Earnings Over Headlines

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

Following a volatile March driven by geopolitical escalation and surging oil prices, equity markets staged a sharp and sustained rebound, with the S&P 500 reaching new all-time highs. Instead of focusing on near-term uncertainty surrounding the Iran conflict, investors shifted their attention to resilient economic data and exceptionally strong corporate earnings. That divergence reflects the simple reality that markets are priced on expectations over current events.

While surging oil and gasoline prices have pushed inflation higher and weighed on sentiment, the underlying fundamentals have remained intact. This gap between what the headlines suggest and what the fundamentals show has defined the current environment. The key question moving forward is whether markets can continue to look through near-term shocks, or whether elevated inflation and policy uncertainty begin to challenge what has so far been a remarkably resilient backdrop.

April 2026 at a glance

- Economic Growth: Economic activity remained resilient, supported by solid consumer spending and continued strong business investment despite elevated uncertainty.1

- Earnings: Q1 earnings reported so far have been exceptionally strong, led by mega-cap technology companies. Growth is tracking nearly 30% year-over-year with the vast majority of companies beating expectations.2

- Equity markets: U.S. equities rebounded sharply in April, with the S&P 500 rising nearly 10% and the NASDAQ up over 15%. Many indices reached new all-time highs as investors looked past geopolitical risks and focused on improving fundamentals.3

- Fixed Income: Bond returns were modest as inflation concerns kept yields elevated and delayed expectations for rate cuts.4

