Great Expectations

Compound is a digital family office for entrepreneurs, professionals, and retirees who want the personal touch of a dedicated advisor accompanied by a beautiful digital experience.

The path of investment returns is often about reconciling delivered fundamental results with the expectations for those fundamentals built into asset prices. When actual results come in below expectations, related asset prices typically fail to align with the updated and disappointing reality. Depending on the level of expectations relative to the magnitude of the shortfall, the downward price adjustment can be immediate and large and, depending on how broadly the expectations have impacted asset prices, can extend to the broad market and create impacts on the economy more generally. Of course, the opposite can also be true. When actual results come in above expectations, that can lead to upward moves in asset prices and a positive feedback loop to the economy.

As the rest of 2025 plays out, that reconciliation process will be especially important along two dimensions: the timing and magnitude of interest rate cuts; and, the trajectory of corporate earnings, especially among the fast growing tech and AI-related industries. Asset prices currently reflect high expectations that the Fed will cut rates by 25 basis points at its September meeting and an increasing probability of one or two more similar cuts over the remainder of the year.1 Perhaps more importantly, equity markets, which have been especially driven by a handful of US technology and AI-related companies in the past several years, are pricing in continued exceptional earnings growth from these companies and the sector in general.

Disappointment on either of these expectations - no or fewer rate cuts, any slowing in AI-related earnings growth - will likely lead to a sharp decline in equity prices, a substantial rotation in asset class leadership, or both.

We will explore these two areas later in this month's market update, but first…

Last month at a glance

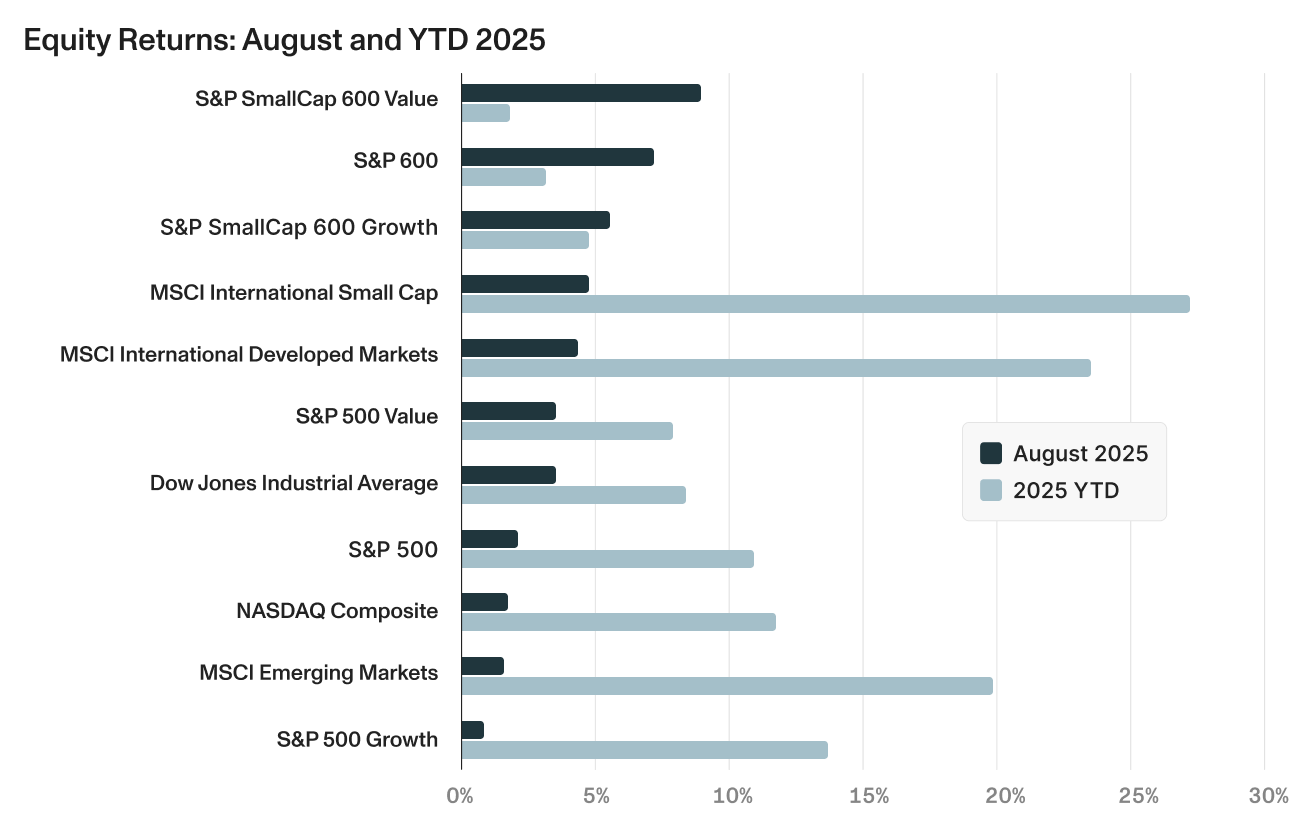

- Market Performance: Equity markets rose across the board in August with a notable rotation into small cap and value stocks.2 Bond returns were also strong on falling interest rates.3

