www.bls.gov/news.release/archives/ppi_02272026.htm

[7] https://www.bea.gov/data/personal-consumption-expenditures-price-index

[8] https://www.bls.gov/news.release/empsit.nr0.htm

[9] https://budgetlab.yale.edu/research/state-tariffs-february-21-2026

[10] https://www.cnbc.com/2026/02/26/nvidia-nvda-stock-price-q4-earnings.html Past performance is not indicative of future results.

[11] https://www.cnbc.com/2026/03/02/iran-israel-us-conflict-oil-jumps-trump-netanyahu-what-is-next.html

[12] https://www.spglobal.com/spdji/en/index-family/equity/

[13] https://www.spglobal.com/spdji/en/index-family/equity/

[14] https://www.msci.com/end-of-day-data-search

[15] https://www.nasdaq.com/market-activity/index/comp/historical

[16] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[17] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[18] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[19] Blackstone, Private Markets Hot Topics Feb. 27, 2026

[20] Cliffwater, “After Misstep, Blue Owl Gets It Right, Unlike the Press”, February 22, 2026

[21] https://www.commercialsearch.com/news/a-better-year-for-cre/

[22] https://www.fa-mag.com/news/private-equity-s-dry-spell-now-worse-than-2008-crisis--bain-says-85967.html

[23] https://www.franklintempleton.com/articles/2026/institute/quick-thoughts-us-supreme-court-strikes-down-trump-tariffs

[24] https://budgetlab.yale.edu/research/state-tariffs-february-21-2026

[25] https://budgetlab.yale.edu/research/state-tariffs-february-21-2026

[26] https://fred.stlouisfed.org/series/B235RC1Q027SBEA

[27] https://www.franklintempleton.com/articles/2026/institute/quick-thoughts-us-supreme-court-strikes-down-trump-tariffs

[28] https://www.franklintempleton.com/articles/2026/institute/quick-thoughts-us-supreme-court-strikes-down-trump-tariffs

[29] https://www.carlyle.com/carlyle-compass/rise-of-the-security-premium

[30] https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/tmt/the-us-and-israel-strike-iran-what-it-could-mean-for-markets

[31] https://www.carlyle.com/carlyle-compass/rise-of-the-security-premium

[32] https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/tmt/the-us-and-israel-strike-iran-what-it-could-mean-for-markets

[33] https://www.bcred.com/resources/

[34] https://www.connectmoney.com/stories/evergreen-alternative-funds-surge-to-493b-as-private-markets-go-mainstream/

[35] https://www.bcred.com/resources/

[36] Cliffwater, “After Misstep, Blue Owl Gets It Right, Unlike the Press”, February 22, 2026

[37] Cliffwater, “After Misstep, Blue Owl Gets It Right, Unlike the Press”, February 22, 2026

[38] Blackstone, Private Markets Hot Topics Feb. 27, 2026

[39] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[40] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[41] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[42] https://insight.factset.com/sp-500-companies-with-more-international-exposure-reporting-higher-earnings-growth-for-q4

[43] https://insight.factset.com/magnificent-7-companies-reported-earnings-growth-above-25-for-q4

[44] https://www.citadelsecurities.com/news-and-insights/2026-global-intelligence-crisis/

[45] https://www.citiresearch.com/p/2028gic