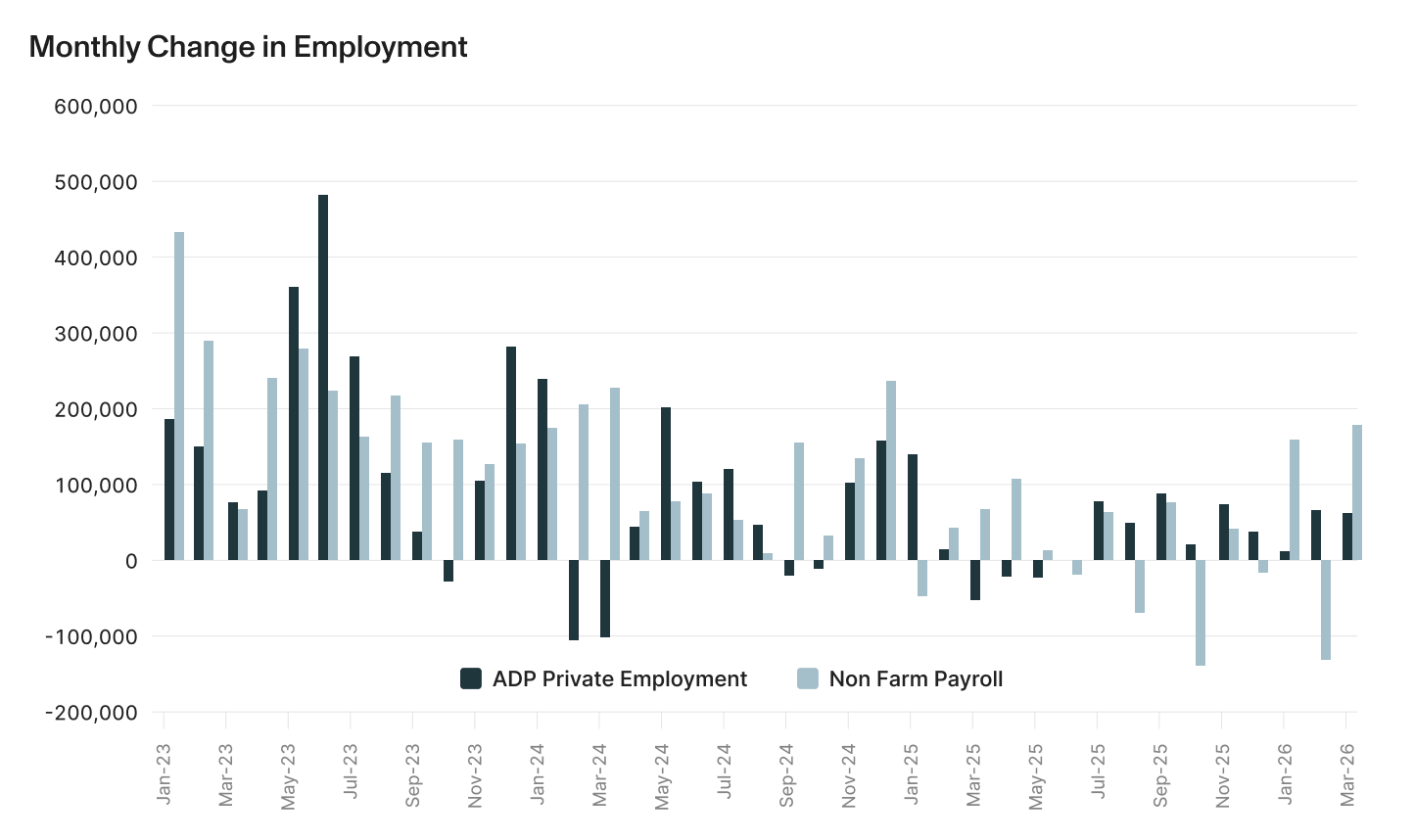

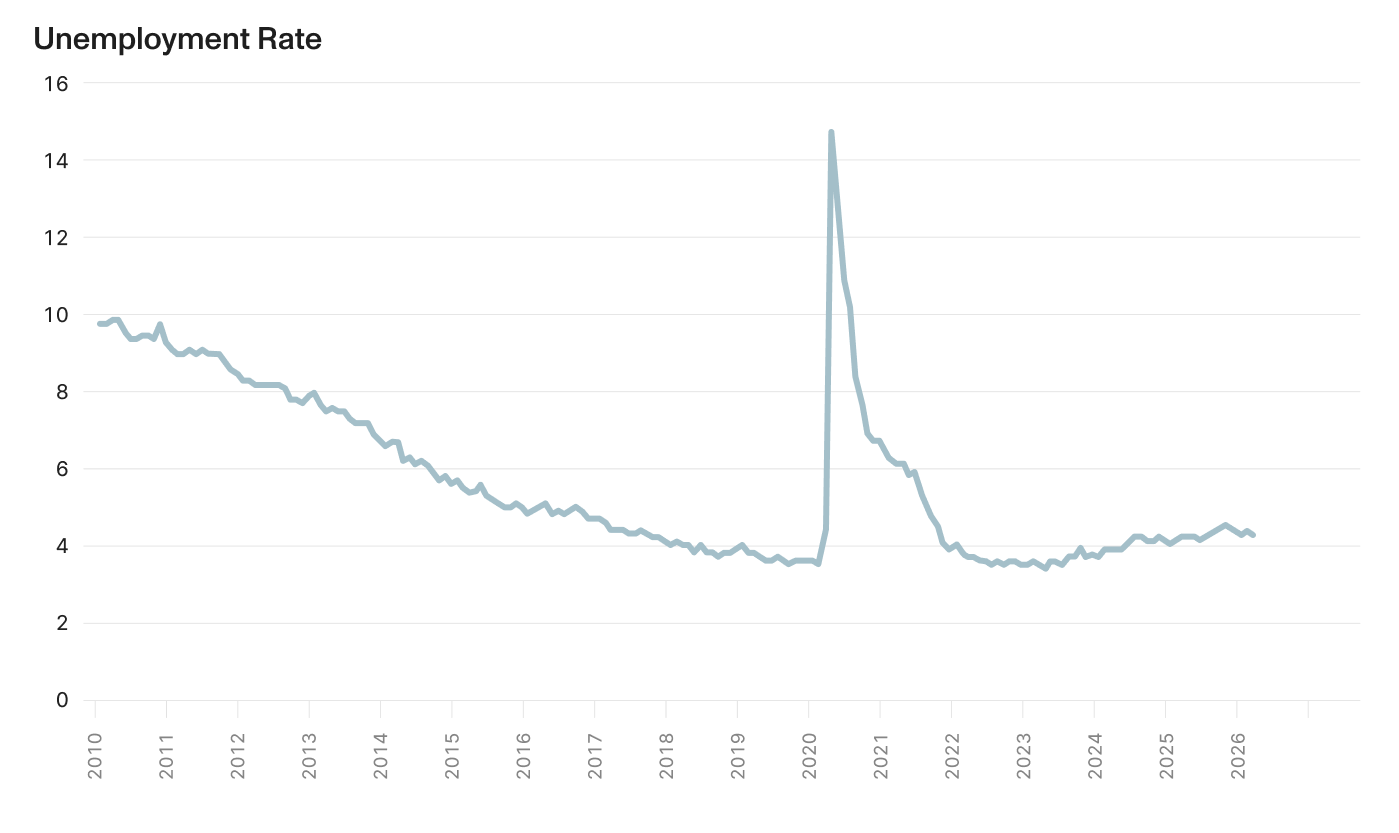

- Inflation and Employment: Inflation moved higher due to rising energy prices while job growth moderated and the unemployment rate held steady at 4.3%.5 6

- The Federal Reserve: In Jerome Powell’s last meeting as Chair, the Fed held rates steady and maintained a data-dependent stance, balancing elevated inflation against a stable labor market and increased geopolitical uncertainty.7

- AI revolution questions: AI remains a central driver of market performance and earnings growth, with continued acceleration in investment and adoption across sectors.