- Private Markets: IPOs have raised $23 billion so far this year, similar to the 2024 pace. Much of this year’s activity has been in high-growth tech and AI industries, but the IPO calendar for the rest of 2025 includes broader sectors like biotech, restaurants, banks, and energy companies. IPO performance has been strong with the Renaissance IPO Index up 15.8% year-to-date.4

- Trade Policy Developments: Tariff policies continued to evolve during August with higher levels imposed on Switzerland, Brazil and India while pauses were extended for China and Mexico and a deal was struck with the European Union.5 As the month ended, a U.S. appeals court ruled that most of the tariffs were illegal, but allowed the tariffs to remain in place through October 14 to allow the administration time to file an appeal with the U.S. Supreme Court.6

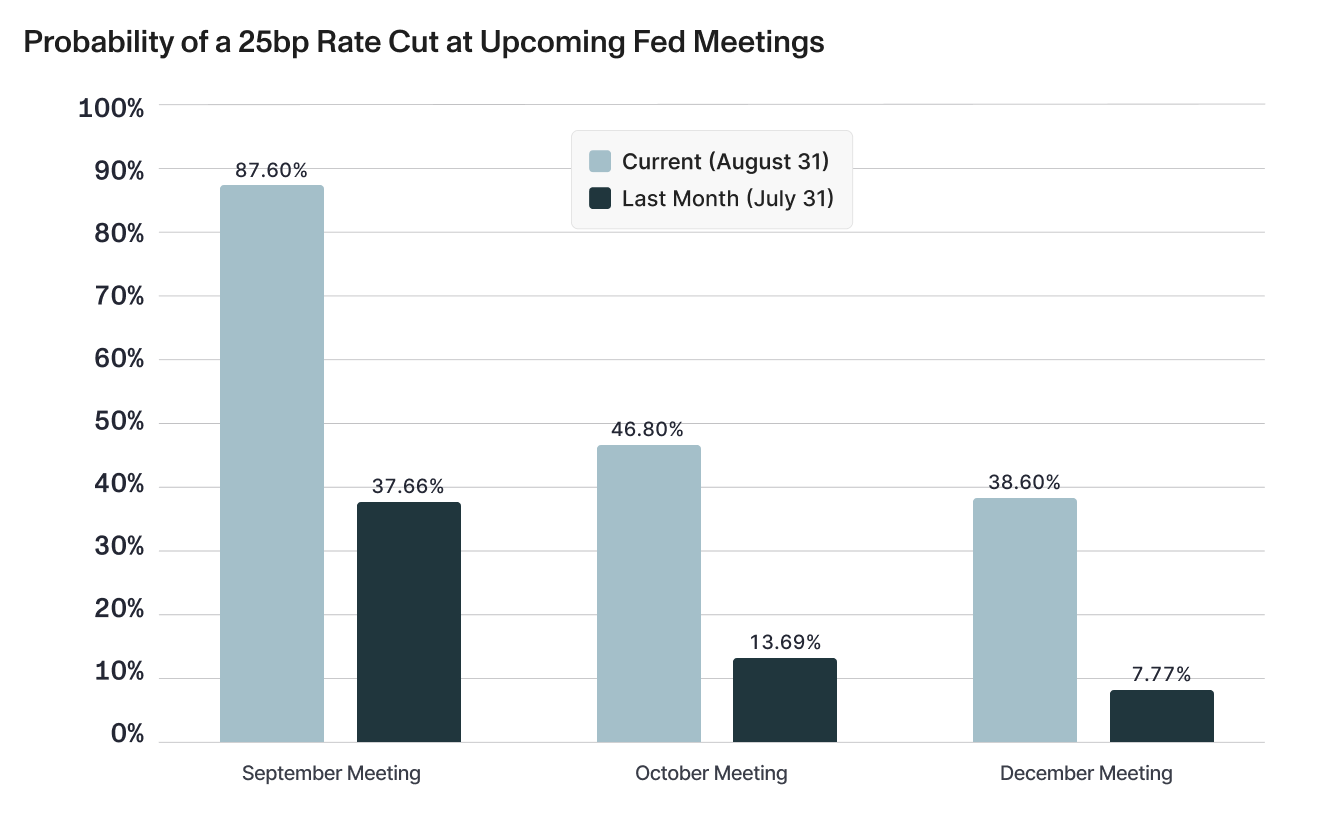

- Federal Reserve: Fed Chair Powell signaled openness to rate cuts at Jackson Hole, with markets now pricing in a 90% probability of a 25bp September cut.7 8 President Trump sought to remove Fed Governor Lisa Cook, a move that will likely end up before the U.S. Supreme Court and test the limits of the Fed’s independence.