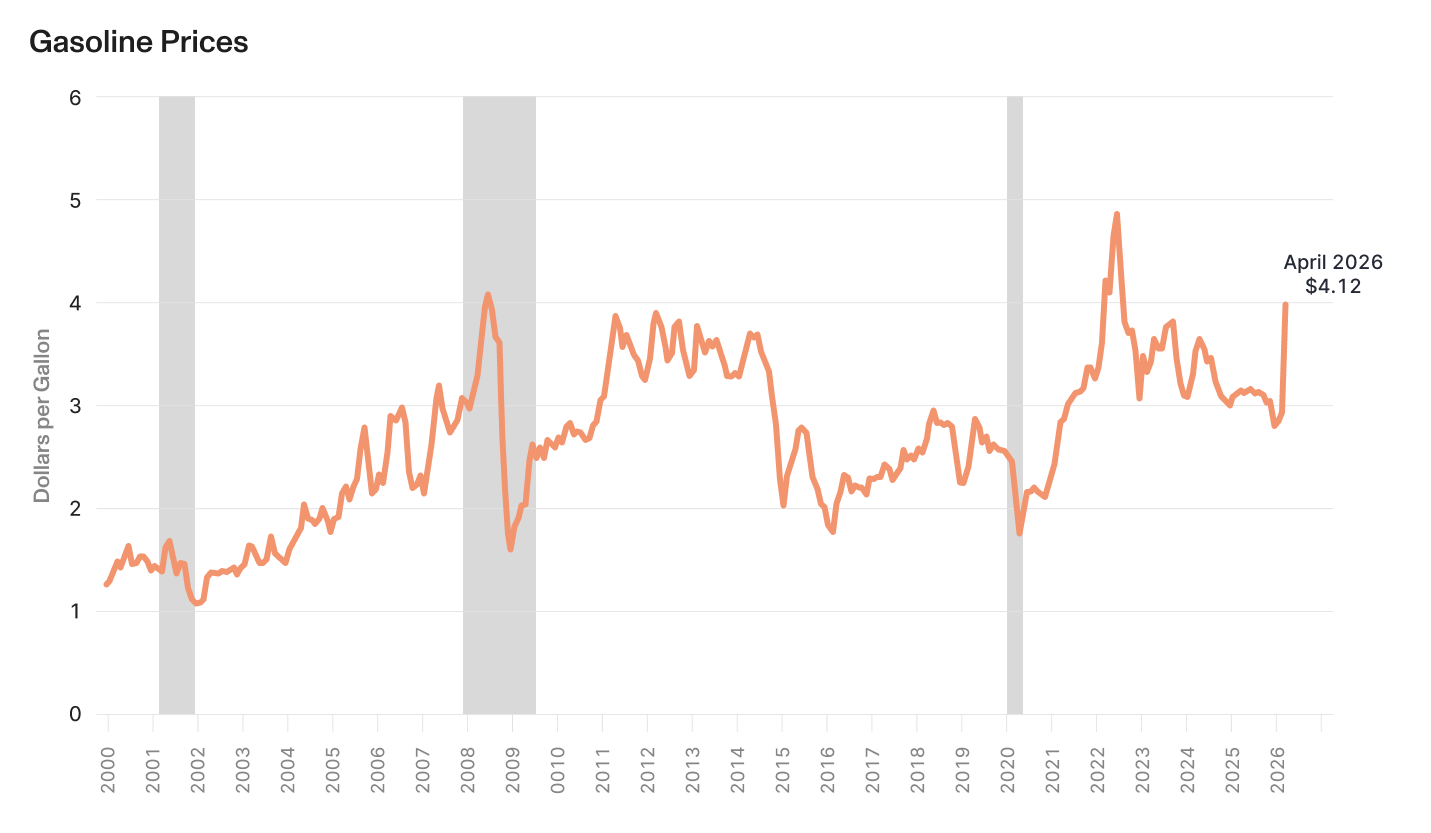

- Geopolitical risks (Iran): The Iran conflict disrupted global oil flows and pushed crude above $100 per barrel, driving gasoline prices higher and contributing to renewed inflation concerns.