- Economic Data: Reports in August showed continued challenges in bringing inflation down to the Fed’s 2% target, with the core PCI gauge up 0.3% from the prior month and 2.9% above year earlier levels.9 Jobless claims rose over the month, underscoring potential softening in the labor markets.10 Consumer spending rose at the fastest pace since March, though consumer confidence fell slightly.11 12

- Earnings: With 98% of companies reporting, 81% of S&P 500 companies beat EPS estimates, the highest since Q3 2023, with an overall annual earnings growth of +11.9%. The “Magnificent 7” continued to lead the pack, with all seven companies beating their estimates, reporting an aggregate 26.6% earnings growth.13

Stocks continue to push higher

Powell's Jackson Hole dovish comments bolstered equity markets over the month, pushing many indices to record highs. The optimistic outlook also drove a rotation into small cap and value stocks as well as a broadening of industry leadership beyond the mega cap tech segments. A general risk-on sentiment prevailed as investors seemed to embrace the likelihood of Fed rate cuts as a positive for growth prospects rather than a reaction to increased recession risk.

- Small-caps broadly outperformed large-caps in August, both in the US and internationally, suggesting risk-on sentiment broadening.14

- Value led growth in both large and small cap, but continued to trail for the full year.

- International markets were mixed with developed market large and small cap stocks rising over 4% for the month while emerging markets rose just 1.47%.15

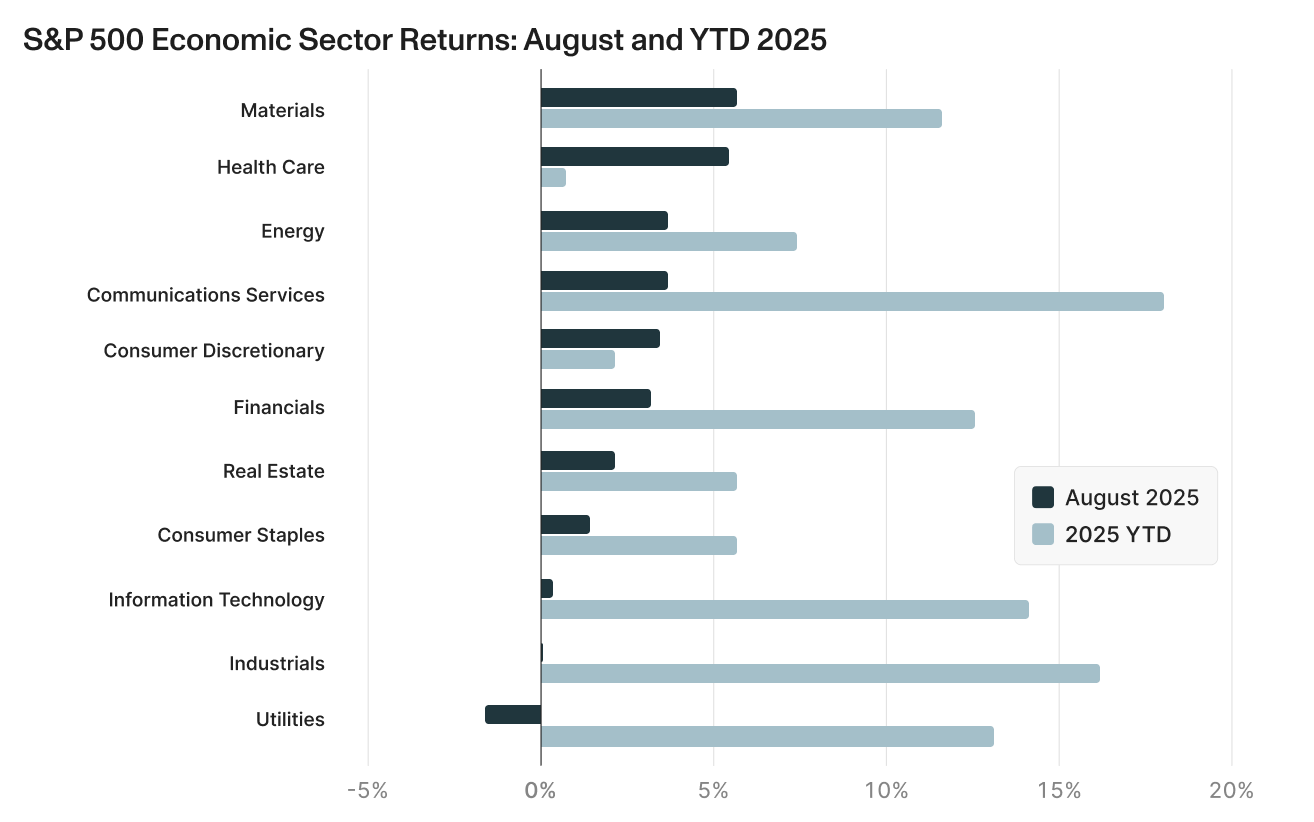

- Sector performance within the S&P 500 showed a rotation out of the dominant technology sectors.16

- Cyclical sectors rallied with materials (+5.76%) and energy (+3.64%) leading performance.

- Information Technology (+0.34%) was the third-worst performing sector despite still solid earnings growth.