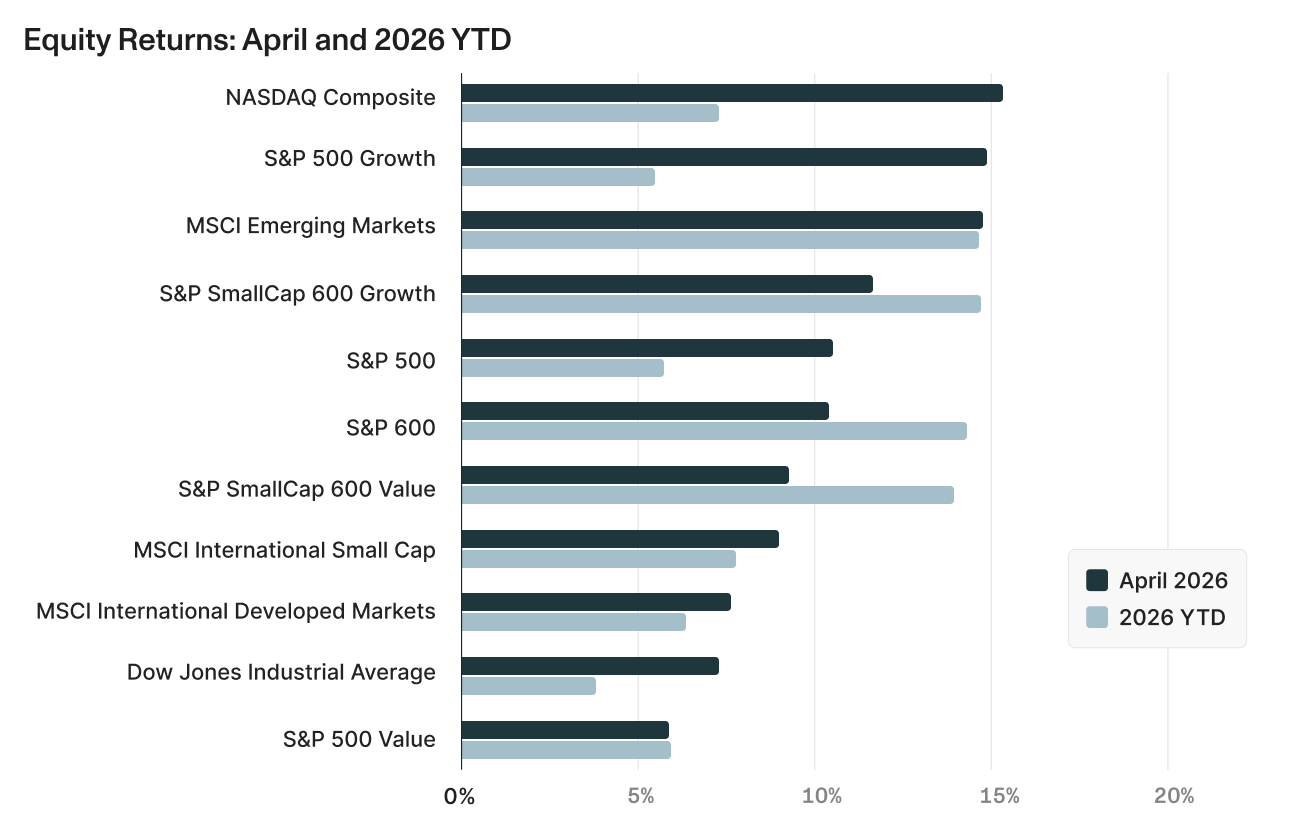

Stocks surge to erase Q1 losses

Equity markets delivered a broad and powerful rebound in April, with major indices recovering March’s losses and pushing to new highs. The rally was driven by a combination of easing geopolitical fears, strong Q1 earnings, and continued momentum in AI-related sectors, reinforcing the market’s focus on fundamentals over near-term uncertainty.

- Growth stocks led the rebound, with the NASDAQ Composite rising 15.31% and the S&P 500 Growth index up 14.79%, while the broader S&P 500 gained 10.49% for the month.

- Performance extended beyond large-cap growth, with small caps (S&P 600 +10.41%) and emerging markets (+14.73%) posting strong gains in April and outperforming on a year-to-date basis (both up just over 14%+ YTD).

- While growth outperformed value in April (S&P 500 Growth +14.79% vs. Value +5.87%), year-to-date returns between the two styles remain more balanced.

- S&P Sector returns:

- Communication Services (+18.54%) and Information Technology (+17.47%) led the market, reflecting strength in mega-cap technology and AI-driven earnings.

- Energy (-3.46%) and Health Care (-0.45%) were the only sectors to decline in April. Despite the pullback, energy remains the top-performing sector year-to-date (+33.46%). Health Care continued to lag, driven by weaker earnings trends and company-specific pressures.

- Cyclical sectors such as Industrials (+7.93%) and Real Estate (+8.76%) outperformed more defensive areas like Utilities (+2.09%) and Consumer Staples (+3.10%) as investors looked past oil price related growth concerns.

Bonds weaken on inflation concerns

Fixed income markets delivered modestly positive returns in April, but performance lagged equities as rising oil prices and the resulting inflation concerns kept upward pressure on yields and delayed expectations for Fed rate cuts. The environment continued to favor riskier credit and higher-yielding segments over traditional duration exposure.

- Credit-sensitive sectors led, with Preferreds (+4.54%), Emerging Market Bonds (+2.11%), and High Yield (+1.69%) outperforming, reflecting improving risk sentiment and support from strong corporate earnings.

- More traditional core bond exposures were muted, with the U.S. Aggregate Bond index (+0.11%) and investment-grade corporates (+0.45%) posting modest gains. Treasuries were slightly down (-0.07%) for the month and remain negative year-to-date, with longer-dated bonds lagging treasury bills.

- Inflation-linked bonds (TIPS +1.15%) rose on concerns that oil prices will remain higher for longer than anticipated.

Private Markets: A more selective environment

- Private Equity & Venture Capital: Headline deal volumes improved in the first quarter, though activity was largely driven by a small number of large transactions, most notably the SpaceX acquisition of xAI, masking softer underlying activity in the broader market.13 Elevated volatility and uncertainty around rates and geopolitics have made underwriting more difficult and widened bid-ask spreads. Exit activity also remains constrained, with IPO markets still in an uneven recovery phase. There is a growing pipeline of high-quality companies and the potential for a reopening of the IPO window, but investors are likely to remain selective outside of AI-driven sectors.