- Defensive sectors were mixed with consumer staples (+1.59%) and utilities (-1.58%) underperforming while health care (+5.38%) surged on a rebound from beaten up stocks like United Healthcare and Eli Lilly.

Rates fall and boost fixed income

Fixed income returns rose across the board in August as investors embraced lower volatility and yield curve normalization with the Fed’s pivot to lowering rates. While short-term rates predictably fell on the shift in policy expectations, declines in rates at the longer end of the curve and the solid returns in high yield suggests the bond market found the evolving rate policy supportive to the credit cycle rather than signaling distress.21

- TIPS leadership (+1.54%) in August, despite a more dovish Fed, suggests investors remain focussed on price pressures from tariffs and solid economic growth.

- Global bonds (+1.45% developed markets and +1.34% emerging markets) slightly outperformed the U.S. Aggregate (+1.20%), benefiting from currency and global rate dynamics.

- U.S. High Yield (+1.25%) outperformed Treasuries (+1.06%) as credit spreads tightened on economic optimism and Fed easing expectations.

- Ultra Short Treasury (+0.38%) lagged all fixed income sectors as increased expectations for Fed cuts reduced short-term yields.

- Municipal bonds (+0.87%) continued to lag and are flat so far in 2025, well behind all other fixed income segments, as a supply surge and tax policy uncertainty have hurt muni fundamentals.

Looking forward: Key areas to watch

1. The September rate cut

In many comments in his Jackson Hole conference speech, Fed Chair Powell solidified expectations of rate cut at the FOMC meeting on September 16-17. One sentence in particular summarized the change in policy positioning: “Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”22 Increased expectations of a 25bp rate cut in the target Fed Funds range at the Fed’s September meeting had already been building over the month of August, but the speech solidified those expectations. We can see the magnitude of the change in those expectations in the chart below. The CME Group’s Fed Watch estimates the market’s expectation for rate cuts implied by 30-Day Fed Funds futures prices.23 That probability stands at 87.6% as of the end of August, up substantially from 38% at the end of July.

Expectations for similar cuts at the October and December meetings are lower than for the September meeting, but also dramatically higher than they were in July. Taken together, current expectations are for a “certain” rate cut in September and likely at least one more cut during the rest of 2025.

Of course, these probabilities can change. As Chair Powell also reiterated in Jackson Hole, “Monetary policy is not on a preset course. FOMC members will make these decisions, based solely on their assessment of the data and its implications for the economic outlook and the balance of risks. We will never deviate from that approach.”25 That data dependency is well understood by the market and thus warrants keeping an eye on unfolding measures of inflation and the longer-term inflation expectations of consumers and businesses. Actual inflation reported in August came in close to expectations, but still above the Fed’s 2% target. The Core (excluding Food and Energy) Personal Consumption Expenditures price index showed inflation up 2.9% from a year ago, the same as the prior month, but up from earlier this year.26 The Michigan Consumer Sentiment Survey showed a small increase in both year ahead and longer-term inflation expectations in August after falling in the prior two months.27

Failure to cut rates by at least 25bp at the September meeting would force a substantial reconsideration of the interest rate trajectory that is currently reflected in asset prices. That would most certainly lower those prices broadly even though the reason for not cutting would mean that the employment side of the Fed’s dual mandate to keep inflation low and employment high was showing a still strong economy. Not cutting in September would also likely warrant a substantial response from President Trump and the administration who have called for even more than 25bp of cuts.29

Rate Cuts — What to look out for:

- Signs of rising inflation. There will be no new PCE inflation report “hard data” before the September meeting, so survey reports (“soft data”) of increased inflation, especially price increases related to tariffs, wage pressures or rising inflation expectations could change investors confidence in a September cut.

- September jobs report. Since the Fed’s change in posture is also connected to perceptions of a slowing labor market, any substantial strengthening in the employment situation could change expectations.