- Private Credit: Fundamentals remain stable, with defaults still low, but liquidity dynamics for many funds are presenting an important stress test. Elevated redemption requests in semi-liquid structures have increased the number of funds prorating withdrawals. A report from Bank of America estimated that these redemption requests in non-traded BDCs are likely to peak in Q2.14 While higher yields continue to support private credit demand, the environment is becoming more differentiated, reinforcing the importance of manager selection, portfolio transparency, and liquidity management.

- Private Real Estate: The sector remains the most challenged segment of private markets. Higher interest rates continue to pressure valuations and financing conditions, while fundraising has slowed and distributions remain limited. The result is a market still in the process of repricing. Although select sectors, like data centers and logistics, are benefiting from continued strong demand, a broader recovery is likely to be gradual and uneven.

Looking forward: Geopolitical risks cloud fundamental strength

The Fed: changes in leadership but no change in mandate

The Federal Reserve continues to navigate a complex environment shaped by its dual mandate of stable prices and maximum employment. Inflation has moved back to the forefront of the policy discussion, driven largely by the recent surge in oil and gasoline prices. Headline inflation, as measured by the Personal Consumption Expenditures (PCE) index, has reaccelerated toward 3.5%, while core inflation excluding food and energy has remained more stable, but is still well above the Federal Reserve’s 2% target. The divergence between headline and core measures reflects the outsized impact of energy prices, which have historically been one of the most volatile components of inflation.

The recent increase in gasoline prices, driven by disruptions to global oil supply, is particularly important because of its impact on consumers. Unlike many other components of inflation, energy prices are highly visible and can influence both inflation expectations and consumer behavior. While energy-driven inflation is often viewed as transitory, the potential for second-order effects from any prolonged higher prices complicates the policy outlook, particularly if elevated prices begin to feed into the costs of goods and services more broadly.

At the same time, the labor market remains relatively stable. While job growth has slowed, unemployment has held steady and broader labor indicators suggest a gradual normalization rather than deterioration. Recent data suggests the labor market is no longer a primary source of inflationary pressure, allowing the Fed to focus more directly on price stability without the need to aggressively respond to wage-driven inflation.

Still, job growth has slowed, and while layoffs remain relatively contained at the aggregate level, there are signs of softness in certain industries and job openings have gradually declined from prior peaks. This reflects a labor market that is cooling through reduced hiring rather than widespread job losses.

Structural factors are playing an important role in slowing job growth. Changes in immigration, demographics, and the growing influence of artificial intelligence are reshaping both labor supply and demand. Recent analysis suggests that the labor market may now be operating near a “zero-growth equilibrium,” where relatively little job creation is needed to maintain a low unemployment rate due to a smaller and slower-growing labor force.17

Overall, the labor market remains resilient, but the trajectory is clear: slower job growth, fewer openings, and a more balanced supply-demand dynamic. For the Fed, this reinforces the view that the employment side of the dual mandate is largely in equilibrium, shifting the focus more squarely toward inflation as the primary constraint on policy decisions.

The Fed has maintained a data-dependent stance and held rates steady, signaling a willingness to ease policy over time but only as inflation shows clearer signs of moderating. The path to rate cuts has become less certain, particularly if oil prices remain elevated and keep headline inflation above target.

Adding to this uncertainty is the upcoming transition in Federal Reserve leadership. Chair Powell has indicated that he intends to remain on the Board of Governors after stepping down as Chair, which would provide a degree of continuity in policy discussions and institutional knowledge. However, the appointment of Kevin Warsh as the next Chair introduces the potential for a shift in emphasis, particularly around the focus on inflation and the communication of policy.

Warsh has been explicit in emphasizing the importance of Federal Reserve independence, stating that he would not be influenced by political pressure and rejecting the notion that he would serve as a “proxy” for the administration’s calls for immediate rate cuts.

It’s important to remember that monetary policy decisions are made collectively by the FOMC rather than unilaterally by the Chair, and that market forces — particularly inflation expectations and bond yields — serve as an additional check on policy actions. In addition, Warsh has historically been viewed as more hawkish on inflation, which could translate into a more cautious approach to easing policy. As a result, while the tone of communication and the policy framework may evolve under new leadership, a sharp deviation from a data-dependent approach remains unlikely.

In this environment, the most likely path forward is a prolonged pause, with rate cuts dependent on a normalization in oil prices and a continued moderation in inflation.

The Dual Mandate — what to watch:

- Will energy-driven inflation prove temporary, or begin to impact broader price pressures and expectations?

- How will the Fed balance stable employment with still-elevated inflation in determining the timing of rate cuts?

- To what extent will new leadership and political pressure influence the pace of rate cuts and communication of monetary policy?

Economic growth bolstered by spending and investment

Economic growth remained positive in the first quarter, with initial estimates showing GDP increasing approximately 2.0%, reflecting continued resilience despite elevated geopolitical uncertainty and higher energy prices.21 As shown in the chart, growth was supported by a balanced contribution across consumption, investment, government spending, and exports, offsetting a surge in imports. This composition highlights an economy that continues to expand on multiple fronts, rather than relying on a single driver.