2. Earnings expectations are high - can the AI engine keep delivering?

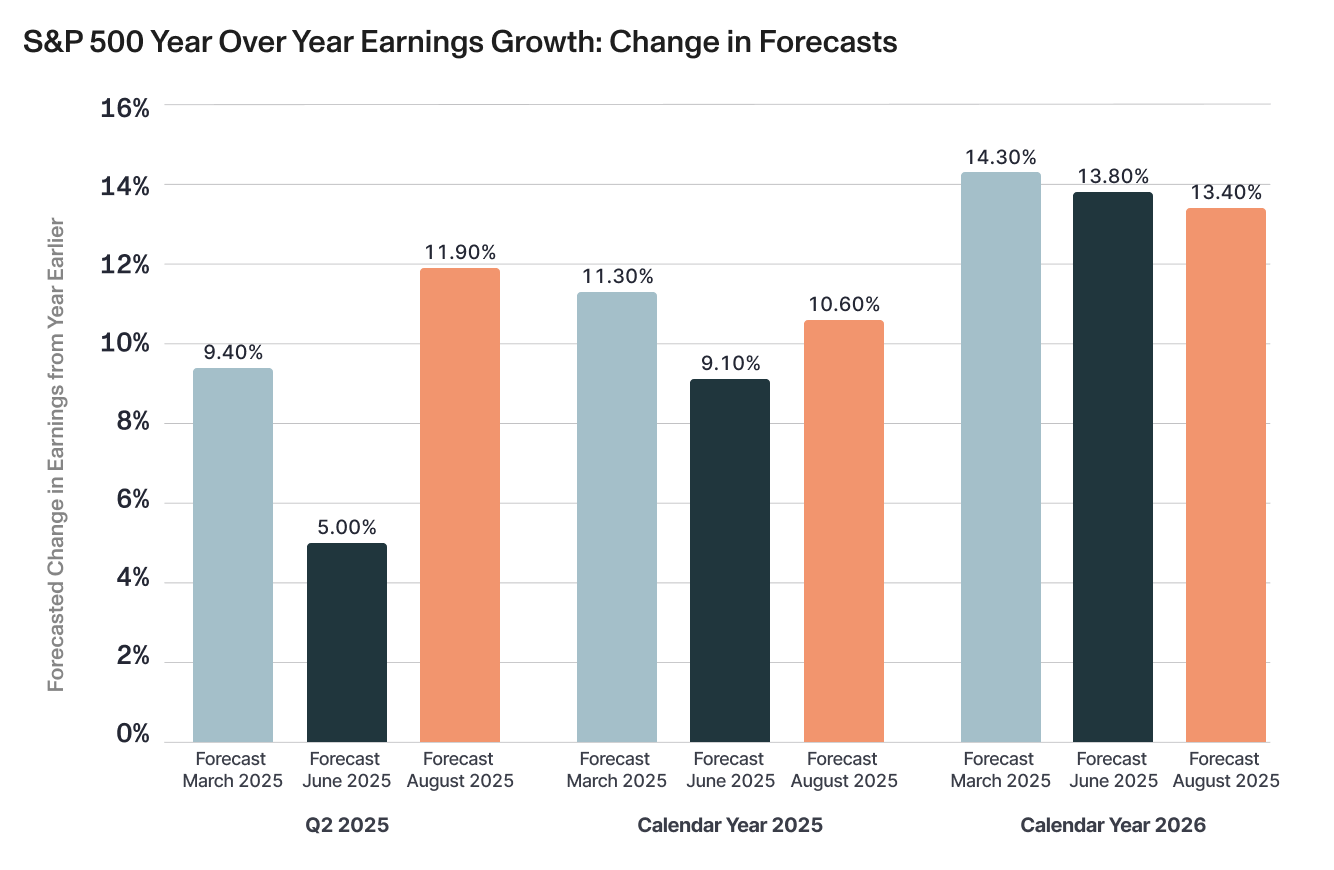

Entering the second quarter, earnings expectations had fallen substantially on fears that tariffs would have a relatively large impact on sales and profits. Actual results for the 98% of S&P 500 companies that have reported Q2 results so far, show that those expectations were far too pessimistic. Eighty-one percent of companies beat the lowered earnings estimates for the quarter, showing an earnings growth rate of 11.9%, more than double the initial 5% expectation from June 30th and even higher than the 9.4% pre-tariff expectation.30 Revenue growth came in at a robust 6.4%, marking the highest revenue growth rate since Q3 2022. While there is still some uncertainty about the shifting of spending and inventory accumulation and unwinding between the first and second quarters as consumers and businesses looked to front run tariffs, the overall earnings picture in Q2 has left investors feeling that the impact from tariffs will be less than initially feared.

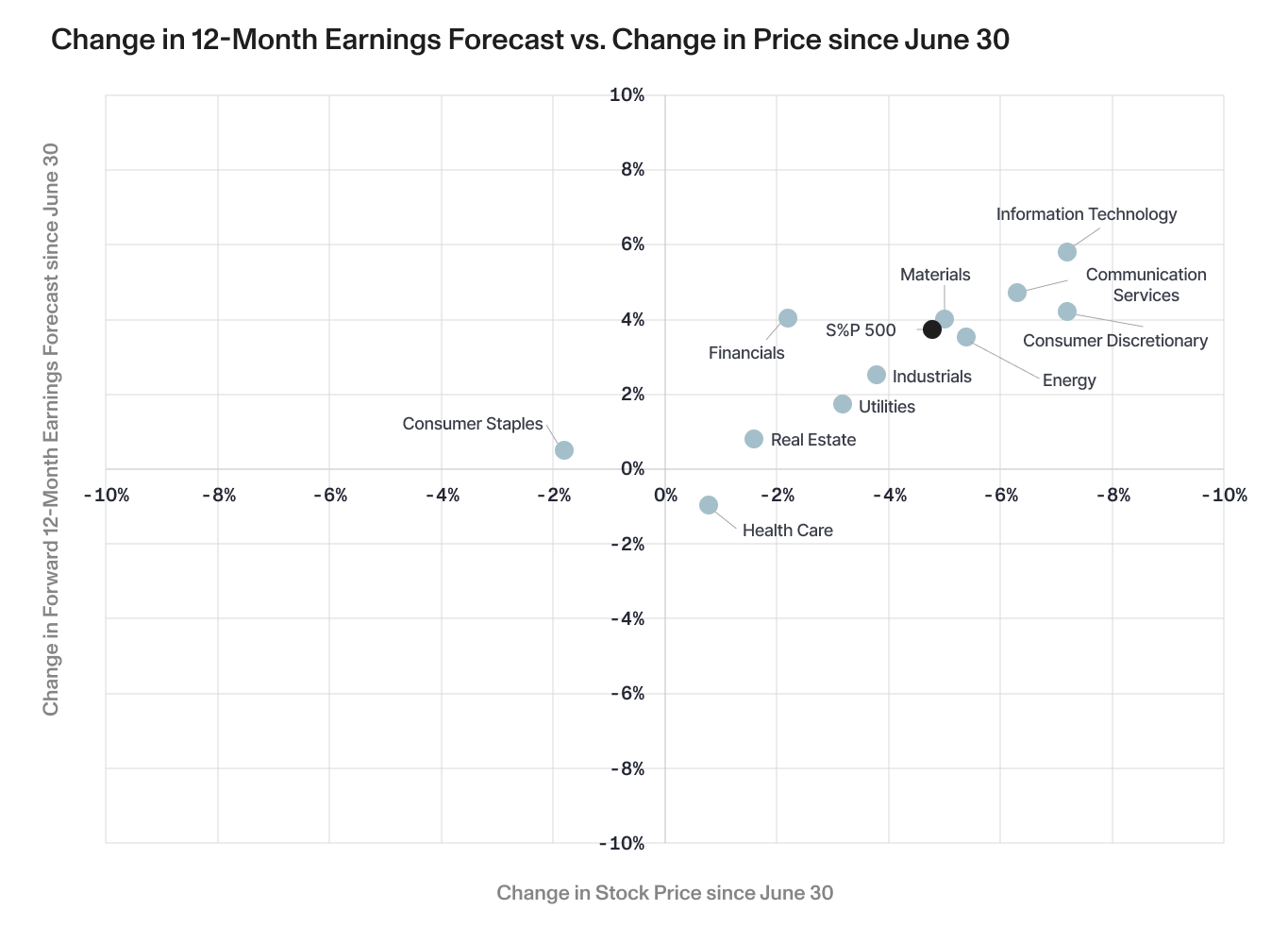

Indeed, equity prices since the June 30 low point in this year’s earnings expectation have been closely related to improving earnings forecasts. The chart below plots this relationship by economic sector. We can see that larger increases in year ahead earnings forecasts have been associated with higher stock price performance since the start of Q2. For the S&P 500 overall, the index gained 4.32% while forward 12-month EPS estimates increased 3.5%, indicating that most of the market's advance was supported by fundamental earnings improvements rather than multiple expansion alone. Still, multiples have expanded and they reflect an increasingly optimistic earnings growth outlook.

Part of that optimism is because of the continued strong earnings growth of US technology companies. The information technology sector reported 22.6% year-over-year earnings growth, making it the second-highest performing sector in Q2 after communication services (which is also heavily represented by tech related companies, like Alphabet).The delivered and expected earnings growth of the tech sector is reflected in its premium valuation, with its price-to-forward earnings ratio standing at 29.6, the highest among all sectors. While optimism for the earnings growth for the sector continues (88% of technology companies issued positive earnings guidance for the next year), expectations are extremely high making stock prices especially vulnerable to any earnings disappointment.33

Within the tech and communication services sector, the “Magnificent 7” companies (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla) were again standout earnings performers in Q2. All seven companies reported positive earnings surprises, delivering an aggregated 26.6% earnings growth from a year earlier, twice the growth delivered by the other 493 companies in the S&P 500.35 Four of these companies—NVIDIA, Amazon, Meta, and Microsoft—ranked among the top six contributors to S&P 500 earnings growth.