Consumer spending remains the foundation of growth, supported by stable employment and steady income gains, even as sentiment indicators have weakened. At the same time, business investment has been a notable contributor, reflecting tremendous ongoing spending tied to AI, infrastructure, and capacity expansion. This investment cycle, especially in technology and energy-related sectors, continues to provide an important offset to external shocks, reinforcing the underlying strength of the economy.

Despite these growth drivers, risks remain somewhat elevated. Higher oil prices are acting as a tax on consumers, reducing discretionary spending power and creating a headwind for growth, while tighter financial conditions continue to weigh on more rate-sensitive sectors. As a result, growth expectations have moderated, with a slower pace of expansion likely in the coming quarters. Importantly, however, the U.S. economy appears less vulnerable to energy shocks than in prior cycles. Increased domestic production, improved efficiency, and a more diversified economic base reduce the likelihood that higher oil prices alone will trigger a recession, while strong corporate balance sheets and ongoing investment continue to provide support.

From a cycle perspective, the economy appears to be in a late-stage expansion — slowing, but still growing. Labor markets are stable, inflation remains above target but is no longer broadly accelerating, and monetary policy is restrictive but not tightening further. Recession risks remain present but are more likely to stem from external or policy shocks — particularly if elevated energy prices persist — rather than from underlying economic imbalances. For now, the most likely path forward is continued, albeit slower, growth rather than an imminent downturn.

Economic Growth — what to watch:

- The pace of consumer spending as higher energy prices weigh on real incomes.

- Will AI-related business investment continue to match lofty expectations?

- Will higher energy prices increase the risks of recession?