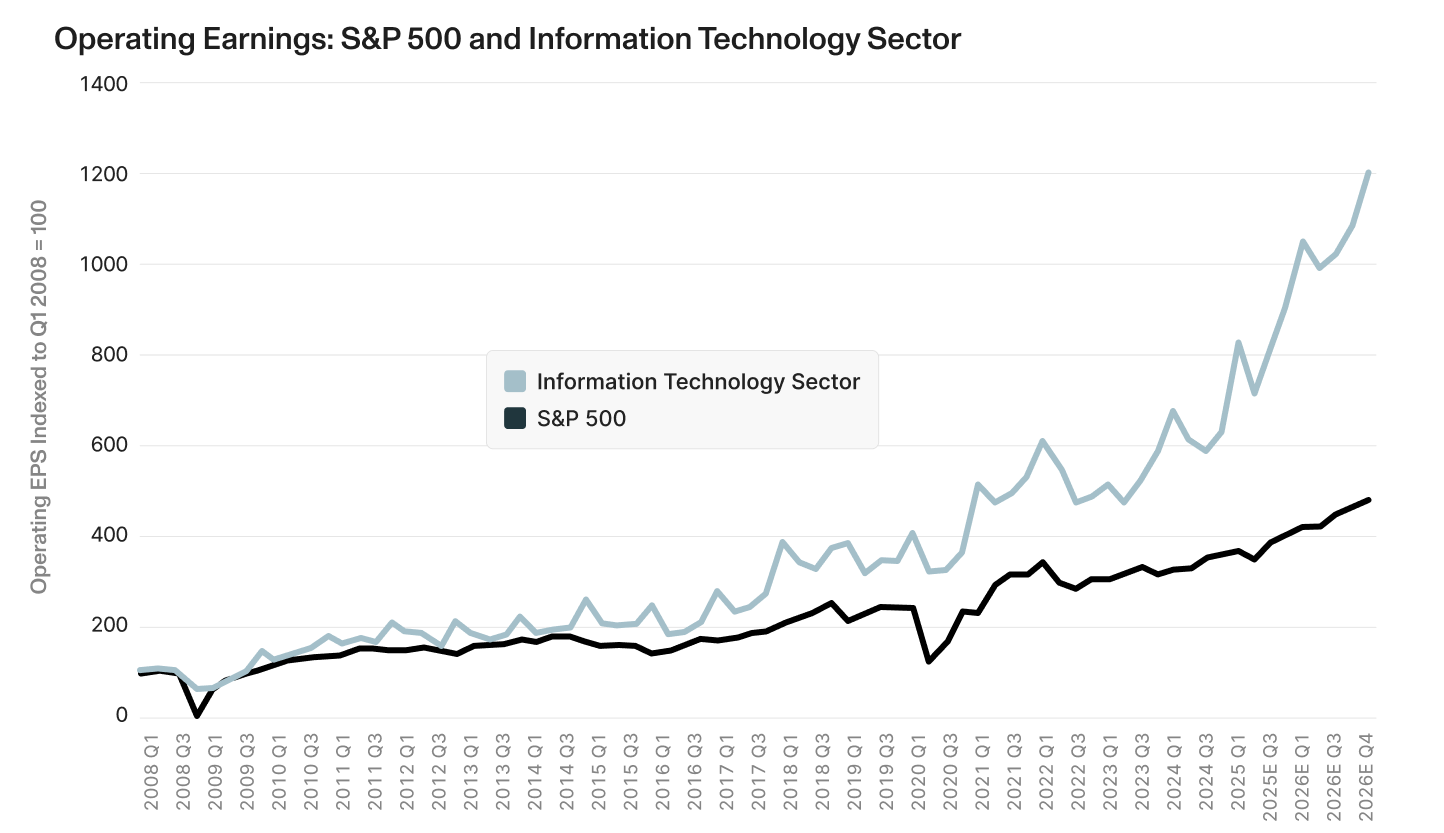

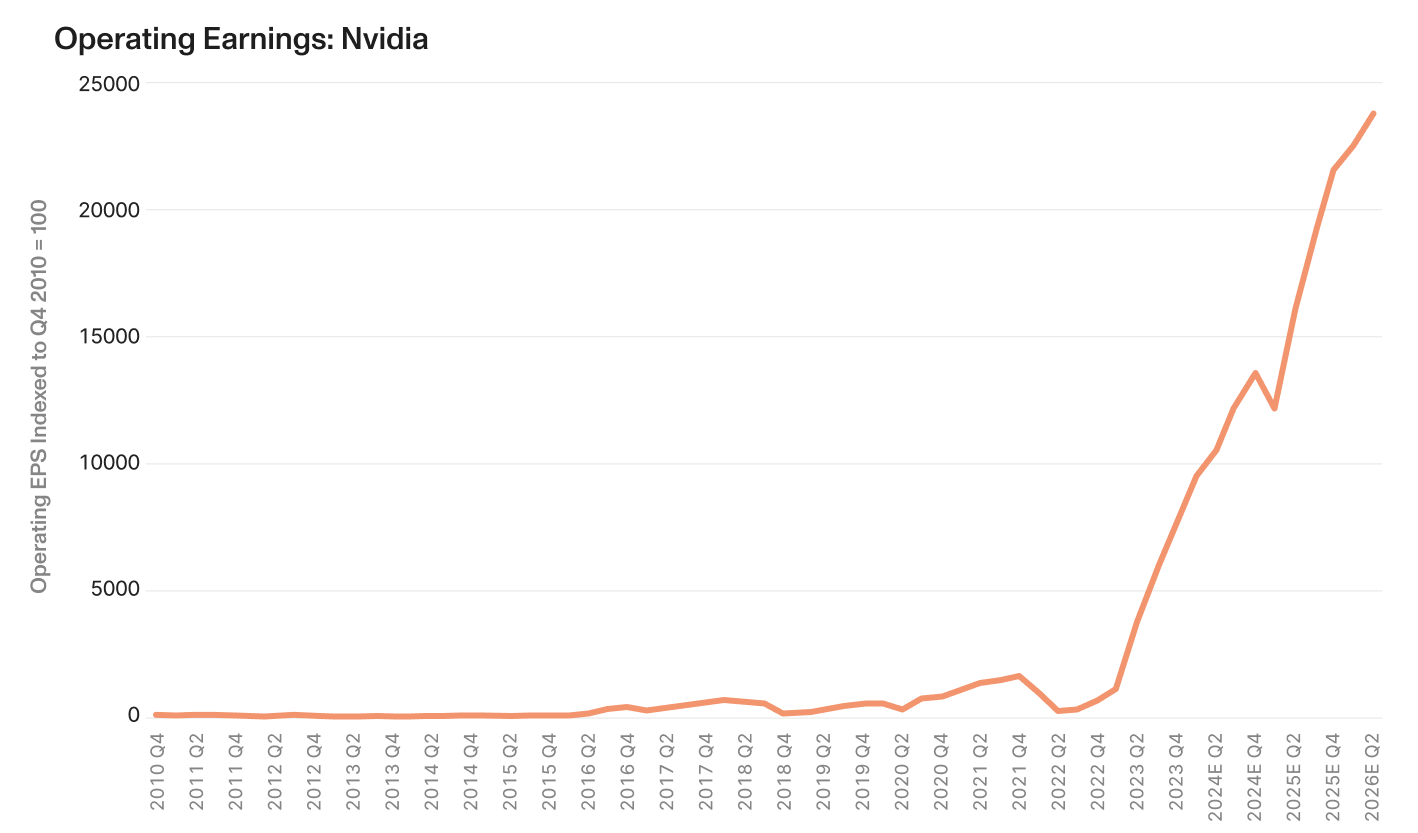

Artificial Intelligence investment is driving much of this earnings growth. We can see that trajectory in the chart below of Nvidia’s operating earnings growth.36 To understand the exceptional nature of that growth, note the differences in the scale of the chart versus the chart above showing the operating earnings of the S&P and the broader tech sector.

When viewed more broadly, there seems to have been a fundamental shift in economic drivers, with AI and technology investments becoming primary growth catalysts. In the first half of 2025, consumption contributed only 0.7% to GDP growth compared to the historical average of 1.7%, while business investment in information processing and R&D contributed 1.1% versus the typical 0.4%. NVIDIA's optimistic outlook projects $3-4 trillion in AI infrastructure spending by decade's end, underscoring the secular shift toward AI-driven capital allocation.37

The remarkable AI-driven growth engine is at least somewhat reflected in current stock prices for the related companies. Indeed, expectations are very high for this relatively narrow group. Hints or actual reports of anything that even slightly dampens that enthusiastic outlook will likely be met with an immediate downward adjustment in prices. Indeed, the market is showing increased sensitivity to earnings disappointments. So far in Q2, companies beating estimates saw performance the next day in line with historical averages, while those missing estimates experienced severe -6.4% average one day decline, nearly triple the historical average penalty.39

Earnings — What to look out for:

- Any slowing in the exceptional future earnings outlook for technology and AI related companies will hit the stock prices of those companies, and likely the overall market, very hard.

- Competition to the leading companies. In free markets, competition is usually what erodes exceptional profitability and earnings.

Navigating the Path Forward

The market's recent strength has been built on two pillars: anticipated rate cuts from the Fed and continued exceptional earnings growth from AI-driven technology companies. While both narratives have strong current support—with the Fed signaling clear dovish intent and technology earnings delivering remarkable results—the recent tailwind to these themes has embedded high expectations into asset prices. The path forward will likely be determined by whether these elevated expectations can be met or whether any disappointment triggers the kind of sharp repricing that markets have historically experienced when reality falls short of optimistic projections. Success in this environment will require careful attention to emerging data, disciplined risk management, and the flexibility to adapt as the reconciliation between expectations and outcomes unfolds.

Compound provides everything you need to manage your finances (liquidity planning, concentrated position management, stock option optimization, and more).

This material is approved for use in one-on-one presentations by authorized individuals only. Compound Planning, Inc. is an investment adviser registered with the Securities and Exchange Commission and based out of New York. The views expressed in this material are the views of Compound Planning through the period ended September 1, 2025 and are subject to change based on market and other conditions.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

All information is from Compound Planning unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Compound Planning is not, by means of this publication, rendering legal, tax, accounting, consulting, securities, real estate or other professional advice or services, and this publication should not be used as a basis for any investment decision or as a substitute for consultation with professional advisors. Compound Planning shall not be held responsible for any loss sustained by any person that relies on information contained in this publication.

This publication and the information contained herein is intended to offer general information and is not to be construed as a recommendation to make any decision concerning the purchase or sale of securities, insurance products, real estate, accounting and or legal services. Such offers are made only by prospectus, contract, or engagement agreement. A prospectus or contract should be read thoroughly and understood before investing or sending money. Investments involve risk. Investment return and principal value will fluctuate, so that your investment, when redeemed, may be worth more or less than its original cost. Past performance is not a guarantee of future results. All such decisions should be based on the consideration of specific objectives, relevant facts, pertinent issues and particular circumstances, and should involve appropriate professional advisors.