Surging earnings expectations

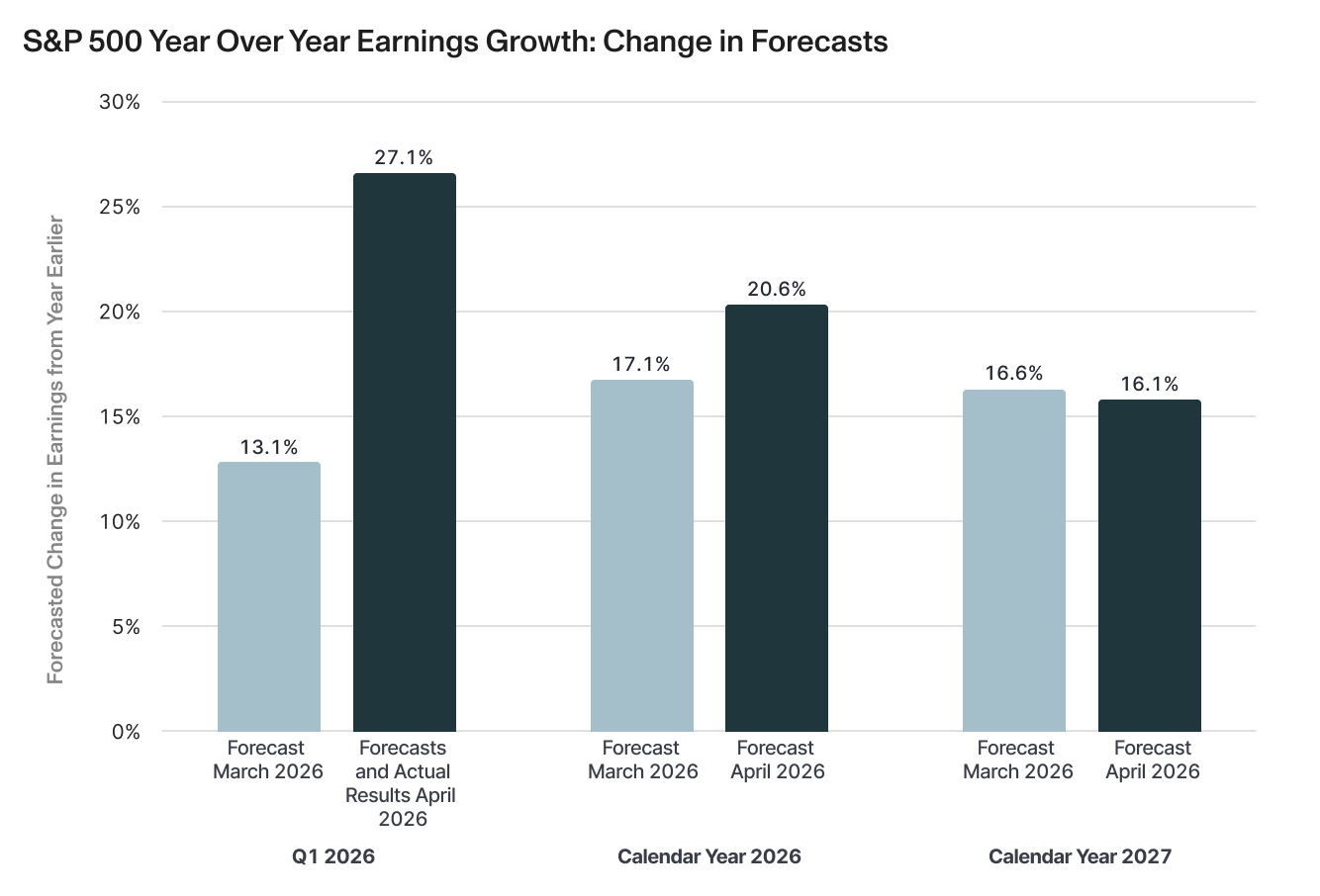

Corporate earnings strength remains the cornerstone of the current market environment. Both the magnitude and persistence of growth have exceeded expectations in Q1. The quarter is now tracking approximately 27% year-over-year earnings growth, marking the strongest expansion since 2021 and extending a multi-quarter streak of double-digit gains.23 This continuation of strong earnings growth in the face of geopolitical uncertainty and rising input costs reinforces the underlying strength of corporate fundamentals.

As shown in the charts, the most notable development this quarter has been the significant upward revision in both actual and expected earnings growth. Q1 earnings growth expectations increased from approximately 13% forecasted in March to over 27% based on both reported results so far as well as upward revisions to forecasts. Reported results also show a higher-than-usual level of positive earnings surprises. This trend extends beyond the current quarter, with full-year 2026 earnings forecasts revised higher (from 17% to over 20%) and 2027 estimates remaining solid in the mid-teens, pointing to continued momentum.

A key driver of this strength has been the combination of revenue growth and expanding profit margins. Companies have not only benefited from resilient demand from both consumers and businesses, but have also demonstrated the ability to manage costs effectively, with margins continuing to expand.

Looking ahead, analysts expect earnings growth of approximately 20%+ for full-year 2026, supported by continued AI investment, stable economic growth, and resilient margins. Even in the face of higher energy costs, companies have thus far demonstrated an ability to manage input pressures and maintain profitability.

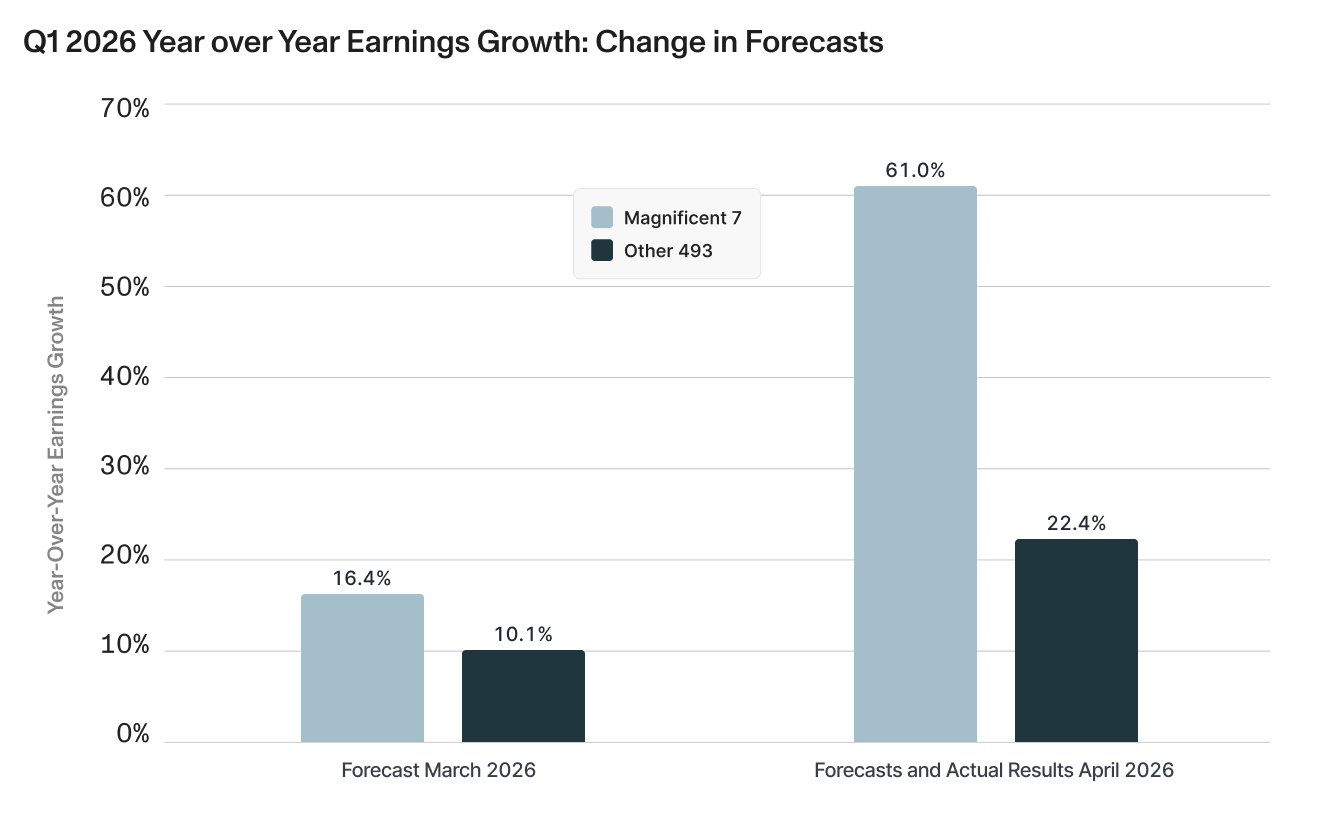

Growth continues to be led by technology and AI-related sectors. Upward revisions to earnings growth forecasts have been particularly pronounced within the largest technology companies. The “Magnificent 7” saw Q1 earnings growth expectations increase dramatically from roughly the mid-teens in March to over 60% currently. This remarkable growth highlights both the strength of demand and the scale of operating leverage within these businesses. The remaining companies in the S&P 500 also saw solid upward revisions in growth, with forecasts increasing into the low-20% range currently, more than double levels from a month ago.

This dynamic underscores two important trends. First, AI-driven investment and demand continue to disproportionately benefit large-cap technology companies, reinforcing their outsized contribution to overall earnings growth. Second, the broader market is still participating in the earnings expansion, supported by improving fundamentals and easier comparisons in more cyclical sectors. The result is a market where leadership remains concentrated, but the underlying earnings backdrop is becoming incrementally more broad-based.

Management commentary in the Q1 earnings calls points to a slightly more cautious tone looking forward.27 While current demand remains solid and near-term results have been strong, companies are increasingly acknowledging the potential impact from macroeconomic uncertainty and adopting more measured guidance. This suggests that while the earnings backdrop remains supportive, expectations may be moderating as the year progresses.

Still, any moderation has not yet materialized, even in the face of external shocks. In a market environment shaped by geopolitical risks and policy uncertainty, this continued strength in corporate profitability remains the primary support for equity valuations and market performance.

Earnings trends — what to watch:

- Can earnings growth sustain its current pace?

- Will margin strength persist if input costs, particularly energy, remain elevated?

- Does earnings growth broaden further beyond mega-cap technology and AI-driven sectors?

Looking ahead

April reinforced a critical lesson patient investors already know: markets are ultimately driven by fundamentals, not headlines. Despite the conflict in the Middle East, oil above $100, and persistent inflation, equities moved higher on the back of strong earnings and resilient economic data.

The tension in this environment is real. Energy prices are weighing on consumers, inflation is complicating the path for monetary policy, and management teams are getting more cautious in their guidance. These aren’t small risks. But the economy is still growing, the labor market is stable, and corporate balance sheets are strong. For now, fundamentals are winning.

The backdrop doesn’t guarantee smooth sailing — external shocks can still derail a fundamentally sound market. But in the absence of major imbalances, the more likely outcome is that the market continues to surprise on the upside.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

[1] https://www.bea.gov/news/2026/gdp-advance-estimate-1st-quarter-2026

[2] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[3] https://www.spglobal.com/spdji/en/index-family/equity/

[4] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[5] https://www.bea.gov/news/2026/personal-income-and-outlays-march-2026

[6] https://www.bls.gov/news.release/empsit.nr0.htm

[7] https://www.federalreserve.gov/newsevents/pressreleases/monetary20260429a.htm

[8] https://www.spglobal.com/spdji/en/index-family/equity/

[9] https://www.msci.com/end-of-day-data-search

[10] https://www.nasdaq.com/market-activity/index/comp/historical

[11] https://www.spglobal.com/spdji/en/index-family/equity/us-equity/sp-sectors/#overview

[12] https://www.spglobal.com/spdji/en/index-family/fixed-income/

[13] https://pitchbook.com/news/articles/record-q1-m-a-masks-a-more-selective-market2

[14] https://pitchbook.com/news/articles/private-credit-bdc-redemption-requests-likely-to-peak-in-q2-2026-bofa

[15] https://www.bea.gov/news/2026/personal-income-and-outlays-march-2026

[16] https://www.eia.gov/dnav/pet/pet_pri_gnd_a_epmr_pte_dpgal_w.htm

[17] Alpine Macro, “Global Strategy: U.S. Labor Market: From Zero To Hero – Special Report”, April 20, 2026

[18] https://adpemploymentreport.com/

[19] https://www.bls.gov/news.release/empsit.nr0.htm

[20] https://www.bls.gov/news.release/empsit.nr0.htm

[21] https://www.bea.gov/news/2026/gdp-advance-estimate-1st-quarter-2026

[22] https://www.bea.gov/news/2026/gdp-advance-estimate-1st-quarter-2026

[23] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[24] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[25] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[26] https://insight.factset.com/sp-500-earnings-season-update-may-1-2026

[27] Alpine Macro, “Equity Strategy: All Eyes On Me: Q1 Earnings Impressions”, April 28, 2026